The global Aramid Fiber Market was valued at USD 4.98 billion in 2026 and is projected to reach USD 11.88 billion by 2036, expanding at a CAGR of 8.81% during the forecast period. Aramid fibers are among the world's most advanced high-performance synthetic materials, valued for their exceptional tensile strength, lightweight properties, heat resistance, flame retardancy, and superior chemical stability. Available primarily as para-aramid and meta-aramid fibers, these materials play a critical role in applications requiring high durability and protection across defense, aerospace, automotive, industrial manufacturing, telecommunications, electrical insulation, and personal protective equipment. Growing demand for lightweight composite materials, increasing defense modernization programs, and rising adoption of advanced protective solutions are significantly accelerating market expansion worldwide.

The market is also benefiting from rapid technological advancements in fiber engineering, sustainable manufacturing processes, and next-generation composite materials. Increasing utilization of aramid fibers in electric vehicles, battery protection systems, lightweight automotive components, industrial filtration, friction materials, wind energy, and high-performance sporting goods is creating new avenues for growth. Furthermore, continuous investments by leading manufacturers in production capacity expansion, specialty fiber development, recycling technologies, and environmentally sustainable production methods are strengthening the long-term outlook for the global Aramid Fiber Market.

Market growth is driven by increasing demand from defense, aerospace, electric vehicles, industrial safety equipment, lightweight composites, and advanced manufacturing applications.

According to Quintile Reports' analysts, rising demand for lightweight composite materials, increasing defense modernization programs, and expanding electric vehicle production will continue to drive long-term growth in the Aramid Fiber Market. Advances in recyclable aramid materials, next-generation para-aramid fibers, and sustainable manufacturing technologies are expected to create new opportunities for manufacturers across defense, aerospace, automotive, and industrial applications.

Rising Demand for Lightweight Automotive Components

The automotive industry is increasingly adopting aramid fibers to manufacture lightweight, high-strength components such as belts, hoses, tires, brake pads, gaskets, clutch facings, and heat shields. Their exceptional mechanical strength, abrasion resistance, and thermal stability enable manufacturers to reduce vehicle weight while improving fuel efficiency and overall performance. The accelerating transition toward electric vehicles (EVs), high-performance sports cars, and stricter emission regulations is further driving the demand for advanced aramid fiber composites across the global automotive sector.

Growing Defense and Aerospace Investments

Increasing defense modernization programs and rising global military expenditure are significantly boosting demand for aramid fibers used in ballistic protection systems, combat helmets, body armor, armored vehicles, aircraft structures, and aerospace composites. Para-aramid fibers offer an exceptional strength-to-weight ratio, outstanding impact resistance, and superior thermal stability, making them indispensable for advanced defense applications. Simultaneously, the aerospace industry continues to increase the adoption of aramid-reinforced composite materials to reduce aircraft weight, improve fuel efficiency, and enhance structural durability.

Expanding Use in Industrial Friction and Reinforcement Applications

Aramid fibers are increasingly replacing traditional reinforcement materials such as steel and asbestos in industrial applications including brake pads, clutch plates, gaskets, conveyor belts, seals, and friction materials. Their excellent wear resistance, dimensional stability, high-temperature performance, and long operational life improve equipment reliability while reducing maintenance requirements. Growing industrial automation, manufacturing expansion, and demand for durable engineering materials continue to strengthen the market for aramid fiber-based industrial components.

Increasing Adoption in Telecommunications and Advanced Composite Materials

Rapid expansion of global telecommunications infrastructure and high-performance composite applications is creating new opportunities for aramid fiber manufacturers. Aramid yarns provide excellent tensile strength for optical fiber cables, while advanced composite materials are increasingly utilized in drones, wind turbine blades, sporting equipment, marine applications, and industrial machinery. Rising investments in 5G infrastructure, renewable energy projects, and advanced engineering applications continue to expand the commercial adoption of aramid fibers beyond traditional markets.

High Production Costs and Complex Manufacturing Processes

The production of aramid fibers involves sophisticated chemical synthesis and specialized wet-spinning or dry-spinning manufacturing processes that require advanced equipment, stringent process control, and significant energy consumption. These technically demanding production methods substantially increase manufacturing costs compared to conventional synthetic fibers, limiting widespread adoption in cost-sensitive applications and emerging markets. High capital investment requirements also create barriers for new manufacturers entering the industry.

Dependence on Specialized Raw Materials

Aramid fiber manufacturing depends on specialized aromatic polyamide chemicals and high-purity raw materials such as p-phenylenediamine (PPD) and related intermediates. Disruptions in global chemical supply chains, geopolitical uncertainties, fluctuations in raw material prices, and limited supplier availability can significantly affect production costs and supply stability. This dependence on specialized feedstocks continues to represent a key challenge for manufacturers operating in the global aramid fiber market.

Competition from Alternative High-Performance Materials

The market faces increasing competition from alternative advanced materials including carbon fiber, fiberglass, and ultra-high molecular weight polyethylene (UHMWPE) fibers such as Dyneema® and Spectra®. These materials offer attractive strength-to-weight characteristics, lower production costs in certain applications, and expanding commercial availability. In industries where cost optimization is a primary consideration, these alternatives are increasingly competing with aramid fibers, particularly in automotive, industrial, and sporting goods applications.

Material Processing and Performance Limitations

Although aramid fibers exhibit exceptional mechanical properties, they remain susceptible to ultraviolet (UV) radiation, moisture absorption, and long-term environmental degradation without appropriate protective treatments. Additionally, manufacturing and processing aramid composites require specialized weaving, coating, bonding, and finishing techniques that demand skilled expertise and advanced production infrastructure. These technical complexities increase manufacturing costs and may limit adoption in regions with less-developed composite manufacturing capabilities.

North America represents one of the largest and most technologically advanced markets for aramid fibers, driven by strong demand from the aerospace, defense, automotive, and industrial sectors. The United States leads regional consumption through extensive use of para-aramid fibers in ballistic protection systems, military vehicles, aircraft structures, high-performance composites, and tire reinforcement, while meta-aramid fibers are widely utilized in flame-resistant protective clothing, electrical insulation, and high-temperature industrial applications. Increasing investments in defense modernization, aerospace innovation, lightweight automotive materials, and advanced composite manufacturing continue to strengthen regional demand. Growing emphasis on worker safety, stringent regulatory standards, and continuous technological innovation are expected to support sustained market growth across North America.

Europe remains a mature and innovation-driven aramid fiber market, supported by advanced automotive manufacturing, aerospace engineering, industrial safety regulations, and renewable energy investments. Germany, France, the United Kingdom, and Scandinavian countries are leading adopters of aramid-reinforced composites used in electric vehicles, railway systems, wind turbine blades, protective equipment, and high-performance industrial applications. Strong regional focus on sustainability has encouraged investments in recyclable aramid materials, environmentally responsible manufacturing processes, and hybrid composite technologies combining aramid, carbon fiber, and glass fiber. Continued research and development activities, coupled with strict environmental and safety regulations, are expected to drive long-term demand for advanced aramid fiber solutions across Europe.

Asia-Pacific dominates the global Aramid Fiber Market owing to rapid industrialization, expanding automotive production, growing defense expenditure, and increasing manufacturing capacity for advanced materials. China, Japan, South Korea, and India continue expanding domestic production of both para-aramid and meta-aramid fibers to satisfy rising demand from defense equipment, automotive friction materials, industrial filtration, electrical insulation, and protective apparel industries. Competitive manufacturing costs, expanding technical textile production, government support for domestic manufacturing, and increasing adoption of lightweight composite materials continue to strengthen the region's global leadership. The rapid growth of electric vehicle manufacturing and industrial automation further accelerates regional market expansion.

Latin America is witnessing gradual growth in the aramid fiber market, supported by increasing investments in automotive manufacturing, mining, industrial safety, and infrastructure development. Countries including Brazil, Mexico, and Chile are expanding the use of aramid-reinforced products across personal protective equipment (PPE), industrial hoses, conveyor belts, friction materials, and safety textiles. International manufacturers are strengthening their regional presence through partnerships, distribution networks, and localized processing facilities to better serve growing industrial demand. Although market penetration remains relatively modest, expanding industrial activity and stronger workplace safety standards are expected to support long-term market development.

The Middle East & Africa region is steadily emerging as an important growth market for aramid fibers, driven by rising investments in defense, oil & gas, industrial manufacturing, and infrastructure development. Countries across the Gulf Cooperation Council (GCC) and South Africa are increasingly utilizing aramid-based protective clothing, high-temperature insulation materials, industrial cables, and flame-resistant textiles to improve operational safety in demanding environments. Expanding distributor networks, regional manufacturing partnerships, and growing awareness of advanced protective materials are strengthening market accessibility. As industrial diversification and defense modernization programs continue across the region, demand for high-performance aramid fiber products is expected to grow steadily.

The United States remains the largest market for aramid fibers, supported by substantial investments in defense modernization, aerospace manufacturing, homeland security, and advanced industrial applications. Rising defense budgets and increasing procurement of lightweight ballistic protection systems, military aircraft, armored vehicles, and missile technologies continue to drive strong demand for para-aramid fibers. Major aerospace manufacturing hubs across California, Texas, Ohio, and Washington utilize aramid composites extensively in aircraft structures, high-performance cables, protective systems, and lightweight engineering applications. Products such as Kevlar® remain essential components in military body armor, combat helmets, aircraft interiors, and high-strength composite materials.

The country is also investing heavily in next-generation aramid technologies capable of delivering enhanced thermal stability, impact resistance, lightweight performance, and multifunctional capabilities. Strategic collaborations between leading manufacturers, defense agencies, aerospace companies, and research institutions are accelerating the development of advanced para-aramid and meta-aramid fibers designed for future military, aerospace, electric vehicle, and industrial applications. Continued investment in domestic manufacturing capacity and advanced materials research is expected to reinforce the United States' leadership within the global aramid fiber industry.

Germany has emerged as one of Europe's leading consumers of aramid fibers, driven primarily by its globally competitive automotive industry and growing emphasis on lightweight engineering for electric mobility. Automotive manufacturers are increasingly utilizing aramid-reinforced composites in battery enclosures, airbag systems, thermal insulation, structural components, brake systems, and noise-dampening materials to improve vehicle safety, efficiency, and overall performance. The country's strong commitment to reducing vehicle emissions and improving battery efficiency continues to accelerate demand for lightweight, high-strength composite materials.

Leading automotive manufacturing regions including Baden-Württemberg, Bavaria, and Lower Saxony continue investing in advanced composite technologies that incorporate aramid fibers into next-generation electric vehicles and transportation systems. Simultaneously, German manufacturers are strengthening research into recyclable composite materials, fire-resistant engineering solutions, and hybrid reinforcement systems to support sustainable mobility objectives. Continuous collaboration between automotive OEMs, material innovators, and research institutions is expected to further expand aramid fiber applications across transportation, aerospace, industrial manufacturing, and renewable energy sectors.

Japan continues to strengthen its position within the global Aramid Fiber Market through technological leadership, advanced manufacturing capabilities, and continuous innovation in high-performance materials. The country's automotive, aerospace, electronics, and industrial sectors increasingly utilize aramid fibers in flame-resistant protective clothing, electrical insulation systems, optical fiber reinforcement, high-performance composites, and lightweight structural applications. Japanese manufacturers emphasize superior product quality, precision engineering, and continuous research to develop next-generation aramid materials offering improved durability, thermal resistance, and processing efficiency.

The rapid expansion of electric vehicles, advanced electronics, robotics, and industrial automation is creating new opportunities for aramid fiber applications across Japan's manufacturing sector. Companies continue investing in advanced fiber technologies, specialty composite materials, and environmentally sustainable production methods while expanding exports of high-value technical textiles and engineering materials. Through continuous innovation and strong industrial expertise, Japan remains a key contributor to the global advancement of high-performance aramid fiber technologies.

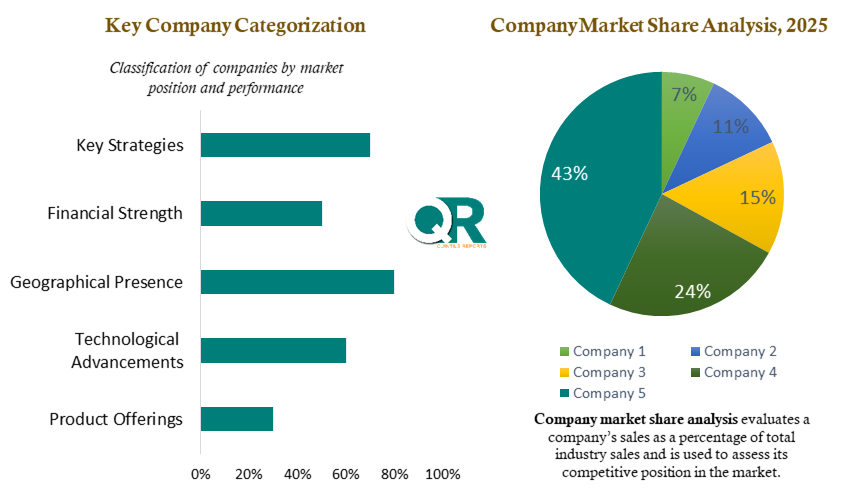

The global Aramid Fiber Market is characterized by moderate market consolidation, with a limited number of manufacturers possessing the technological expertise and production capabilities required to manufacture high-performance para-aramid and meta-aramid fibers. Competition is primarily driven by product performance, application-specific innovation, manufacturing scale, and long-term partnerships with OEMs operating across defense, aerospace, automotive, industrial, and protective equipment industries. Leading manufacturers continue investing in advanced fiber engineering, specialty product development, and capacity expansion to strengthen their competitive position in high-value end-use markets.

Technological innovation remains one of the strongest competitive differentiators across the industry. Companies are developing next-generation aramid fibers with enhanced tensile strength, thermal stability, flexibility, impact resistance, and lightweight characteristics for demanding applications such as ballistic body armor, aerospace composites, electric vehicle battery protection, industrial filtration, optical fiber reinforcement, and high-performance automotive components. Continuous research into multifunctional composites, resin compatibility, advanced coatings, and specialty fiber grades enables manufacturers to address evolving performance requirements while expanding aramid applications into emerging industries including electric mobility, renewable energy, telecommunications, and advanced electronics.

Manufacturing efficiency and production scalability have become increasingly important competitive factors as global demand continues to expand. Major manufacturers are investing in highly automated production facilities, vertical integration strategies, advanced spinning technologies, and capacity expansion projects to improve production efficiency, reduce manufacturing costs, and enhance supply reliability. These investments enable producers to deliver consistent product quality while supporting growing demand from both traditional defense applications and rapidly expanding commercial industries such as automotive, industrial manufacturing, and advanced composites.

Sustainability has emerged as another critical area of competitive differentiation. Manufacturers are increasingly investing in environmentally responsible production processes, recycled feedstocks, circular economy initiatives, and lower-carbon manufacturing technologies to address growing regulatory requirements and customer expectations. Recycling programs for aramid fibers, development of bio-based raw materials, improved resource efficiency, and transparent environmental reporting are strengthening manufacturers' ESG performance while creating new opportunities in environmentally conscious markets. Companies capable of combining high-performance materials with sustainable manufacturing practices are expected to gain long-term competitive advantages.

Regional manufacturing diversification and strategic partnerships continue to shape the competitive landscape. While Asia-Pacific remains the largest production and consumption hub for aramid fibers, manufacturers across North America and Europe are expanding domestic production capabilities to improve supply chain resilience, reduce lead times, and support localized manufacturing strategies. Strategic collaborations with automotive OEMs, aerospace manufacturers, defense organizations, and industrial equipment producers are accelerating product innovation and enabling suppliers to develop customized fiber solutions for rapidly evolving end-use applications.

Key market participants include: DuPont de Nemours, Inc., Teijin Limited, Kolon Industries Inc., Hyosung Corporation, Yantai Tayho Advanced Materials Co., Ltd., Toray Industries, Inc., Huvis Corporation, China National Bluestar Group Co., Ltd., SRO Aramid (Jiangsu) Co., Ltd., JSC Kamenskvolokno, Guangdong Charming Company, Kermel, Aramid HPM LLC, and other global and regional manufacturers.

Recent strategic developments demonstrate the industry's continued focus on sustainability, advanced material innovation, and operational optimization. In March 2024, Teijin Aramid received the Tire Technology International Materials Innovation of the Year Award for its Twaron® aramid fiber containing recycled content. The award recognized the company's ability to deliver high-performance tire reinforcement materials while advancing circular economy initiatives and reducing the environmental footprint of aramid fiber production.

In April 2023, DuPont introduced Kevlar® EXO™, the company's most significant aramid fiber innovation in more than five decades. The next-generation material combines superior ballistic protection with exceptional flexibility and lightweight performance, offering enhanced protection for military personnel, law enforcement, and first responders while expanding opportunities across advanced industrial and transportation applications.

In November 2024, Teijin Aramid announced a strategic organizational restructuring program that includes approximately 15% workforce optimization and the potential closure of its Arnhem production facility. The initiative is designed to improve operational efficiency, strengthen competitiveness, optimize manufacturing capacity, and focus investments on high-growth applications and emerging markets, reinforcing the company's long-term profitability and strategic market position.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 8.81 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Type |

|

| The Segment Covered by Application |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report has been prepared by a team of experienced advanced materials analysts, specialty fiber researchers, composite materials specialists, and industrial market experts with extensive expertise in high-performance fibers, engineered materials, defense technologies, aerospace composites, automotive lightweighting, and industrial manufacturing. Combining deep industry knowledge with advanced market research methodologies, the team delivers comprehensive insights into production trends, technological innovations, regulatory developments, competitive dynamics, and long-term growth opportunities shaping the global Aramid Fiber Market.

Leveraging a robust research framework that integrates primary interviews, secondary intelligence, quantitative market modeling, and expert validation, our analysts continuously monitor developments across the entire aramid fiber value chain—from raw material sourcing and fiber manufacturing to yarn and fabric processing, composite production, industrial applications, and end-use industries. The report also evaluates emerging trends including next-generation para-aramid and meta-aramid fibers, lightweight composite materials, ballistic protection systems, EV battery insulation, industrial filtration media, sustainable manufacturing technologies, and recycling initiatives influencing the future of the global aramid fiber industry.

Our commitment to analytical excellence, data integrity, and objective market assessment ensures that every market estimate, forecast, and strategic insight is supported by credible industry sources and rigorous validation processes. The intelligence presented in this report is designed to help aramid fiber manufacturers, composite material producers, automotive OEMs, aerospace companies, defense organizations, industrial equipment manufacturers, investors, policymakers, and other industry stakeholders identify emerging opportunities, evaluate competitive positioning, optimize investment strategies, and make informed long-term business decisions within the global Aramid Fiber Market.

The global Aramid Fiber Market was valued at USD 4.98 billion in 2026 and is projected to reach USD 11.88 billion by 2036, expanding at a CAGR of 8.81% during the forecast period. Aramid fibers are among the world's most advanced high-performance synthetic materials, valued for their exceptional tensile strength, lightweight properties, heat resistance, flame retardancy, and superior chemical stability. Available primarily as para-aramid and meta-aramid fibers, these materials play a critical role in applications requiring high durability and protection across defense, aerospace, automotive, industrial manufacturing, telecommunications, electrical insulation, and personal protective equipment. Growing demand for lightweight composite materials, increasing defense modernization programs, and rising adoption of advanced protective solutions are significantly accelerating market expansion worldwide.

The market is also benefiting from rapid technological advancements in fiber engineering, sustainable manufacturing processes, and next-generation composite materials. Increasing utilization of aramid fibers in electric vehicles, battery protection systems, lightweight automotive components, industrial filtration, friction materials, wind energy, and high-performance sporting goods is creating new avenues for growth. Furthermore, continuous investments by leading manufacturers in production capacity expansion, specialty fiber development, recycling technologies, and environmentally sustainable production methods are strengthening the long-term outlook for the global Aramid Fiber Market.

Market growth is driven by increasing demand from defense, aerospace, electric vehicles, industrial safety equipment, lightweight composites, and advanced manufacturing applications.

According to Quintile Reports' analysts, rising demand for lightweight composite materials, increasing defense modernization programs, and expanding electric vehicle production will continue to drive long-term growth in the Aramid Fiber Market. Advances in recyclable aramid materials, next-generation para-aramid fibers, and sustainable manufacturing technologies are expected to create new opportunities for manufacturers across defense, aerospace, automotive, and industrial applications.

Rising Demand for Lightweight Automotive Components

The automotive industry is increasingly adopting aramid fibers to manufacture lightweight, high-strength components such as belts, hoses, tires, brake pads, gaskets, clutch facings, and heat shields. Their exceptional mechanical strength, abrasion resistance, and thermal stability enable manufacturers to reduce vehicle weight while improving fuel efficiency and overall performance. The accelerating transition toward electric vehicles (EVs), high-performance sports cars, and stricter emission regulations is further driving the demand for advanced aramid fiber composites across the global automotive sector.

Growing Defense and Aerospace Investments

Increasing defense modernization programs and rising global military expenditure are significantly boosting demand for aramid fibers used in ballistic protection systems, combat helmets, body armor, armored vehicles, aircraft structures, and aerospace composites. Para-aramid fibers offer an exceptional strength-to-weight ratio, outstanding impact resistance, and superior thermal stability, making them indispensable for advanced defense applications. Simultaneously, the aerospace industry continues to increase the adoption of aramid-reinforced composite materials to reduce aircraft weight, improve fuel efficiency, and enhance structural durability.

Expanding Use in Industrial Friction and Reinforcement Applications

Aramid fibers are increasingly replacing traditional reinforcement materials such as steel and asbestos in industrial applications including brake pads, clutch plates, gaskets, conveyor belts, seals, and friction materials. Their excellent wear resistance, dimensional stability, high-temperature performance, and long operational life improve equipment reliability while reducing maintenance requirements. Growing industrial automation, manufacturing expansion, and demand for durable engineering materials continue to strengthen the market for aramid fiber-based industrial components.

Increasing Adoption in Telecommunications and Advanced Composite Materials

Rapid expansion of global telecommunications infrastructure and high-performance composite applications is creating new opportunities for aramid fiber manufacturers. Aramid yarns provide excellent tensile strength for optical fiber cables, while advanced composite materials are increasingly utilized in drones, wind turbine blades, sporting equipment, marine applications, and industrial machinery. Rising investments in 5G infrastructure, renewable energy projects, and advanced engineering applications continue to expand the commercial adoption of aramid fibers beyond traditional markets.

High Production Costs and Complex Manufacturing Processes

The production of aramid fibers involves sophisticated chemical synthesis and specialized wet-spinning or dry-spinning manufacturing processes that require advanced equipment, stringent process control, and significant energy consumption. These technically demanding production methods substantially increase manufacturing costs compared to conventional synthetic fibers, limiting widespread adoption in cost-sensitive applications and emerging markets. High capital investment requirements also create barriers for new manufacturers entering the industry.

Dependence on Specialized Raw Materials

Aramid fiber manufacturing depends on specialized aromatic polyamide chemicals and high-purity raw materials such as p-phenylenediamine (PPD) and related intermediates. Disruptions in global chemical supply chains, geopolitical uncertainties, fluctuations in raw material prices, and limited supplier availability can significantly affect production costs and supply stability. This dependence on specialized feedstocks continues to represent a key challenge for manufacturers operating in the global aramid fiber market.

Competition from Alternative High-Performance Materials

The market faces increasing competition from alternative advanced materials including carbon fiber, fiberglass, and ultra-high molecular weight polyethylene (UHMWPE) fibers such as Dyneema® and Spectra®. These materials offer attractive strength-to-weight characteristics, lower production costs in certain applications, and expanding commercial availability. In industries where cost optimization is a primary consideration, these alternatives are increasingly competing with aramid fibers, particularly in automotive, industrial, and sporting goods applications.

Material Processing and Performance Limitations

Although aramid fibers exhibit exceptional mechanical properties, they remain susceptible to ultraviolet (UV) radiation, moisture absorption, and long-term environmental degradation without appropriate protective treatments. Additionally, manufacturing and processing aramid composites require specialized weaving, coating, bonding, and finishing techniques that demand skilled expertise and advanced production infrastructure. These technical complexities increase manufacturing costs and may limit adoption in regions with less-developed composite manufacturing capabilities.

North America represents one of the largest and most technologically advanced markets for aramid fibers, driven by strong demand from the aerospace, defense, automotive, and industrial sectors. The United States leads regional consumption through extensive use of para-aramid fibers in ballistic protection systems, military vehicles, aircraft structures, high-performance composites, and tire reinforcement, while meta-aramid fibers are widely utilized in flame-resistant protective clothing, electrical insulation, and high-temperature industrial applications. Increasing investments in defense modernization, aerospace innovation, lightweight automotive materials, and advanced composite manufacturing continue to strengthen regional demand. Growing emphasis on worker safety, stringent regulatory standards, and continuous technological innovation are expected to support sustained market growth across North America.

Europe remains a mature and innovation-driven aramid fiber market, supported by advanced automotive manufacturing, aerospace engineering, industrial safety regulations, and renewable energy investments. Germany, France, the United Kingdom, and Scandinavian countries are leading adopters of aramid-reinforced composites used in electric vehicles, railway systems, wind turbine blades, protective equipment, and high-performance industrial applications. Strong regional focus on sustainability has encouraged investments in recyclable aramid materials, environmentally responsible manufacturing processes, and hybrid composite technologies combining aramid, carbon fiber, and glass fiber. Continued research and development activities, coupled with strict environmental and safety regulations, are expected to drive long-term demand for advanced aramid fiber solutions across Europe.

Asia-Pacific dominates the global Aramid Fiber Market owing to rapid industrialization, expanding automotive production, growing defense expenditure, and increasing manufacturing capacity for advanced materials. China, Japan, South Korea, and India continue expanding domestic production of both para-aramid and meta-aramid fibers to satisfy rising demand from defense equipment, automotive friction materials, industrial filtration, electrical insulation, and protective apparel industries. Competitive manufacturing costs, expanding technical textile production, government support for domestic manufacturing, and increasing adoption of lightweight composite materials continue to strengthen the region's global leadership. The rapid growth of electric vehicle manufacturing and industrial automation further accelerates regional market expansion.

Latin America is witnessing gradual growth in the aramid fiber market, supported by increasing investments in automotive manufacturing, mining, industrial safety, and infrastructure development. Countries including Brazil, Mexico, and Chile are expanding the use of aramid-reinforced products across personal protective equipment (PPE), industrial hoses, conveyor belts, friction materials, and safety textiles. International manufacturers are strengthening their regional presence through partnerships, distribution networks, and localized processing facilities to better serve growing industrial demand. Although market penetration remains relatively modest, expanding industrial activity and stronger workplace safety standards are expected to support long-term market development.

The Middle East & Africa region is steadily emerging as an important growth market for aramid fibers, driven by rising investments in defense, oil & gas, industrial manufacturing, and infrastructure development. Countries across the Gulf Cooperation Council (GCC) and South Africa are increasingly utilizing aramid-based protective clothing, high-temperature insulation materials, industrial cables, and flame-resistant textiles to improve operational safety in demanding environments. Expanding distributor networks, regional manufacturing partnerships, and growing awareness of advanced protective materials are strengthening market accessibility. As industrial diversification and defense modernization programs continue across the region, demand for high-performance aramid fiber products is expected to grow steadily.

The United States remains the largest market for aramid fibers, supported by substantial investments in defense modernization, aerospace manufacturing, homeland security, and advanced industrial applications. Rising defense budgets and increasing procurement of lightweight ballistic protection systems, military aircraft, armored vehicles, and missile technologies continue to drive strong demand for para-aramid fibers. Major aerospace manufacturing hubs across California, Texas, Ohio, and Washington utilize aramid composites extensively in aircraft structures, high-performance cables, protective systems, and lightweight engineering applications. Products such as Kevlar® remain essential components in military body armor, combat helmets, aircraft interiors, and high-strength composite materials.

The country is also investing heavily in next-generation aramid technologies capable of delivering enhanced thermal stability, impact resistance, lightweight performance, and multifunctional capabilities. Strategic collaborations between leading manufacturers, defense agencies, aerospace companies, and research institutions are accelerating the development of advanced para-aramid and meta-aramid fibers designed for future military, aerospace, electric vehicle, and industrial applications. Continued investment in domestic manufacturing capacity and advanced materials research is expected to reinforce the United States' leadership within the global aramid fiber industry.

Germany has emerged as one of Europe's leading consumers of aramid fibers, driven primarily by its globally competitive automotive industry and growing emphasis on lightweight engineering for electric mobility. Automotive manufacturers are increasingly utilizing aramid-reinforced composites in battery enclosures, airbag systems, thermal insulation, structural components, brake systems, and noise-dampening materials to improve vehicle safety, efficiency, and overall performance. The country's strong commitment to reducing vehicle emissions and improving battery efficiency continues to accelerate demand for lightweight, high-strength composite materials.

Leading automotive manufacturing regions including Baden-Württemberg, Bavaria, and Lower Saxony continue investing in advanced composite technologies that incorporate aramid fibers into next-generation electric vehicles and transportation systems. Simultaneously, German manufacturers are strengthening research into recyclable composite materials, fire-resistant engineering solutions, and hybrid reinforcement systems to support sustainable mobility objectives. Continuous collaboration between automotive OEMs, material innovators, and research institutions is expected to further expand aramid fiber applications across transportation, aerospace, industrial manufacturing, and renewable energy sectors.

Japan continues to strengthen its position within the global Aramid Fiber Market through technological leadership, advanced manufacturing capabilities, and continuous innovation in high-performance materials. The country's automotive, aerospace, electronics, and industrial sectors increasingly utilize aramid fibers in flame-resistant protective clothing, electrical insulation systems, optical fiber reinforcement, high-performance composites, and lightweight structural applications. Japanese manufacturers emphasize superior product quality, precision engineering, and continuous research to develop next-generation aramid materials offering improved durability, thermal resistance, and processing efficiency.

The rapid expansion of electric vehicles, advanced electronics, robotics, and industrial automation is creating new opportunities for aramid fiber applications across Japan's manufacturing sector. Companies continue investing in advanced fiber technologies, specialty composite materials, and environmentally sustainable production methods while expanding exports of high-value technical textiles and engineering materials. Through continuous innovation and strong industrial expertise, Japan remains a key contributor to the global advancement of high-performance aramid fiber technologies.

The global Aramid Fiber Market is characterized by moderate market consolidation, with a limited number of manufacturers possessing the technological expertise and production capabilities required to manufacture high-performance para-aramid and meta-aramid fibers. Competition is primarily driven by product performance, application-specific innovation, manufacturing scale, and long-term partnerships with OEMs operating across defense, aerospace, automotive, industrial, and protective equipment industries. Leading manufacturers continue investing in advanced fiber engineering, specialty product development, and capacity expansion to strengthen their competitive position in high-value end-use markets.

Technological innovation remains one of the strongest competitive differentiators across the industry. Companies are developing next-generation aramid fibers with enhanced tensile strength, thermal stability, flexibility, impact resistance, and lightweight characteristics for demanding applications such as ballistic body armor, aerospace composites, electric vehicle battery protection, industrial filtration, optical fiber reinforcement, and high-performance automotive components. Continuous research into multifunctional composites, resin compatibility, advanced coatings, and specialty fiber grades enables manufacturers to address evolving performance requirements while expanding aramid applications into emerging industries including electric mobility, renewable energy, telecommunications, and advanced electronics.

Manufacturing efficiency and production scalability have become increasingly important competitive factors as global demand continues to expand. Major manufacturers are investing in highly automated production facilities, vertical integration strategies, advanced spinning technologies, and capacity expansion projects to improve production efficiency, reduce manufacturing costs, and enhance supply reliability. These investments enable producers to deliver consistent product quality while supporting growing demand from both traditional defense applications and rapidly expanding commercial industries such as automotive, industrial manufacturing, and advanced composites.

Sustainability has emerged as another critical area of competitive differentiation. Manufacturers are increasingly investing in environmentally responsible production processes, recycled feedstocks, circular economy initiatives, and lower-carbon manufacturing technologies to address growing regulatory requirements and customer expectations. Recycling programs for aramid fibers, development of bio-based raw materials, improved resource efficiency, and transparent environmental reporting are strengthening manufacturers' ESG performance while creating new opportunities in environmentally conscious markets. Companies capable of combining high-performance materials with sustainable manufacturing practices are expected to gain long-term competitive advantages.

Regional manufacturing diversification and strategic partnerships continue to shape the competitive landscape. While Asia-Pacific remains the largest production and consumption hub for aramid fibers, manufacturers across North America and Europe are expanding domestic production capabilities to improve supply chain resilience, reduce lead times, and support localized manufacturing strategies. Strategic collaborations with automotive OEMs, aerospace manufacturers, defense organizations, and industrial equipment producers are accelerating product innovation and enabling suppliers to develop customized fiber solutions for rapidly evolving end-use applications.

Key market participants include: DuPont de Nemours, Inc., Teijin Limited, Kolon Industries Inc., Hyosung Corporation, Yantai Tayho Advanced Materials Co., Ltd., Toray Industries, Inc., Huvis Corporation, China National Bluestar Group Co., Ltd., SRO Aramid (Jiangsu) Co., Ltd., JSC Kamenskvolokno, Guangdong Charming Company, Kermel, Aramid HPM LLC, and other global and regional manufacturers.

Recent strategic developments demonstrate the industry's continued focus on sustainability, advanced material innovation, and operational optimization. In March 2024, Teijin Aramid received the Tire Technology International Materials Innovation of the Year Award for its Twaron® aramid fiber containing recycled content. The award recognized the company's ability to deliver high-performance tire reinforcement materials while advancing circular economy initiatives and reducing the environmental footprint of aramid fiber production.

In April 2023, DuPont introduced Kevlar® EXO™, the company's most significant aramid fiber innovation in more than five decades. The next-generation material combines superior ballistic protection with exceptional flexibility and lightweight performance, offering enhanced protection for military personnel, law enforcement, and first responders while expanding opportunities across advanced industrial and transportation applications.

In November 2024, Teijin Aramid announced a strategic organizational restructuring program that includes approximately 15% workforce optimization and the potential closure of its Arnhem production facility. The initiative is designed to improve operational efficiency, strengthen competitiveness, optimize manufacturing capacity, and focus investments on high-growth applications and emerging markets, reinforcing the company's long-term profitability and strategic market position.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 8.81 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Type |

|

| The Segment Covered by Application |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report has been prepared by a team of experienced advanced materials analysts, specialty fiber researchers, composite materials specialists, and industrial market experts with extensive expertise in high-performance fibers, engineered materials, defense technologies, aerospace composites, automotive lightweighting, and industrial manufacturing. Combining deep industry knowledge with advanced market research methodologies, the team delivers comprehensive insights into production trends, technological innovations, regulatory developments, competitive dynamics, and long-term growth opportunities shaping the global Aramid Fiber Market.

Leveraging a robust research framework that integrates primary interviews, secondary intelligence, quantitative market modeling, and expert validation, our analysts continuously monitor developments across the entire aramid fiber value chain—from raw material sourcing and fiber manufacturing to yarn and fabric processing, composite production, industrial applications, and end-use industries. The report also evaluates emerging trends including next-generation para-aramid and meta-aramid fibers, lightweight composite materials, ballistic protection systems, EV battery insulation, industrial filtration media, sustainable manufacturing technologies, and recycling initiatives influencing the future of the global aramid fiber industry.

Our commitment to analytical excellence, data integrity, and objective market assessment ensures that every market estimate, forecast, and strategic insight is supported by credible industry sources and rigorous validation processes. The intelligence presented in this report is designed to help aramid fiber manufacturers, composite material producers, automotive OEMs, aerospace companies, defense organizations, industrial equipment manufacturers, investors, policymakers, and other industry stakeholders identify emerging opportunities, evaluate competitive positioning, optimize investment strategies, and make informed long-term business decisions within the global Aramid Fiber Market.

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 9 Germany Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 21 China Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Aramid Fiber Market: Market Scenario

Fig.4 Global Aramid Fiber Market Competitive Outlook

Fig.5 Global Aramid Fiber Market Driver Analysis

Fig.6 Global Aramid Fiber Market Restraint Analysis

Fig.7 Global Aramid Fiber Market Opportunity Analysis

Fig.8 Global Aramid Fiber Market Trends Analysis

Fig.9 Global Aramid Fiber Market: Segment Analysis (Based on the Scope)

Fig.10 Global Aramid Fiber Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 9 Germany Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 21 China Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Aramid Fiber Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Aramid Fiber Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Aramid Fiber Market: Market Scenario

Fig.4 Global Aramid Fiber Market Competitive Outlook

Fig.5 Global Aramid Fiber Market Driver Analysis

Fig.6 Global Aramid Fiber Market Restraint Analysis

Fig.7 Global Aramid Fiber Market Opportunity Analysis

Fig.8 Global Aramid Fiber Market Trends Analysis

Fig.9 Global Aramid Fiber Market: Segment Analysis (Based on the Scope)

Fig.10 Global Aramid Fiber Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

The global Aramid Fiber Market was valued at USD 4.98 billion in 2026 and is projected to reach USD 11.88 billion by 2036.

Asia-Pacific dominates the global market, driven by rapid industrialization, expanding automotive manufacturing, increasing defense expenditure, and strong investments in advanced composite materials across China, Japan, South Korea, and India.

Para-aramid fiber accounts for the largest market share due to its exceptional strength-to-weight ratio, impact resistance, and extensive use in ballistic protection, aerospace components, automotive parts, and high-performance industrial applications.

Protective fabrics and security & defense applications lead global demand, supported by the increasing use of aramid fibers in body armor, combat helmets, flame-resistant clothing, aerospace composites, and industrial protective equipment.

Leading market participants include DuPont de Nemours, Inc., Teijin Limited, Kolon Industries Inc., Hyosung Corporation, Toray Industries, Inc., Huvis Corporation, China National Bluestar Group Co., Ltd., SRO Aramid (Jiangsu) Co., Ltd., JSC Kamenskvolokno, Guangdong Charming Company, Kermel, and Aramid HPM LLC.

Market growth is primarily driven by increasing defense modernization programs, rising aerospace production, expanding electric vehicle manufacturing, growing demand for lightweight composite materials, industrial safety regulations, and continuous technological advancements in high-performance fibers.

Key challenges include high production costs, dependence on specialized raw materials, competition from alternative high-performance materials such as carbon fiber and UHMWPE, and the technical complexities associated with processing and manufacturing aramid fiber composites.

The global Aramid Fiber Market was valued at USD 4.98 billion in 2026 and is projected to reach USD 11.88 billion by 2036, expanding at a CAGR of 8.81% during the forecast period. Aramid fibers are among the world's most advanced high-performance synthetic materials, valued for their exceptional tensile strength, lightweight properties, heat resistance, flame retardancy, and superior chemical stability. Available primarily as para-aramid and meta-aramid fibers, these materials play a critical role in applications requiring high durability and protection across defense, aerospace, automotive, industrial manufacturing, telecommunications, electrical insulation, and personal protective equipment. Growing demand for lightweight composite materials, increasing defense modernization programs, and rising adoption of advanced protective solutions are significantly accelerating market expansion worldwide.

The market is also benefiting from rapid technological advancements in fiber engineering, sustainable manufacturing processes, and next-generation composite materials. Increasing utilization of aramid fibers in electric vehicles, battery protection systems, lightweight automotive components, industrial filtration, friction materials, wind energy, and high-performance sporting goods is creating new avenues for growth. Furthermore, continuous investments by leading manufacturers in production capacity expansion, specialty fiber development, recycling technologies, and environmentally sustainable production methods are strengthening the long-term outlook for the global Aramid Fiber Market.

Market growth is driven by increasing demand from defense, aerospace, electric vehicles, industrial safety equipment, lightweight composites, and advanced manufacturing applications.

According to Quintile Reports' analysts, rising demand for lightweight composite materials, increasing defense modernization programs, and expanding electric vehicle production will continue to drive long-term growth in the Aramid Fiber Market. Advances in recyclable aramid materials, next-generation para-aramid fibers, and sustainable manufacturing technologies are expected to create new opportunities for manufacturers across defense, aerospace, automotive, and industrial applications.

Rising Demand for Lightweight Automotive Components

The automotive industry is increasingly adopting aramid fibers to manufacture lightweight, high-strength components such as belts, hoses, tires, brake pads, gaskets, clutch facings, and heat shields. Their exceptional mechanical strength, abrasion resistance, and thermal stability enable manufacturers to reduce vehicle weight while improving fuel efficiency and overall performance. The accelerating transition toward electric vehicles (EVs), high-performance sports cars, and stricter emission regulations is further driving the demand for advanced aramid fiber composites across the global automotive sector.

Growing Defense and Aerospace Investments

Increasing defense modernization programs and rising global military expenditure are significantly boosting demand for aramid fibers used in ballistic protection systems, combat helmets, body armor, armored vehicles, aircraft structures, and aerospace composites. Para-aramid fibers offer an exceptional strength-to-weight ratio, outstanding impact resistance, and superior thermal stability, making them indispensable for advanced defense applications. Simultaneously, the aerospace industry continues to increase the adoption of aramid-reinforced composite materials to reduce aircraft weight, improve fuel efficiency, and enhance structural durability.

Expanding Use in Industrial Friction and Reinforcement Applications

Aramid fibers are increasingly replacing traditional reinforcement materials such as steel and asbestos in industrial applications including brake pads, clutch plates, gaskets, conveyor belts, seals, and friction materials. Their excellent wear resistance, dimensional stability, high-temperature performance, and long operational life improve equipment reliability while reducing maintenance requirements. Growing industrial automation, manufacturing expansion, and demand for durable engineering materials continue to strengthen the market for aramid fiber-based industrial components.

Increasing Adoption in Telecommunications and Advanced Composite Materials

Rapid expansion of global telecommunications infrastructure and high-performance composite applications is creating new opportunities for aramid fiber manufacturers. Aramid yarns provide excellent tensile strength for optical fiber cables, while advanced composite materials are increasingly utilized in drones, wind turbine blades, sporting equipment, marine applications, and industrial machinery. Rising investments in 5G infrastructure, renewable energy projects, and advanced engineering applications continue to expand the commercial adoption of aramid fibers beyond traditional markets.

High Production Costs and Complex Manufacturing Processes

The production of aramid fibers involves sophisticated chemical synthesis and specialized wet-spinning or dry-spinning manufacturing processes that require advanced equipment, stringent process control, and significant energy consumption. These technically demanding production methods substantially increase manufacturing costs compared to conventional synthetic fibers, limiting widespread adoption in cost-sensitive applications and emerging markets. High capital investment requirements also create barriers for new manufacturers entering the industry.

Dependence on Specialized Raw Materials

Aramid fiber manufacturing depends on specialized aromatic polyamide chemicals and high-purity raw materials such as p-phenylenediamine (PPD) and related intermediates. Disruptions in global chemical supply chains, geopolitical uncertainties, fluctuations in raw material prices, and limited supplier availability can significantly affect production costs and supply stability. This dependence on specialized feedstocks continues to represent a key challenge for manufacturers operating in the global aramid fiber market.

Competition from Alternative High-Performance Materials

The market faces increasing competition from alternative advanced materials including carbon fiber, fiberglass, and ultra-high molecular weight polyethylene (UHMWPE) fibers such as Dyneema® and Spectra®. These materials offer attractive strength-to-weight characteristics, lower production costs in certain applications, and expanding commercial availability. In industries where cost optimization is a primary consideration, these alternatives are increasingly competing with aramid fibers, particularly in automotive, industrial, and sporting goods applications.

Material Processing and Performance Limitations

Although aramid fibers exhibit exceptional mechanical properties, they remain susceptible to ultraviolet (UV) radiation, moisture absorption, and long-term environmental degradation without appropriate protective treatments. Additionally, manufacturing and processing aramid composites require specialized weaving, coating, bonding, and finishing techniques that demand skilled expertise and advanced production infrastructure. These technical complexities increase manufacturing costs and may limit adoption in regions with less-developed composite manufacturing capabilities.

North America represents one of the largest and most technologically advanced markets for aramid fibers, driven by strong demand from the aerospace, defense, automotive, and industrial sectors. The United States leads regional consumption through extensive use of para-aramid fibers in ballistic protection systems, military vehicles, aircraft structures, high-performance composites, and tire reinforcement, while meta-aramid fibers are widely utilized in flame-resistant protective clothing, electrical insulation, and high-temperature industrial applications. Increasing investments in defense modernization, aerospace innovation, lightweight automotive materials, and advanced composite manufacturing continue to strengthen regional demand. Growing emphasis on worker safety, stringent regulatory standards, and continuous technological innovation are expected to support sustained market growth across North America.

Europe remains a mature and innovation-driven aramid fiber market, supported by advanced automotive manufacturing, aerospace engineering, industrial safety regulations, and renewable energy investments. Germany, France, the United Kingdom, and Scandinavian countries are leading adopters of aramid-reinforced composites used in electric vehicles, railway systems, wind turbine blades, protective equipment, and high-performance industrial applications. Strong regional focus on sustainability has encouraged investments in recyclable aramid materials, environmentally responsible manufacturing processes, and hybrid composite technologies combining aramid, carbon fiber, and glass fiber. Continued research and development activities, coupled with strict environmental and safety regulations, are expected to drive long-term demand for advanced aramid fiber solutions across Europe.

Asia-Pacific dominates the global Aramid Fiber Market owing to rapid industrialization, expanding automotive production, growing defense expenditure, and increasing manufacturing capacity for advanced materials. China, Japan, South Korea, and India continue expanding domestic production of both para-aramid and meta-aramid fibers to satisfy rising demand from defense equipment, automotive friction materials, industrial filtration, electrical insulation, and protective apparel industries. Competitive manufacturing costs, expanding technical textile production, government support for domestic manufacturing, and increasing adoption of lightweight composite materials continue to strengthen the region's global leadership. The rapid growth of electric vehicle manufacturing and industrial automation further accelerates regional market expansion.

Latin America is witnessing gradual growth in the aramid fiber market, supported by increasing investments in automotive manufacturing, mining, industrial safety, and infrastructure development. Countries including Brazil, Mexico, and Chile are expanding the use of aramid-reinforced products across personal protective equipment (PPE), industrial hoses, conveyor belts, friction materials, and safety textiles. International manufacturers are strengthening their regional presence through partnerships, distribution networks, and localized processing facilities to better serve growing industrial demand. Although market penetration remains relatively modest, expanding industrial activity and stronger workplace safety standards are expected to support long-term market development.

The Middle East & Africa region is steadily emerging as an important growth market for aramid fibers, driven by rising investments in defense, oil & gas, industrial manufacturing, and infrastructure development. Countries across the Gulf Cooperation Council (GCC) and South Africa are increasingly utilizing aramid-based protective clothing, high-temperature insulation materials, industrial cables, and flame-resistant textiles to improve operational safety in demanding environments. Expanding distributor networks, regional manufacturing partnerships, and growing awareness of advanced protective materials are strengthening market accessibility. As industrial diversification and defense modernization programs continue across the region, demand for high-performance aramid fiber products is expected to grow steadily.

The United States remains the largest market for aramid fibers, supported by substantial investments in defense modernization, aerospace manufacturing, homeland security, and advanced industrial applications. Rising defense budgets and increasing procurement of lightweight ballistic protection systems, military aircraft, armored vehicles, and missile technologies continue to drive strong demand for para-aramid fibers. Major aerospace manufacturing hubs across California, Texas, Ohio, and Washington utilize aramid composites extensively in aircraft structures, high-performance cables, protective systems, and lightweight engineering applications. Products such as Kevlar® remain essential components in military body armor, combat helmets, aircraft interiors, and high-strength composite materials.

The country is also investing heavily in next-generation aramid technologies capable of delivering enhanced thermal stability, impact resistance, lightweight performance, and multifunctional capabilities. Strategic collaborations between leading manufacturers, defense agencies, aerospace companies, and research institutions are accelerating the development of advanced para-aramid and meta-aramid fibers designed for future military, aerospace, electric vehicle, and industrial applications. Continued investment in domestic manufacturing capacity and advanced materials research is expected to reinforce the United States' leadership within the global aramid fiber industry.

Germany has emerged as one of Europe's leading consumers of aramid fibers, driven primarily by its globally competitive automotive industry and growing emphasis on lightweight engineering for electric mobility. Automotive manufacturers are increasingly utilizing aramid-reinforced composites in battery enclosures, airbag systems, thermal insulation, structural components, brake systems, and noise-dampening materials to improve vehicle safety, efficiency, and overall performance. The country's strong commitment to reducing vehicle emissions and improving battery efficiency continues to accelerate demand for lightweight, high-strength composite materials.

Leading automotive manufacturing regions including Baden-Württemberg, Bavaria, and Lower Saxony continue investing in advanced composite technologies that incorporate aramid fibers into next-generation electric vehicles and transportation systems. Simultaneously, German manufacturers are strengthening research into recyclable composite materials, fire-resistant engineering solutions, and hybrid reinforcement systems to support sustainable mobility objectives. Continuous collaboration between automotive OEMs, material innovators, and research institutions is expected to further expand aramid fiber applications across transportation, aerospace, industrial manufacturing, and renewable energy sectors.

Japan continues to strengthen its position within the global Aramid Fiber Market through technological leadership, advanced manufacturing capabilities, and continuous innovation in high-performance materials. The country's automotive, aerospace, electronics, and industrial sectors increasingly utilize aramid fibers in flame-resistant protective clothing, electrical insulation systems, optical fiber reinforcement, high-performance composites, and lightweight structural applications. Japanese manufacturers emphasize superior product quality, precision engineering, and continuous research to develop next-generation aramid materials offering improved durability, thermal resistance, and processing efficiency.

The rapid expansion of electric vehicles, advanced electronics, robotics, and industrial automation is creating new opportunities for aramid fiber applications across Japan's manufacturing sector. Companies continue investing in advanced fiber technologies, specialty composite materials, and environmentally sustainable production methods while expanding exports of high-value technical textiles and engineering materials. Through continuous innovation and strong industrial expertise, Japan remains a key contributor to the global advancement of high-performance aramid fiber technologies.

The global Aramid Fiber Market is characterized by moderate market consolidation, with a limited number of manufacturers possessing the technological expertise and production capabilities required to manufacture high-performance para-aramid and meta-aramid fibers. Competition is primarily driven by product performance, application-specific innovation, manufacturing scale, and long-term partnerships with OEMs operating across defense, aerospace, automotive, industrial, and protective equipment industries. Leading manufacturers continue investing in advanced fiber engineering, specialty product development, and capacity expansion to strengthen their competitive position in high-value end-use markets.

Technological innovation remains one of the strongest competitive differentiators across the industry. Companies are developing next-generation aramid fibers with enhanced tensile strength, thermal stability, flexibility, impact resistance, and lightweight characteristics for demanding applications such as ballistic body armor, aerospace composites, electric vehicle battery protection, industrial filtration, optical fiber reinforcement, and high-performance automotive components. Continuous research into multifunctional composites, resin compatibility, advanced coatings, and specialty fiber grades enables manufacturers to address evolving performance requirements while expanding aramid applications into emerging industries including electric mobility, renewable energy, telecommunications, and advanced electronics.