The global Iron Ore Market was valued at USD 284.67 billion in 2026 and is projected to reach USD 462.20 billion by 2036, expanding at a CAGR of 4.81% during the forecast period. Iron ore remains one of the world's most strategically important mineral resources, serving as the primary raw material for steel production and supporting industries ranging from construction and transportation to manufacturing, energy, and infrastructure development. Approximately 98% of globally mined iron ore is utilized in steelmaking, highlighting its indispensable role in economic development and industrial growth.

The market continues to benefit from increasing urbanization, large-scale infrastructure investments, and expanding industrial activity across both developed and emerging economies. Simultaneously, the global transition toward low-carbon steel production is reshaping demand for premium-grade iron ore suitable for direct reduced iron (DRI) and hydrogen-based steelmaking processes. Technological advancements in mining automation, ore beneficiation, digital operations, and sustainable extraction practices are further improving operational efficiency while supporting long-term market expansion.

Market growth is supported by increasing global steel consumption, infrastructure development, renewable energy expansion, urbanization, and growing demand for high-grade iron ore suitable for low-carbon steel production.

The iron ore industry is entering a new phase of transformation as traditional demand from construction and manufacturing is increasingly complemented by emerging requirements associated with sustainable steel production. Rapid urbanization across Asia-Pacific, expanding transportation networks, renewable energy infrastructure, and industrial modernization programs continue to generate significant demand for steel and, consequently, iron ore.

At the same time, governments and steel producers worldwide are investing heavily in decarbonization initiatives, including hydrogen-based direct reduced iron technologies and electric arc furnace production. These evolving production routes require higher-grade, lower-impurity iron ore capable of improving process efficiency while reducing carbon emissions. As a result, mining companies are expanding beneficiation capacity, improving ore quality, and investing in advanced extraction technologies to meet changing customer requirements and strengthen long-term competitiveness.

Rising Global Steel Demand from Infrastructure and Construction Development

The iron ore market is primarily driven by the expanding global steel industry, which consumes nearly 98% of all mined iron ore. Rapid urbanization, large-scale infrastructure development, commercial construction, and increasing investments in transportation networks continue to fuel steel consumption across both developed and emerging economies. Government-led infrastructure initiatives, smart city projects, and industrial expansion are generating sustained demand for high-quality iron ore to support long-term steel production.

Accelerating Industrialization Across Emerging Economies

Rapid industrial growth in countries such as India, Vietnam, Indonesia, and other Southeast Asian economies is significantly increasing iron ore consumption. Expansion of manufacturing facilities, logistics infrastructure, industrial parks, railways, ports, and urban development projects is driving higher steel demand, strengthening the need for stable iron ore supplies to support economic growth and industrialization.

Renewable Energy Expansion Supporting Steel Consumption

The global transition toward renewable energy is creating new opportunities for the iron ore market. Wind turbines, solar mounting structures, transmission towers, and grid infrastructure require substantial volumes of steel, directly increasing demand for iron ore. As governments continue investing in clean energy capacity and power infrastructure, steel-intensive renewable energy projects are expected to remain a key long-term growth driver for the market.

Advancements in Mining Technologies and Digital Operations

Continuous improvements in mining automation, artificial intelligence, autonomous equipment, remote monitoring, predictive maintenance, and ore beneficiation technologies are enhancing operational efficiency while reducing production costs. These technological innovations enable mining companies to optimize resource utilization, improve productivity, enhance worker safety, and maintain consistent production levels in increasingly competitive global markets.

Government Support for Domestic Mining and Resource Security

Many governments are implementing policies aimed at strengthening domestic mining industries and securing critical raw material supply chains. Mining incentives, infrastructure investments, export policy reforms, and streamlined regulatory approvals are encouraging new exploration projects and production capacity expansion. These initiatives are improving long-term supply security while enhancing the global competitiveness of major iron ore-producing countries.

Stringent Environmental Regulations and Sustainability Requirements

Iron ore mining operations face increasing regulatory scrutiny due to their environmental impact, including land degradation, deforestation, water consumption, and greenhouse gas emissions. Compliance with stricter environmental standards, mine rehabilitation requirements, and sustainability regulations has increased operational complexity and capital expenditure for mining companies, particularly in environmentally sensitive regions.

Volatility in Iron Ore Prices and Steel Market Demand

The iron ore market remains highly cyclical and closely linked to fluctuations in global steel production and macroeconomic conditions. Changes in construction activity, manufacturing output, infrastructure spending, and international trade can significantly affect iron ore demand and pricing. Price volatility creates uncertainty for producers, investors, and downstream steel manufacturers, impacting profitability and long-term investment decisions.

High Capital Investment and Infrastructure Requirements

Iron ore mining requires substantial investment in exploration, extraction equipment, processing plants, rail networks, ports, and logistics infrastructure. Developing and maintaining these assets—particularly in remote mining regions—requires significant capital expenditure and long project development timelines. These high entry barriers limit new market participation and increase operational risks for mining companies.

Supply Chain Disruptions and Logistics Challenges

The global iron ore industry relies heavily on efficient transportation networks, including railways, bulk shipping routes, and export terminals. Disruptions caused by extreme weather events, geopolitical tensions, labor shortages, port congestion, or transportation bottlenecks can interrupt supply chains, delay shipments, and increase operating costs. Maintaining resilient logistics infrastructure remains essential to ensuring stable global iron ore supply.

Rising Demand for High-Grade Iron Ore in Green Steel Production

The global shift toward low-carbon steelmaking is increasing demand for premium-grade iron ore with higher iron content and lower impurities. Hydrogen-based direct reduced iron (DRI) technologies and electric arc furnace (EAF) production require superior-quality feedstock, creating significant opportunities for producers capable of supplying high-grade ores that support decarbonization goals.

Expansion of Mining Projects in Emerging Resource-Rich Regions

Growing investments in untapped iron ore reserves, particularly in West Africa, Australia, Brazil, and other resource-rich regions, are creating new opportunities for production expansion. Large-scale mining developments supported by improved infrastructure and foreign investment are expected to strengthen future global supply capacity.

Digital Transformation and Smart Mining Technologies

Increasing adoption of artificial intelligence, automation, autonomous haulage systems, drone-based surveying, predictive maintenance, and digital mine management platforms is improving mining efficiency, reducing operating costs, and enhancing environmental performance. Companies investing in smart mining technologies are expected to gain stronger competitive advantages.

Sustainable Mining and Beneficiation Innovations

Growing emphasis on ESG performance is encouraging investment in energy-efficient processing, advanced ore beneficiation, renewable energy integration, water recycling systems, and carbon reduction initiatives. Mining companies that successfully improve operational sustainability while maintaining productivity are expected to benefit from stronger investor confidence, regulatory support, and long-term customer relationships.

Asia-Pacific dominates the global market due to extensive steel production, rapid industrialization, and large-scale infrastructure investments, particularly in China and India.

North America maintains stable demand driven by domestic steel manufacturing, infrastructure modernization, and investments in sustainable steel production.

Europe is increasingly focused on sourcing high-grade iron ore to support hydrogen-based steelmaking and low-carbon industrial initiatives.

Latin America, led by Brazil, remains one of the world's largest iron ore exporting regions with abundant reserves and well-established export infrastructure.

Middle East & Africa are emerging growth regions supported by large untapped reserves, new mining investments, and strategic infrastructure developments, particularly in Guinea.

North America maintains a stable position in the global iron ore market, supported by well-established steel manufacturing industries and consistent demand from construction, automotive, machinery, and energy infrastructure sectors. The United States and Canada continue to produce high-grade iron ore primarily for domestic steel production, reducing dependence on imported raw materials while strengthening regional supply security. Canada remains one of the world's leading iron ore producers and exporters, benefiting from abundant reserves and efficient mining operations. Increasing investments in mine automation, digital technologies, beneficiation processes, and sustainable mining practices are enhancing productivity while supporting environmental objectives. The region's growing emphasis on electric arc furnace (EAF) steel production and low-carbon manufacturing is also increasing demand for premium-quality iron ore products suitable for cleaner steelmaking technologies.

Europe represents one of the world's largest iron ore consuming regions despite limited domestic production capacity. The region relies heavily on imports from Brazil, Sweden, Canada, and Australia to support its advanced steel, automotive, engineering, and manufacturing industries. The transition toward green steel production and carbon neutrality is fundamentally reshaping regional demand patterns, with steel producers increasingly seeking high-grade, low-impurity iron ore suitable for hydrogen-based direct reduced iron (DRI) processes. Governments across Europe continue to invest in hydrogen infrastructure, low-carbon industrial technologies, and emissions reduction initiatives, creating long-term opportunities for premium iron ore suppliers capable of supporting next-generation steel production.

Asia-Pacific dominates the global iron ore market and is expected to maintain its leadership position throughout the forecast period. China remains the world's largest consumer of iron ore due to its enormous steel production capacity and continuous investments in construction, infrastructure, manufacturing, and industrial development. Australia continues to lead global exports through extensive mining operations and efficient transportation infrastructure, while India is strengthening its position through expanding domestic production and growing steel manufacturing capacity. Rapid urbanization, industrialization, transportation infrastructure development, and increasing manufacturing activity across Southeast Asian economies including Vietnam, Indonesia, and Thailand continue to generate substantial demand for iron ore and steel products, reinforcing the region's long-term growth outlook.

Latin America remains one of the world's most significant iron ore exporting regions, led by Brazil's extensive high-grade iron ore reserves and globally competitive mining industry. Strong export infrastructure, established international trade relationships, and abundant natural resources position the region as a critical supplier to steel producers across Asia and Europe. Mining companies continue investing in production capacity expansion, operational efficiency, and sustainable mining technologies to maintain global competitiveness. However, political uncertainty, environmental regulations, permitting challenges, and infrastructure development requirements may continue to influence future investment decisions and production growth across certain parts of the region.

The Middle East & Africa region possesses some of the world's largest untapped iron ore reserves, particularly across West Africa, creating substantial long-term growth potential. Countries such as Guinea are attracting significant international investment through large-scale mining projects including the Simandou development, which is expected to become one of the world's most important sources of high-grade iron ore. Growing investment from international mining companies and steel producers is supporting infrastructure development, railway construction, and port expansion throughout the region. Although logistical constraints, regulatory complexity, financing requirements, and transportation infrastructure remain key challenges, continued resource development is expected to strengthen the region's strategic importance within the global iron ore supply chain.

The United States continues to maintain a strong domestic iron ore industry, with production concentrated primarily in the Great Lakes region, particularly Minnesota and Michigan. High-grade iron ore pellets produced within the country remain essential for domestic blast furnace operations and steel manufacturing, supporting construction, automotive, machinery, defense, and infrastructure industries. Ongoing investments in transportation networks, energy infrastructure, and industrial modernization continue to generate stable demand for domestically produced iron ore while reducing dependence on imported raw materials.

The country's steel industry is also undergoing a significant transformation as manufacturers adopt lower-carbon production technologies and improve operational efficiency. Growing investments in advanced beneficiation technologies, electric arc furnace (EAF)-compatible iron ore feedstocks, mine automation, and sustainable processing methods are helping improve productivity while supporting national decarbonization objectives. Government initiatives promoting domestic manufacturing, supply chain resilience, and critical mineral security are expected to encourage additional investment across the U.S. iron ore value chain.

Germany remains one of Europe's largest consumers of iron ore, supported by its globally competitive automotive, engineering, machinery, and industrial manufacturing sectors. Although domestic iron ore production is limited, the country imports substantial volumes of high-grade ore from Brazil, Sweden, Canada, and other major producing nations to supply its integrated steel industry. Strong industrial demand and advanced manufacturing capabilities continue to make iron ore a strategic raw material within Germany's economy.

The country's ambitious climate objectives are accelerating the transition toward hydrogen-based direct reduced iron (DRI) production and low-carbon steelmaking technologies. Significant investments in hydrogen infrastructure, renewable energy integration, and industrial decarbonization are increasing demand for premium-grade, low-contaminant iron ore suitable for cleaner production processes. As Germany continues to modernize its steel industry, suppliers capable of providing high-quality iron ore for green steel production are expected to benefit from expanding long-term market opportunities.

Japan remains one of the world's largest importers of iron ore, relying primarily on supplies from Australia and Brazil to support its highly advanced steel manufacturing industry. Despite limited domestic mineral resources, Japan has developed one of the world's most technologically advanced steel sectors, supplying high-quality materials to automotive, shipbuilding, heavy machinery, electronics, and construction industries. Stable import supply chains and efficient steel production processes continue to support the country's industrial competitiveness.

Japan is increasingly investing in low-carbon steelmaking technologies, hydrogen-based production methods, and resource-efficient manufacturing as part of its long-term carbon neutrality strategy. Steel producers are evaluating higher-grade iron ore feedstocks capable of improving efficiency while reducing emissions during future production processes. Continued investment in advanced steel technologies, recycling initiatives, and sustainable industrial practices is expected to strengthen demand for premium iron ore products while supporting Japan's transition toward a more environmentally sustainable steel industry.

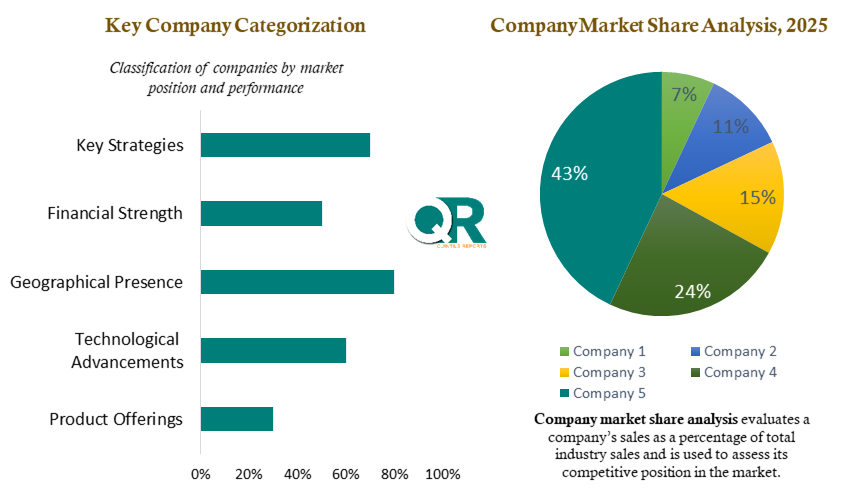

The global Iron Ore Market is highly consolidated, with a small group of multinational mining companies controlling a significant share of global production and exports. Market leaders benefit from extensive high-grade reserves, integrated mining and logistics operations, strong financial resources, and long-term supply agreements with leading steel manufacturers. Their ability to operate large-scale, low-cost mining assets while maintaining efficient transportation networks provides a significant competitive advantage and creates substantial barriers to entry for new market participants.

Technological innovation has become a key competitive differentiator as mining companies increasingly deploy automation, artificial intelligence, autonomous haulage systems, digital mine management platforms, predictive maintenance, and advanced ore beneficiation technologies to improve operational efficiency, enhance worker safety, and reduce production costs. Investments in digital transformation are enabling producers to optimize resource recovery, improve ore quality, increase productivity, and strengthen compliance with increasingly stringent environmental and operational standards.

Geographic positioning and logistics infrastructure continue to play a critical role in determining market competitiveness. Producers with access to high-grade reserves located near major export ports, rail networks, and key steel-producing markets benefit from lower transportation costs, faster delivery timelines, and stronger supply chain reliability. Australia and Brazil continue to dominate global seaborne iron ore trade due to their extensive resource base, world-class mining infrastructure, and established export capabilities, allowing major producers to maintain strong relationships with steel manufacturers across Asia, Europe, and other international markets.

Environmental, Social, and Governance (ESG) performance is becoming increasingly important as steel producers and investors prioritize sustainable sourcing and lower-carbon supply chains. Mining companies are investing in renewable energy integration, water conservation technologies, mine rehabilitation programs, carbon reduction initiatives, and responsible community engagement to strengthen their sustainability credentials. Producers capable of supplying high-grade, low-impurity iron ore that supports hydrogen-based direct reduced iron (DRI) and low-carbon steel production are expected to gain a significant competitive advantage as global decarbonization efforts accelerate.

In addition, pricing strategies, diversified customer portfolios, and long-term offtake agreements continue to influence market positioning. Companies with geographically diversified operations, flexible production capabilities, resilient supply chains, and balanced exposure to both contract and spot markets are better positioned to withstand commodity price volatility and fluctuations in global steel demand.

Key market participants include Vale S.A., Rio Tinto, BHP, Fortescue Metals Group Ltd., Anglo American plc, Ansteel Group Corporation Limited, ArcelorMittal, METALLOINVEST MC LLC, LKAB, Cleveland-Cliffs Inc., HBIS Group, EVRAZ plc, Tata Steel, POSCO, JSW Steel, Northern Iron & Machine, Shree Minerals Ltd., Mount Gibson Iron, Iron Ore Company of Canada, China Minmetals Corporation, National Mineral Development Corporation (NMDC), and other regional and global mining companies.

Recent developments reflect the industry's increasing focus on sustainable steelmaking, pelletization technologies, and expansion of high-grade iron ore supply. In September 2024, Metso secured a contract to supply a travelling-grate pelletizing plant for Ruifeng Iron & Steel in Tangshan, Hebei. Designed with an annual production capacity of 1.7 million tonnes, the facility incorporates advanced indurating furnace technology, digital process instrumentation, and automated control systems to improve pellet quality, reduce carbon emissions, and replace less efficient shaft furnace operations, supporting cleaner and more energy-efficient steel production.

In July 2024, Rio Tinto announced that its Simandou Project had received all required regulatory approvals from both the Guinean and Chinese authorities. The project, recognized as one of the world's largest undeveloped high-grade iron ore deposits, is expected to significantly strengthen future global iron ore supply while providing premium-quality, low-impurity ore suitable for hydrogen-based direct reduced iron (DRI) production and other low-carbon steelmaking technologies. The development is anticipated to play a pivotal role in supporting the global steel industry's decarbonization efforts and enhancing long-term supply chain resilience.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 4.81 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Type |

|

| The Segment Covered by Product Grade |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report provides a comprehensive, data-driven analysis of the global Iron Ore Market, developed through a rigorous research methodology that combines extensive primary research, secondary intelligence, and advanced market modeling. The study draws on insights from mining companies, steel manufacturers, raw material suppliers, industry experts, government agencies, trade associations, and logistics providers to deliver an objective assessment of current market conditions and future growth opportunities.

The analysis covers the complete iron ore value chain, from exploration and mining to beneficiation, transportation, export logistics, steel production, and end-use industries. Market estimates are validated using production volumes, trade statistics, mining capacity, steel consumption patterns, infrastructure investments, and regional demand trends, ensuring a high level of analytical accuracy and reliability. Particular emphasis is placed on evaluating high-grade iron ore demand, green steel initiatives, hydrogen-based direct reduced iron (DRI) technologies, and evolving decarbonization strategies that are reshaping the global iron ore industry.

The report also examines key market drivers, technological advancements in mining automation and ore beneficiation, environmental regulations, supply chain developments, and geopolitical factors influencing global iron ore production and trade. Advanced forecasting models, demand-supply analysis, and data triangulation techniques are employed to generate reliable market forecasts and identify emerging opportunities across major producing and consuming regions.

Backed by robust research methodologies and continuous industry monitoring, this report serves as a trusted source of strategic intelligence for mining companies, steel producers, investors, equipment manufacturers, policymakers, and other stakeholders seeking to understand competitive dynamics, evaluate investment opportunities, optimize supply chain strategies, and make informed business decisions within the global Iron Ore Market.

This study on the Iron Ore Market was developed using a comprehensive research framework that integrates primary research, secondary intelligence gathering, and advanced quantitative analysis to provide accurate, reliable, and actionable market insights. The research process began with an extensive review of mining industry publications, company annual reports, investor presentations, government mining statistics, geological surveys, customs and trade databases, steel industry reports, commodity market analyses, and publications from international mining organizations. Particular emphasis was placed on evaluating iron ore production trends, reserve distribution, steel manufacturing demand, seaborne trade flows, pricing movements, beneficiation technologies, and sustainability initiatives influencing the global iron ore industry.

Primary research involved in-depth interviews with iron ore producers, mining companies, steel manufacturers, commodity traders, logistics providers, equipment manufacturers, distributors, procurement managers, industry consultants, and regulatory authorities across major producing and consuming regions. These interactions validated secondary findings while providing valuable insights into production capacity expansion, mining investments, ore grade demand, pricing dynamics, export trends, technological advancements, supply chain developments, and future market opportunities.

Market size estimation and forecasting were conducted using a combination of bottom-up and top-down methodologies. The bottom-up approach evaluated revenues generated by leading iron ore producers, production volumes, export shipments, mine capacities, and end-use demand across steel manufacturing, construction, automotive, machinery, energy, and industrial sectors. The top-down approach validated market estimates through analysis of global steel production, infrastructure investments, industrial output, construction spending, international trade flows, and macroeconomic indicators influencing iron ore consumption.

Forecast models incorporated critical market variables including global steel demand, urbanization trends, infrastructure development, mining capacity expansion, high-grade iron ore adoption, hydrogen-based direct reduced iron (DRI) production, green steel initiatives, commodity price fluctuations, environmental regulations, and technological advancements in mining automation and ore beneficiation. Regional market forecasts were further refined through analysis of government mining policies, export regulations, transportation infrastructure, logistics capacity, and investment activity across key producing and consuming countries.

All findings were subjected to rigorous data triangulation and validation using independent industry databases, company disclosures, trade associations, government statistics, and expert consultations to ensure the highest level of analytical accuracy, consistency, and reliability. This robust methodology enables the report to provide dependable market intelligence, helping mining companies, steel producers, investors, policymakers, equipment manufacturers, and other stakeholders make informed strategic, operational, and investment decisions within the global Iron Ore Market.

This report has been prepared by a team of experienced mining industry analysts, metals and minerals specialists, and commodity market researchers with extensive expertise in iron ore mining, steel manufacturing, raw material supply chains, and global commodity markets. Combining deep industry knowledge with advanced research methodologies, the team delivers comprehensive insights into production trends, trade dynamics, technological advancements, sustainability initiatives, competitive developments, and long-term growth opportunities shaping the global Iron Ore Market.

Leveraging a robust research framework that integrates primary interviews, secondary intelligence, quantitative market modeling, and expert validation, our analysts continuously monitor developments across the iron ore value chain—from exploration and mining operations to beneficiation, transportation, steel production, and end-use industries. The report also evaluates evolving trends in green steel production, hydrogen-based direct reduced iron (DRI) technologies, mining automation, ESG initiatives, and government policies influencing global iron ore demand and supply.

Our commitment to analytical excellence, data integrity, and objective market assessment ensures that every market estimate, forecast, and strategic insight is supported by credible industry sources and rigorous validation processes. The intelligence presented in this report is designed to help mining companies, steel manufacturers, investors, equipment suppliers, policymakers, traders, and other industry stakeholders identify emerging opportunities, evaluate competitive positioning, optimize investment strategies, and make informed long-term business decisions within the global Iron Ore Market.

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Iron Ore Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Iron Ore Market, by Region, (USD Million) 2017-2036

Table 9 Germany Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Iron Ore Market, by Region, (USD Million) 2017-2036

Table 21 China Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Iron Ore Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Iron Ore Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Iron Ore Market: Market Scenario

Fig.4 Global Iron Ore Market Competitive Outlook

Fig.5 Global Iron Ore Market Driver Analysis

Fig.6 Global Iron Ore Market Restraint Analysis

Fig.7 Global Iron Ore Market Opportunity Analysis

Fig.8 Global Iron Ore Market Trends Analysis

Fig.9 Global Iron Ore Market: Segment Analysis (Based on the Scope)

Fig.10 Global Iron Ore Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Iron Ore Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Iron Ore Market, by Region, (USD Million) 2017-2036

Table 9 Germany Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Iron Ore Market, by Region, (USD Million) 2017-2036

Table 21 China Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Iron Ore Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Iron Ore Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Iron Ore Market: Market Scenario

Fig.4 Global Iron Ore Market Competitive Outlook

Fig.5 Global Iron Ore Market Driver Analysis

Fig.6 Global Iron Ore Market Restraint Analysis

Fig.7 Global Iron Ore Market Opportunity Analysis

Fig.8 Global Iron Ore Market Trends Analysis

Fig.9 Global Iron Ore Market: Segment Analysis (Based on the Scope)

Fig.10 Global Iron Ore Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Iron ore is a naturally occurring mineral that serves as the primary raw material for steel production. Around 98% of globally mined iron ore is used in manufacturing steel for construction, transportation, infrastructure, and industrial applications.

Iron ore is essential for producing steel, which forms the foundation of buildings, bridges, automobiles, railways, machinery, renewable energy infrastructure, and numerous industrial products.

Growth is driven by increasing global steel demand, urbanization, infrastructure development, renewable energy projects, industrial expansion, and rising demand for high-grade iron ore used in green steel production.

Green steel refers to steel produced using low-carbon technologies such as hydrogen-based Direct Reduced Iron (DRI) and electric arc furnaces (EAF), significantly reducing greenhouse gas emissions compared to conventional steelmaking.

High-grade iron ore improves production efficiency and reduces carbon emissions during steel manufacturing, making it essential for low-carbon and hydrogen-based steelmaking processes.

Asia-Pacific dominates the market due to extensive steel production, rapid industrialization, and strong demand from China, India, and other emerging economies.

Leading companies include Vale S.A., Rio Tinto, BHP, Fortescue Metals Group, Anglo American, LKAB, Cleveland-Cliffs, Tata Steel, POSCO, and NMDC.

The global Iron Ore Market is projected to grow at a CAGR of 4.81% during the forecast period from 2026 to 2036.

The global Iron Ore Market was valued at USD 284.67 billion in 2026 and is projected to reach USD 462.20 billion by 2036, expanding at a CAGR of 4.81% during the forecast period. Iron ore remains one of the world's most strategically important mineral resources, serving as the primary raw material for steel production and supporting industries ranging from construction and transportation to manufacturing, energy, and infrastructure development. Approximately 98% of globally mined iron ore is utilized in steelmaking, highlighting its indispensable role in economic development and industrial growth.

The market continues to benefit from increasing urbanization, large-scale infrastructure investments, and expanding industrial activity across both developed and emerging economies. Simultaneously, the global transition toward low-carbon steel production is reshaping demand for premium-grade iron ore suitable for direct reduced iron (DRI) and hydrogen-based steelmaking processes. Technological advancements in mining automation, ore beneficiation, digital operations, and sustainable extraction practices are further improving operational efficiency while supporting long-term market expansion.

Market growth is supported by increasing global steel consumption, infrastructure development, renewable energy expansion, urbanization, and growing demand for high-grade iron ore suitable for low-carbon steel production.

The iron ore industry is entering a new phase of transformation as traditional demand from construction and manufacturing is increasingly complemented by emerging requirements associated with sustainable steel production. Rapid urbanization across Asia-Pacific, expanding transportation networks, renewable energy infrastructure, and industrial modernization programs continue to generate significant demand for steel and, consequently, iron ore.

At the same time, governments and steel producers worldwide are investing heavily in decarbonization initiatives, including hydrogen-based direct reduced iron technologies and electric arc furnace production. These evolving production routes require higher-grade, lower-impurity iron ore capable of improving process efficiency while reducing carbon emissions. As a result, mining companies are expanding beneficiation capacity, improving ore quality, and investing in advanced extraction technologies to meet changing customer requirements and strengthen long-term competitiveness.

Rising Global Steel Demand from Infrastructure and Construction Development

The iron ore market is primarily driven by the expanding global steel industry, which consumes nearly 98% of all mined iron ore. Rapid urbanization, large-scale infrastructure development, commercial construction, and increasing investments in transportation networks continue to fuel steel consumption across both developed and emerging economies. Government-led infrastructure initiatives, smart city projects, and industrial expansion are generating sustained demand for high-quality iron ore to support long-term steel production.

Accelerating Industrialization Across Emerging Economies

Rapid industrial growth in countries such as India, Vietnam, Indonesia, and other Southeast Asian economies is significantly increasing iron ore consumption. Expansion of manufacturing facilities, logistics infrastructure, industrial parks, railways, ports, and urban development projects is driving higher steel demand, strengthening the need for stable iron ore supplies to support economic growth and industrialization.

Renewable Energy Expansion Supporting Steel Consumption

The global transition toward renewable energy is creating new opportunities for the iron ore market. Wind turbines, solar mounting structures, transmission towers, and grid infrastructure require substantial volumes of steel, directly increasing demand for iron ore. As governments continue investing in clean energy capacity and power infrastructure, steel-intensive renewable energy projects are expected to remain a key long-term growth driver for the market.

Advancements in Mining Technologies and Digital Operations

Continuous improvements in mining automation, artificial intelligence, autonomous equipment, remote monitoring, predictive maintenance, and ore beneficiation technologies are enhancing operational efficiency while reducing production costs. These technological innovations enable mining companies to optimize resource utilization, improve productivity, enhance worker safety, and maintain consistent production levels in increasingly competitive global markets.

Government Support for Domestic Mining and Resource Security

Many governments are implementing policies aimed at strengthening domestic mining industries and securing critical raw material supply chains. Mining incentives, infrastructure investments, export policy reforms, and streamlined regulatory approvals are encouraging new exploration projects and production capacity expansion. These initiatives are improving long-term supply security while enhancing the global competitiveness of major iron ore-producing countries.

Stringent Environmental Regulations and Sustainability Requirements

Iron ore mining operations face increasing regulatory scrutiny due to their environmental impact, including land degradation, deforestation, water consumption, and greenhouse gas emissions. Compliance with stricter environmental standards, mine rehabilitation requirements, and sustainability regulations has increased operational complexity and capital expenditure for mining companies, particularly in environmentally sensitive regions.

Volatility in Iron Ore Prices and Steel Market Demand

The iron ore market remains highly cyclical and closely linked to fluctuations in global steel production and macroeconomic conditions. Changes in construction activity, manufacturing output, infrastructure spending, and international trade can significantly affect iron ore demand and pricing. Price volatility creates uncertainty for producers, investors, and downstream steel manufacturers, impacting profitability and long-term investment decisions.

High Capital Investment and Infrastructure Requirements

Iron ore mining requires substantial investment in exploration, extraction equipment, processing plants, rail networks, ports, and logistics infrastructure. Developing and maintaining these assets—particularly in remote mining regions—requires significant capital expenditure and long project development timelines. These high entry barriers limit new market participation and increase operational risks for mining companies.

Supply Chain Disruptions and Logistics Challenges

The global iron ore industry relies heavily on efficient transportation networks, including railways, bulk shipping routes, and export terminals. Disruptions caused by extreme weather events, geopolitical tensions, labor shortages, port congestion, or transportation bottlenecks can interrupt supply chains, delay shipments, and increase operating costs. Maintaining resilient logistics infrastructure remains essential to ensuring stable global iron ore supply.

Rising Demand for High-Grade Iron Ore in Green Steel Production

The global shift toward low-carbon steelmaking is increasing demand for premium-grade iron ore with higher iron content and lower impurities. Hydrogen-based direct reduced iron (DRI) technologies and electric arc furnace (EAF) production require superior-quality feedstock, creating significant opportunities for producers capable of supplying high-grade ores that support decarbonization goals.

Expansion of Mining Projects in Emerging Resource-Rich Regions

Growing investments in untapped iron ore reserves, particularly in West Africa, Australia, Brazil, and other resource-rich regions, are creating new opportunities for production expansion. Large-scale mining developments supported by improved infrastructure and foreign investment are expected to strengthen future global supply capacity.

Digital Transformation and Smart Mining Technologies

Increasing adoption of artificial intelligence, automation, autonomous haulage systems, drone-based surveying, predictive maintenance, and digital mine management platforms is improving mining efficiency, reducing operating costs, and enhancing environmental performance. Companies investing in smart mining technologies are expected to gain stronger competitive advantages.

Sustainable Mining and Beneficiation Innovations

Growing emphasis on ESG performance is encouraging investment in energy-efficient processing, advanced ore beneficiation, renewable energy integration, water recycling systems, and carbon reduction initiatives. Mining companies that successfully improve operational sustainability while maintaining productivity are expected to benefit from stronger investor confidence, regulatory support, and long-term customer relationships.

Asia-Pacific dominates the global market due to extensive steel production, rapid industrialization, and large-scale infrastructure investments, particularly in China and India.

North America maintains stable demand driven by domestic steel manufacturing, infrastructure modernization, and investments in sustainable steel production.

Europe is increasingly focused on sourcing high-grade iron ore to support hydrogen-based steelmaking and low-carbon industrial initiatives.

Latin America, led by Brazil, remains one of the world's largest iron ore exporting regions with abundant reserves and well-established export infrastructure.

Middle East & Africa are emerging growth regions supported by large untapped reserves, new mining investments, and strategic infrastructure developments, particularly in Guinea.

North America maintains a stable position in the global iron ore market, supported by well-established steel manufacturing industries and consistent demand from construction, automotive, machinery, and energy infrastructure sectors. The United States and Canada continue to produce high-grade iron ore primarily for domestic steel production, reducing dependence on imported raw materials while strengthening regional supply security. Canada remains one of the world's leading iron ore producers and exporters, benefiting from abundant reserves and efficient mining operations. Increasing investments in mine automation, digital technologies, beneficiation processes, and sustainable mining practices are enhancing productivity while supporting environmental objectives. The region's growing emphasis on electric arc furnace (EAF) steel production and low-carbon manufacturing is also increasing demand for premium-quality iron ore products suitable for cleaner steelmaking technologies.

Europe represents one of the world's largest iron ore consuming regions despite limited domestic production capacity. The region relies heavily on imports from Brazil, Sweden, Canada, and Australia to support its advanced steel, automotive, engineering, and manufacturing industries. The transition toward green steel production and carbon neutrality is fundamentally reshaping regional demand patterns, with steel producers increasingly seeking high-grade, low-impurity iron ore suitable for hydrogen-based direct reduced iron (DRI) processes. Governments across Europe continue to invest in hydrogen infrastructure, low-carbon industrial technologies, and emissions reduction initiatives, creating long-term opportunities for premium iron ore suppliers capable of supporting next-generation steel production.

Asia-Pacific dominates the global iron ore market and is expected to maintain its leadership position throughout the forecast period. China remains the world's largest consumer of iron ore due to its enormous steel production capacity and continuous investments in construction, infrastructure, manufacturing, and industrial development. Australia continues to lead global exports through extensive mining operations and efficient transportation infrastructure, while India is strengthening its position through expanding domestic production and growing steel manufacturing capacity. Rapid urbanization, industrialization, transportation infrastructure development, and increasing manufacturing activity across Southeast Asian economies including Vietnam, Indonesia, and Thailand continue to generate substantial demand for iron ore and steel products, reinforcing the region's long-term growth outlook.

Latin America remains one of the world's most significant iron ore exporting regions, led by Brazil's extensive high-grade iron ore reserves and globally competitive mining industry. Strong export infrastructure, established international trade relationships, and abundant natural resources position the region as a critical supplier to steel producers across Asia and Europe. Mining companies continue investing in production capacity expansion, operational efficiency, and sustainable mining technologies to maintain global competitiveness. However, political uncertainty, environmental regulations, permitting challenges, and infrastructure development requirements may continue to influence future investment decisions and production growth across certain parts of the region.

The Middle East & Africa region possesses some of the world's largest untapped iron ore reserves, particularly across West Africa, creating substantial long-term growth potential. Countries such as Guinea are attracting significant international investment through large-scale mining projects including the Simandou development, which is expected to become one of the world's most important sources of high-grade iron ore. Growing investment from international mining companies and steel producers is supporting infrastructure development, railway construction, and port expansion throughout the region. Although logistical constraints, regulatory complexity, financing requirements, and transportation infrastructure remain key challenges, continued resource development is expected to strengthen the region's strategic importance within the global iron ore supply chain.

The United States continues to maintain a strong domestic iron ore industry, with production concentrated primarily in the Great Lakes region, particularly Minnesota and Michigan. High-grade iron ore pellets produced within the country remain essential for domestic blast furnace operations and steel manufacturing, supporting construction, automotive, machinery, defense, and infrastructure industries. Ongoing investments in transportation networks, energy infrastructure, and industrial modernization continue to generate stable demand for domestically produced iron ore while reducing dependence on imported raw materials.

The country's steel industry is also undergoing a significant transformation as manufacturers adopt lower-carbon production technologies and improve operational efficiency. Growing investments in advanced beneficiation technologies, electric arc furnace (EAF)-compatible iron ore feedstocks, mine automation, and sustainable processing methods are helping improve productivity while supporting national decarbonization objectives. Government initiatives promoting domestic manufacturing, supply chain resilience, and critical mineral security are expected to encourage additional investment across the U.S. iron ore value chain.

Germany remains one of Europe's largest consumers of iron ore, supported by its globally competitive automotive, engineering, machinery, and industrial manufacturing sectors. Although domestic iron ore production is limited, the country imports substantial volumes of high-grade ore from Brazil, Sweden, Canada, and other major producing nations to supply its integrated steel industry. Strong industrial demand and advanced manufacturing capabilities continue to make iron ore a strategic raw material within Germany's economy.

The country's ambitious climate objectives are accelerating the transition toward hydrogen-based direct reduced iron (DRI) production and low-carbon steelmaking technologies. Significant investments in hydrogen infrastructure, renewable energy integration, and industrial decarbonization are increasing demand for premium-grade, low-contaminant iron ore suitable for cleaner production processes. As Germany continues to modernize its steel industry, suppliers capable of providing high-quality iron ore for green steel production are expected to benefit from expanding long-term market opportunities.

Japan remains one of the world's largest importers of iron ore, relying primarily on supplies from Australia and Brazil to support its highly advanced steel manufacturing industry. Despite limited domestic mineral resources, Japan has developed one of the world's most technologically advanced steel sectors, supplying high-quality materials to automotive, shipbuilding, heavy machinery, electronics, and construction industries. Stable import supply chains and efficient steel production processes continue to support the country's industrial competitiveness.

Japan is increasingly investing in low-carbon steelmaking technologies, hydrogen-based production methods, and resource-efficient manufacturing as part of its long-term carbon neutrality strategy. Steel producers are evaluating higher-grade iron ore feedstocks capable of improving efficiency while reducing emissions during future production processes. Continued investment in advanced steel technologies, recycling initiatives, and sustainable industrial practices is expected to strengthen demand for premium iron ore products while supporting Japan's transition toward a more environmentally sustainable steel industry.

The global Iron Ore Market is highly consolidated, with a small group of multinational mining companies controlling a significant share of global production and exports. Market leaders benefit from extensive high-grade reserves, integrated mining and logistics operations, strong financial resources, and long-term supply agreements with leading steel manufacturers. Their ability to operate large-scale, low-cost mining assets while maintaining efficient transportation networks provides a significant competitive advantage and creates substantial barriers to entry for new market participants.

Technological innovation has become a key competitive differentiator as mining companies increasingly deploy automation, artificial intelligence, autonomous haulage systems, digital mine management platforms, predictive maintenance, and advanced ore beneficiation technologies to improve operational efficiency, enhance worker safety, and reduce production costs. Investments in digital transformation are enabling producers to optimize resource recovery, improve ore quality, increase productivity, and strengthen compliance with increasingly stringent environmental and operational standards.

Geographic positioning and logistics infrastructure continue to play a critical role in determining market competitiveness. Producers with access to high-grade reserves located near major export ports, rail networks, and key steel-producing markets benefit from lower transportation costs, faster delivery timelines, and stronger supply chain reliability. Australia and Brazil continue to dominate global seaborne iron ore trade due to their extensive resource base, world-class mining infrastructure, and established export capabilities, allowing major producers to maintain strong relationships with steel manufacturers across Asia, Europe, and other international markets.

Environmental, Social, and Governance (ESG) performance is becoming increasingly important as steel producers and investors prioritize sustainable sourcing and lower-carbon supply chains. Mining companies are investing in renewable energy integration, water conservation technologies, mine rehabilitation programs, carbon reduction initiatives, and responsible community engagement to strengthen their sustainability credentials. Producers capable of supplying high-grade, low-impurity iron ore that supports hydrogen-based direct reduced iron (DRI) and low-carbon steel production are expected to gain a significant competitive advantage as global decarbonization efforts accelerate.

In addition, pricing strategies, diversified customer portfolios, and long-term offtake agreements continue to influence market positioning. Companies with geographically diversified operations, flexible production capabilities, resilient supply chains, and balanced exposure to both contract and spot markets are better positioned to withstand commodity price volatility and fluctuations in global steel demand.

Key market participants include Vale S.A., Rio Tinto, BHP, Fortescue Metals Group Ltd., Anglo American plc, Ansteel Group Corporation Limited, ArcelorMittal, METALLOINVEST MC LLC, LKAB, Cleveland-Cliffs Inc., HBIS Group, EVRAZ plc, Tata Steel, POSCO, JSW Steel, Northern Iron & Machine, Shree Minerals Ltd., Mount Gibson Iron, Iron Ore Company of Canada, China Minmetals Corporation, National Mineral Development Corporation (NMDC), and other regional and global mining companies.

Recent developments reflect the industry's increasing focus on sustainable steelmaking, pelletization technologies, and expansion of high-grade iron ore supply. In September 2024, Metso secured a contract to supply a travelling-grate pelletizing plant for Ruifeng Iron & Steel in Tangshan, Hebei. Designed with an annual production capacity of 1.7 million tonnes, the facility incorporates advanced indurating furnace technology, digital process instrumentation, and automated control systems to improve pellet quality, reduce carbon emissions, and replace less efficient shaft furnace operations, supporting cleaner and more energy-efficient steel production.

In July 2024, Rio Tinto announced that its Simandou Project had received all required regulatory approvals from both the Guinean and Chinese authorities. The project, recognized as one of the world's largest undeveloped high-grade iron ore deposits, is expected to significantly strengthen future global iron ore supply while providing premium-quality, low-impurity ore suitable for hydrogen-based direct reduced iron (DRI) production and other low-carbon steelmaking technologies. The development is anticipated to play a pivotal role in supporting the global steel industry's decarbonization efforts and enhancing long-term supply chain resilience.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 4.81 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Type |

|

| The Segment Covered by Product Grade |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report provides a comprehensive, data-driven analysis of the global Iron Ore Market, developed through a rigorous research methodology that combines extensive primary research, secondary intelligence, and advanced market modeling. The study draws on insights from mining companies, steel manufacturers, raw material suppliers, industry experts, government agencies, trade associations, and logistics providers to deliver an objective assessment of current market conditions and future growth opportunities.

The analysis covers the complete iron ore value chain, from exploration and mining to beneficiation, transportation, export logistics, steel production, and end-use industries. Market estimates are validated using production volumes, trade statistics, mining capacity, steel consumption patterns, infrastructure investments, and regional demand trends, ensuring a high level of analytical accuracy and reliability. Particular emphasis is placed on evaluating high-grade iron ore demand, green steel initiatives, hydrogen-based direct reduced iron (DRI) technologies, and evolving decarbonization strategies that are reshaping the global iron ore industry.

The report also examines key market drivers, technological advancements in mining automation and ore beneficiation, environmental regulations, supply chain developments, and geopolitical factors influencing global iron ore production and trade. Advanced forecasting models, demand-supply analysis, and data triangulation techniques are employed to generate reliable market forecasts and identify emerging opportunities across major producing and consuming regions.

Backed by robust research methodologies and continuous industry monitoring, this report serves as a trusted source of strategic intelligence for mining companies, steel producers, investors, equipment manufacturers, policymakers, and other stakeholders seeking to understand competitive dynamics, evaluate investment opportunities, optimize supply chain strategies, and make informed business decisions within the global Iron Ore Market.

This study on the Iron Ore Market was developed using a comprehensive research framework that integrates primary research, secondary intelligence gathering, and advanced quantitative analysis to provide accurate, reliable, and actionable market insights. The research process began with an extensive review of mining industry publications, company annual reports, investor presentations, government mining statistics, geological surveys, customs and trade databases, steel industry reports, commodity market analyses, and publications from international mining organizations. Particular emphasis was placed on evaluating iron ore production trends, reserve distribution, steel manufacturing demand, seaborne trade flows, pricing movements, beneficiation technologies, and sustainability initiatives influencing the global iron ore industry.

Primary research involved in-depth interviews with iron ore producers, mining companies, steel manufacturers, commodity traders, logistics providers, equipment manufacturers, distributors, procurement managers, industry consultants, and regulatory authorities across major producing and consuming regions. These interactions validated secondary findings while providing valuable insights into production capacity expansion, mining investments, ore grade demand, pricing dynamics, export trends, technological advancements, supply chain developments, and future market opportunities.

Market size estimation and forecasting were conducted using a combination of bottom-up and top-down methodologies. The bottom-up approach evaluated revenues generated by leading iron ore producers, production volumes, export shipments, mine capacities, and end-use demand across steel manufacturing, construction, automotive, machinery, energy, and industrial sectors. The top-down approach validated market estimates through analysis of global steel production, infrastructure investments, industrial output, construction spending, international trade flows, and macroeconomic indicators influencing iron ore consumption.

Forecast models incorporated critical market variables including global steel demand, urbanization trends, infrastructure development, mining capacity expansion, high-grade iron ore adoption, hydrogen-based direct reduced iron (DRI) production, green steel initiatives, commodity price fluctuations, environmental regulations, and technological advancements in mining automation and ore beneficiation. Regional market forecasts were further refined through analysis of government mining policies, export regulations, transportation infrastructure, logistics capacity, and investment activity across key producing and consuming countries.

All findings were subjected to rigorous data triangulation and validation using independent industry databases, company disclosures, trade associations, government statistics, and expert consultations to ensure the highest level of analytical accuracy, consistency, and reliability. This robust methodology enables the report to provide dependable market intelligence, helping mining companies, steel producers, investors, policymakers, equipment manufacturers, and other stakeholders make informed strategic, operational, and investment decisions within the global Iron Ore Market.

This report has been prepared by a team of experienced mining industry analysts, metals and minerals specialists, and commodity market researchers with extensive expertise in iron ore mining, steel manufacturing, raw material supply chains, and global commodity markets. Combining deep industry knowledge with advanced research methodologies, the team delivers comprehensive insights into production trends, trade dynamics, technological advancements, sustainability initiatives, competitive developments, and long-term growth opportunities shaping the global Iron Ore Market.

Leveraging a robust research framework that integrates primary interviews, secondary intelligence, quantitative market modeling, and expert validation, our analysts continuously monitor developments across the iron ore value chain—from exploration and mining operations to beneficiation, transportation, steel production, and end-use industries. The report also evaluates evolving trends in green steel production, hydrogen-based direct reduced iron (DRI) technologies, mining automation, ESG initiatives, and government policies influencing global iron ore demand and supply.

Our commitment to analytical excellence, data integrity, and objective market assessment ensures that every market estimate, forecast, and strategic insight is supported by credible industry sources and rigorous validation processes. The intelligence presented in this report is designed to help mining companies, steel manufacturers, investors, equipment suppliers, policymakers, traders, and other industry stakeholders identify emerging opportunities, evaluate competitive positioning, optimize investment strategies, and make informed long-term business decisions within the global Iron Ore Market.

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Iron Ore Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Iron Ore Market, by Region, (USD Million) 2017-2036

Table 9 Germany Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Iron Ore Market, by Region, (USD Million) 2017-2036

Table 21 China Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Iron Ore Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Iron Ore Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Iron Ore Market: Market Scenario

Fig.4 Global Iron Ore Market Competitive Outlook

Fig.5 Global Iron Ore Market Driver Analysis

Fig.6 Global Iron Ore Market Restraint Analysis

Fig.7 Global Iron Ore Market Opportunity Analysis

Fig.8 Global Iron Ore Market Trends Analysis

Fig.9 Global Iron Ore Market: Segment Analysis (Based on the Scope)

Fig.10 Global Iron Ore Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Iron Ore Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Iron Ore Market, by Region, (USD Million) 2017-2036

Table 9 Germany Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Iron Ore Market, by Segment Analysis, (USD Million) 2017-2036