The global Silicon Carbide (SiC) Market was valued at USD 7.52 billion in 2026 and is projected to reach USD 21.47 billion by 2036, registering a robust CAGR of 10.41% during the forecast period. Silicon carbide has emerged as one of the most strategically important advanced materials owing to its exceptional thermal conductivity, wide bandgap, high breakdown voltage, and superior mechanical strength. These characteristics make SiC indispensable across high-performance power electronics, electric vehicles, renewable energy systems, industrial automation, aerospace, defense, and next-generation semiconductor applications.

The market has evolved significantly from its traditional applications in abrasives and refractory materials to becoming a critical enabling technology for modern electrification and energy-efficient systems. Increasing investments in electric mobility, fast-charging infrastructure, AI data centers, smart grids, and high-voltage power conversion are driving widespread adoption of silicon carbide devices. Continuous advancements in wafer manufacturing, crystal growth technologies, substrate quality, and semiconductor fabrication are further strengthening the market's long-term growth outlook.

Market growth is driven by rapid electric vehicle adoption, renewable energy expansion, semiconductor manufacturing investments, industrial automation, and increasing deployment of wide-bandgap semiconductor technologies.

Asia-Pacific dominates the global market due to extensive semiconductor manufacturing, electric vehicle production, and strong investments in wafer fabrication facilities.

North America is witnessing rapid growth driven by AI data centers, EV manufacturing, renewable energy deployment, and domestic semiconductor production initiatives.

Europe continues to expand through automotive electrification, industrial automation, railway electrification, and clean energy infrastructure investments.

Japan, China, South Korea, and Taiwan remain major innovation hubs for silicon carbide wafer manufacturing and advanced power semiconductor technologies.

Middle East & Africa and Latin America are emerging markets supported by renewable energy projects, industrial modernization, and growing adoption of power electronics.

The rapid transition toward electrification and digital infrastructure is fundamentally reshaping demand for silicon carbide technologies. Compared with conventional silicon-based semiconductors, SiC devices deliver significantly higher switching efficiency, lower energy losses, improved thermal management, and superior performance under high-voltage operating conditions. These advantages are making silicon carbide the preferred material for electric vehicle traction inverters, onboard chargers, renewable energy inverters, industrial motor drives, and high-frequency telecommunications equipment.

Growing investments in artificial intelligence infrastructure, hyperscale data centers, and advanced semiconductor manufacturing are creating additional opportunities for silicon carbide adoption. The industry's transition toward larger 200 mm wafers, improved crystal quality, and vertically integrated manufacturing is expected to enhance production scalability while reducing costs, enabling broader commercialization across both industrial and consumer applications.

Rapid Expansion of Electric Vehicle Production

The increasing adoption of electric vehicles worldwide is significantly driving demand for silicon carbide power semiconductors. SiC devices improve power conversion efficiency, extend driving range, enable faster charging, and reduce energy losses, making them essential components in traction inverters, onboard chargers, and battery management systems.

Growing Investments in Renewable Energy Infrastructure

Expanding deployment of solar power, wind energy, and energy storage systems is accelerating the use of silicon carbide-based power electronics. SiC semiconductors enhance inverter efficiency, improve grid reliability, and support high-voltage power conversion required for modern renewable energy applications.

Rising Demand for High-Efficiency Power Electronics

Industries are increasingly adopting silicon carbide devices to improve energy efficiency, reduce operational costs, and support electrification initiatives. The superior thermal conductivity, high switching frequency, and low power losses offered by SiC technology are driving widespread adoption across industrial automation, telecommunications, aerospace, and defense.

Expansion of AI Data Centers and Semiconductor Manufacturing

Growing investments in artificial intelligence infrastructure, hyperscale data centers, and advanced semiconductor fabrication are creating significant demand for silicon carbide components used in power management, cooling systems, and high-performance computing infrastructure.

High Manufacturing Costs

Silicon carbide wafer production requires complex crystal growth processes, advanced manufacturing technologies, and precision fabrication, resulting in higher production costs compared with conventional silicon semiconductors.

Limited Wafer Supply and Manufacturing Capacity

The availability of high-quality silicon carbide substrates remains relatively limited, creating supply constraints as demand continues to increase across automotive, industrial, and renewable energy sectors.

Technical Complexity in Manufacturing

Producing defect-free silicon carbide wafers requires specialized equipment, advanced process control, and significant research and development investments, posing challenges for new market entrants.

High Initial Adoption Costs

Although silicon carbide offers long-term efficiency benefits, its higher upfront component costs may slow adoption among cost-sensitive industries and applications.

Transition to 200 mm Silicon Carbide Wafers

The industry's shift toward 200 mm wafer manufacturing is expected to improve production efficiency, increase manufacturing capacity, reduce costs, and support large-scale commercialization of silicon carbide devices.

Expansion of Fast-Charging Infrastructure

Growing investments in high-power EV charging networks are creating new opportunities for silicon carbide power modules capable of delivering faster charging, higher efficiency, and improved thermal performance.

Industrial Automation and Smart Manufacturing

The increasing adoption of robotics, industrial automation, and smart manufacturing technologies is expanding demand for silicon carbide power electronics in motor drives, power supplies, and industrial control systems.

Government Support for Domestic Semiconductor Manufacturing

Government incentive programs, semiconductor localization initiatives, and investments in domestic chip manufacturing are creating favorable conditions for silicon carbide production capacity expansion and long-term market growth.

The United States continues to lead the global Silicon Carbide (SiC) Market, supported by rapid expansion of artificial intelligence (AI) infrastructure, electric vehicle manufacturing, renewable energy deployment, and domestic semiconductor production. The increasing construction of hyperscale AI data centers and high-performance computing (HPC) facilities has created substantial demand for SiC-based power semiconductors capable of delivering superior energy efficiency, faster switching frequencies, and improved thermal management. These devices play a critical role in power conversion systems, server power supplies, cooling infrastructure, and high-voltage electrical distribution within next-generation computing environments.

The country is also strengthening its domestic SiC manufacturing ecosystem through significant investments in wafer fabrication, crystal growth technologies, and vertically integrated semiconductor production. Major manufacturing hubs across North Carolina, Texas, Arizona, and California continue to expand production capacity to support growing demand from electric vehicles, industrial automation, aerospace, and defense applications. Government initiatives promoting semiconductor localization and supply chain resilience are further reinforcing the United States' position as one of the world's leading centers for silicon carbide innovation and commercial production.

Germany has emerged as one of Europe's most important silicon carbide markets, driven by its globally competitive automotive industry, advanced manufacturing capabilities, and commitment to industrial decarbonization. The rapid transition toward electric mobility has significantly increased demand for SiC-based power electronics used in traction inverters, onboard chargers, DC fast-charging systems, and battery management solutions. Compared with conventional silicon devices, silicon carbide semiconductors improve vehicle efficiency, extend driving range, and enable faster charging while reducing system weight and energy losses.

Leading automotive manufacturers and semiconductor companies are investing heavily in next-generation SiC technologies, including 200 mm wafer production, advanced MOSFETs, Schottky barrier diodes, and high-voltage power modules. Germany's strong collaboration between automotive OEMs, semiconductor manufacturers, research institutions, and government-supported innovation programs continues to accelerate commercialization of advanced silicon carbide technologies. Growing investments in renewable energy, industrial automation, railway electrification, and smart manufacturing are further expanding application opportunities across multiple industrial sectors.

Japan continues to strengthen its position as a global leader in silicon carbide innovation through its advanced semiconductor manufacturing ecosystem, precision engineering expertise, and continuous investment in wide-bandgap semiconductor technologies. Silicon carbide has become increasingly important across semiconductor fabrication equipment, industrial automation systems, power control applications, robotics, and high-performance electronic devices due to its exceptional thermal conductivity, high voltage tolerance, and operational reliability under extreme conditions.

Japanese manufacturers are expanding production of high-purity silicon carbide substrates, epitaxial wafers, and advanced semiconductor materials to support domestic chip manufacturing and global export demand. Significant investments in 150 mm and 200 mm SiC wafer technologies are improving production efficiency while supporting the development of next-generation power semiconductors for electric vehicles, renewable energy systems, industrial equipment, and telecommunications infrastructure. Government initiatives focused on strengthening domestic semiconductor supply chains, increasing research and development, and enhancing manufacturing competitiveness continue to reinforce Japan's strategic role in the global silicon carbide industry. Through continuous technological innovation and collaboration between semiconductor companies, equipment manufacturers, and research institutions, Japan remains a key driver of future advancements in high-performance silicon carbide technologies.

The Silicon Carbide (SiC) Market is highly technology-intensive, with competition centered on device performance, wafer quality, manufacturing scalability, and application-specific innovation. As demand for high-efficiency power electronics accelerates across electric vehicles, renewable energy systems, industrial automation, aerospace, and telecommunications, manufacturers are focusing on developing next-generation SiC MOSFETs, Schottky diodes, power modules, and high-voltage semiconductor devices capable of delivering superior thermal conductivity, faster switching speeds, and lower energy losses. Companies offering high-reliability products for demanding applications continue to strengthen their competitive position.

Manufacturing capability has emerged as another critical competitive differentiator. Leading market participants are investing heavily in advanced crystal growth technologies, defect reduction techniques, epitaxial wafer production, and the transition from 150 mm to 200 mm silicon carbide wafers. Larger wafer formats improve manufacturing yields, reduce production costs, and enable higher-volume semiconductor fabrication, supporting broader adoption across automotive, industrial, and consumer electronics markets. Companies capable of scaling production while maintaining superior wafer quality are expected to gain long-term market advantages.

Supply chain resilience and regional manufacturing expansion have become increasingly important amid geopolitical uncertainties and growing semiconductor localization initiatives. Major manufacturers are establishing new fabrication facilities, expanding regional production capacity, and forming strategic partnerships across North America, Europe, and Asia-Pacific to reduce supply chain risks and strengthen access to critical semiconductor materials. Government-backed programs supporting domestic semiconductor manufacturing, including incentive schemes and industrial investment policies, are further accelerating capacity expansion and regional diversification.

Innovation remains at the core of market competition, with companies investing significantly in research and development, intellectual property portfolios, and collaborative product development. Strategic partnerships between semiconductor manufacturers, automotive OEMs, renewable energy companies, industrial equipment suppliers, and research institutions are accelerating commercialization of advanced silicon carbide technologies while reducing development cycles. In addition, growing emphasis on sustainable manufacturing, low-carbon production processes, and energy-efficient fabrication technologies is creating new opportunities for competitive differentiation as environmental performance becomes increasingly important across the semiconductor value chain.

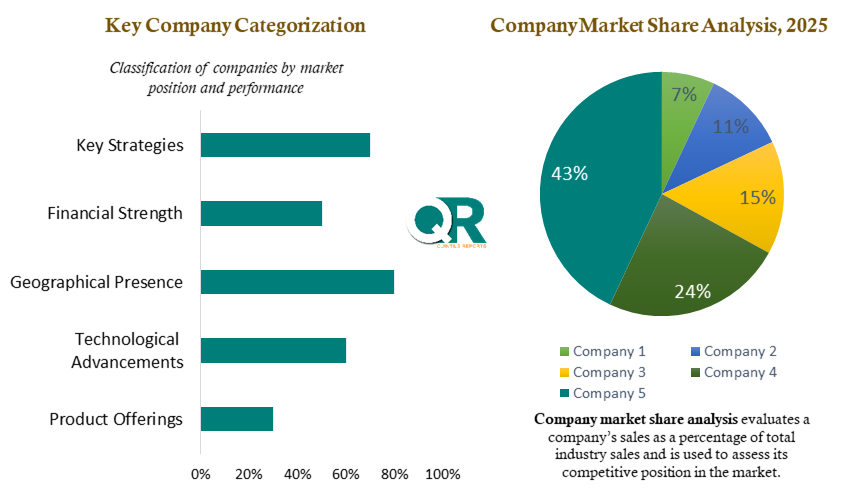

Key market participants include Wolfspeed, Inc., Infineon Technologies AG, ON Semiconductor, STMicroelectronics N.V., ROHM Co., Ltd., Fuji Electric Co., Ltd., General Electric, Toshiba Corporation, Renesas Electronics Corporation, Microchip Technology Inc., Mitsubishi Electric Corporation, Norstel AB, Dow Inc., Silicon Carbide Products, Inc., Grindwell Norton Ltd., and other global and regional semiconductor manufacturers.

Recent strategic developments demonstrate the industry's strong focus on manufacturing scale, electric vehicle innovation, and sustainable semiconductor production. In February 2025, Infineon Technologies AG announced the commercial readiness of its 200 mm (8-inch) silicon carbide wafer manufacturing platform, with initial product deliveries targeting renewable energy systems, electric vehicles, and railway applications. Simultaneously, the company continued expanding its manufacturing operations in Malaysia to support high-volume production and improve manufacturing efficiency.

In June 2025, Infineon Technologies AG partnered with Tata Elxsi to jointly develop application-ready electric vehicle solutions for the Indian market. The collaboration integrates advanced silicon carbide technologies into high-voltage traction inverters, battery management systems, and onboard charging platforms, highlighting the growing role of SiC semiconductors in next-generation electric mobility.

In July 2025, Resonac Holdings Corporation and Tohoku University initiated collaborative research focused on manufacturing silicon carbide semiconductor materials using waste silicon and captured carbon dioxide through advanced carbon recycling technologies. The initiative aims to significantly reduce carbon emissions associated with SiC production while supporting sustainable semiconductor manufacturing. During the same period, Resonac also announced progress in developing 8-inch silicon carbide epitaxial wafer technology, reinforcing the industry's transition toward larger wafer platforms and more efficient large-scale semiconductor production.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 10.41 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Product Type |

|

| The Segment Covered by Device Type |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report delivers a comprehensive and evidence-based assessment of the global Silicon Carbide (SiC) Market, combining extensive primary research with in-depth secondary analysis to provide accurate, reliable, and actionable market intelligence. The research draws upon insights from semiconductor manufacturers, silicon carbide wafer producers, power electronics suppliers, automotive OEMs, renewable energy developers, technology providers, distributors, and industry experts to present a balanced view of current market dynamics and future growth prospects.

The study evaluates the complete silicon carbide value chain, including raw material sourcing, crystal growth, substrate manufacturing, epitaxial wafer production, semiconductor device fabrication, module packaging, and end-use applications across electric vehicles, renewable energy, industrial automation, aerospace, telecommunications, and high-performance computing. Each market estimate is validated using production capacity assessments, wafer shipment analysis, semiconductor demand trends, investment activity, and regional manufacturing developments to ensure a high level of analytical accuracy.

The report also incorporates detailed analysis of technological advancements such as 200 mm silicon carbide wafer commercialization, next-generation MOSFET and Schottky diode development, wide-bandgap semiconductor innovation, and sustainable manufacturing initiatives. In addition, evolving government policies, semiconductor incentive programs, electric vehicle adoption, renewable energy investments, and supply chain localization strategies are thoroughly assessed to provide forward-looking market insights.

Using advanced forecasting models, data triangulation techniques, and expert validation, this report offers dependable market projections and strategic intelligence that support product development, investment planning, capacity expansion, competitive benchmarking, and long-term business decision-making. It serves as a trusted resource for manufacturers, investors, technology providers, policymakers, and other stakeholders seeking to capitalize on the rapidly evolving opportunities within the global Silicon Carbide Market.

This study on the Silicon Carbide Market was developed using a comprehensive research framework that integrates primary research, secondary intelligence gathering, and advanced quantitative analysis to deliver accurate and reliable market insights. The research process began with an extensiv

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 9 Germany Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 21 China Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Silicon Carbide Market: Market Scenario

Fig.4 Global Silicon Carbide Market Competitive Outlook

Fig.5 Global Silicon Carbide Market Driver Analysis

Fig.6 Global Silicon Carbide Market Restraint Analysis

Fig.7 Global Silicon Carbide Market Opportunity Analysis

Fig.8 Global Silicon Carbide Market Trends Analysis

Fig.9 Global Silicon Carbide Market: Segment Analysis (Based on the Scope)

Fig.10 Global Silicon Carbide Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 9 Germany Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 21 China Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Silicon Carbide Market: Market Scenario

Fig.4 Global Silicon Carbide Market Competitive Outlook

Fig.5 Global Silicon Carbide Market Driver Analysis

Fig.6 Global Silicon Carbide Market Restraint Analysis

Fig.7 Global Silicon Carbide Market Opportunity Analysis

Fig.8 Global Silicon Carbide Market Trends Analysis

Fig.9 Global Silicon Carbide Market: Segment Analysis (Based on the Scope)

Fig.10 Global Silicon Carbide Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Silicon Carbide (SiC) is a wide-bandgap semiconductor material known for its exceptional thermal conductivity, high breakdown voltage, and superior energy efficiency. It is widely used in power electronics, electric vehicles, renewable energy systems, industrial automation, and aerospace applications.

Silicon Carbide enables faster switching speeds, lower power losses, and higher operating temperatures than traditional silicon semiconductors. These advantages improve energy efficiency and performance in electric vehicles, fast chargers, renewable energy inverters, and AI data centers.

Major industries using Silicon Carbide include automotive, renewable energy, industrial automation, aerospace & defense, telecommunications, consumer electronics, healthcare, and semiconductor manufacturing.

Electric vehicle manufacturers use SiC power devices because they improve driving range, enable faster charging, reduce energy losses, and enhance the efficiency of traction inverters and onboard charging systems.

A 200 mm SiC wafer is the latest generation of semiconductor substrate that enables higher production efficiency, lower manufacturing costs, and greater scalability for power semiconductor devices.

Asia-Pacific dominates the Silicon Carbide Market due to its strong semiconductor manufacturing ecosystem, rapid electric vehicle production, and extensive investments in power electronics.

The market is primarily driven by increasing EV adoption, renewable energy expansion, AI data center investments, industrial automation, and government support for domestic semiconductor manufacturing.

The global Silicon Carbide Market is expected to grow at a CAGR of 10.41% between 2026 and 2036.

The global Silicon Carbide (SiC) Market was valued at USD 7.52 billion in 2026 and is projected to reach USD 21.47 billion by 2036, registering a robust CAGR of 10.41% during the forecast period. Silicon carbide has emerged as one of the most strategically important advanced materials owing to its exceptional thermal conductivity, wide bandgap, high breakdown voltage, and superior mechanical strength. These characteristics make SiC indispensable across high-performance power electronics, electric vehicles, renewable energy systems, industrial automation, aerospace, defense, and next-generation semiconductor applications.

The market has evolved significantly from its traditional applications in abrasives and refractory materials to becoming a critical enabling technology for modern electrification and energy-efficient systems. Increasing investments in electric mobility, fast-charging infrastructure, AI data centers, smart grids, and high-voltage power conversion are driving widespread adoption of silicon carbide devices. Continuous advancements in wafer manufacturing, crystal growth technologies, substrate quality, and semiconductor fabrication are further strengthening the market's long-term growth outlook.

Market growth is driven by rapid electric vehicle adoption, renewable energy expansion, semiconductor manufacturing investments, industrial automation, and increasing deployment of wide-bandgap semiconductor technologies.

Asia-Pacific dominates the global market due to extensive semiconductor manufacturing, electric vehicle production, and strong investments in wafer fabrication facilities.

North America is witnessing rapid growth driven by AI data centers, EV manufacturing, renewable energy deployment, and domestic semiconductor production initiatives.

Europe continues to expand through automotive electrification, industrial automation, railway electrification, and clean energy infrastructure investments.

Japan, China, South Korea, and Taiwan remain major innovation hubs for silicon carbide wafer manufacturing and advanced power semiconductor technologies.

Middle East & Africa and Latin America are emerging markets supported by renewable energy projects, industrial modernization, and growing adoption of power electronics.

The rapid transition toward electrification and digital infrastructure is fundamentally reshaping demand for silicon carbide technologies. Compared with conventional silicon-based semiconductors, SiC devices deliver significantly higher switching efficiency, lower energy losses, improved thermal management, and superior performance under high-voltage operating conditions. These advantages are making silicon carbide the preferred material for electric vehicle traction inverters, onboard chargers, renewable energy inverters, industrial motor drives, and high-frequency telecommunications equipment.

Growing investments in artificial intelligence infrastructure, hyperscale data centers, and advanced semiconductor manufacturing are creating additional opportunities for silicon carbide adoption. The industry's transition toward larger 200 mm wafers, improved crystal quality, and vertically integrated manufacturing is expected to enhance production scalability while reducing costs, enabling broader commercialization across both industrial and consumer applications.

Rapid Expansion of Electric Vehicle Production

The increasing adoption of electric vehicles worldwide is significantly driving demand for silicon carbide power semiconductors. SiC devices improve power conversion efficiency, extend driving range, enable faster charging, and reduce energy losses, making them essential components in traction inverters, onboard chargers, and battery management systems.

Growing Investments in Renewable Energy Infrastructure

Expanding deployment of solar power, wind energy, and energy storage systems is accelerating the use of silicon carbide-based power electronics. SiC semiconductors enhance inverter efficiency, improve grid reliability, and support high-voltage power conversion required for modern renewable energy applications.

Rising Demand for High-Efficiency Power Electronics

Industries are increasingly adopting silicon carbide devices to improve energy efficiency, reduce operational costs, and support electrification initiatives. The superior thermal conductivity, high switching frequency, and low power losses offered by SiC technology are driving widespread adoption across industrial automation, telecommunications, aerospace, and defense.

Expansion of AI Data Centers and Semiconductor Manufacturing

Growing investments in artificial intelligence infrastructure, hyperscale data centers, and advanced semiconductor fabrication are creating significant demand for silicon carbide components used in power management, cooling systems, and high-performance computing infrastructure.

High Manufacturing Costs

Silicon carbide wafer production requires complex crystal growth processes, advanced manufacturing technologies, and precision fabrication, resulting in higher production costs compared with conventional silicon semiconductors.

Limited Wafer Supply and Manufacturing Capacity

The availability of high-quality silicon carbide substrates remains relatively limited, creating supply constraints as demand continues to increase across automotive, industrial, and renewable energy sectors.

Technical Complexity in Manufacturing

Producing defect-free silicon carbide wafers requires specialized equipment, advanced process control, and significant research and development investments, posing challenges for new market entrants.

High Initial Adoption Costs

Although silicon carbide offers long-term efficiency benefits, its higher upfront component costs may slow adoption among cost-sensitive industries and applications.

Transition to 200 mm Silicon Carbide Wafers

The industry's shift toward 200 mm wafer manufacturing is expected to improve production efficiency, increase manufacturing capacity, reduce costs, and support large-scale commercialization of silicon carbide devices.

Expansion of Fast-Charging Infrastructure

Growing investments in high-power EV charging networks are creating new opportunities for silicon carbide power modules capable of delivering faster charging, higher efficiency, and improved thermal performance.

Industrial Automation and Smart Manufacturing

The increasing adoption of robotics, industrial automation, and smart manufacturing technologies is expanding demand for silicon carbide power electronics in motor drives, power supplies, and industrial control systems.

Government Support for Domestic Semiconductor Manufacturing

Government incentive programs, semiconductor localization initiatives, and investments in domestic chip manufacturing are creating favorable conditions for silicon carbide production capacity expansion and long-term market growth.

The United States continues to lead the global Silicon Carbide (SiC) Market, supported by rapid expansion of artificial intelligence (AI) infrastructure, electric vehicle manufacturing, renewable energy deployment, and domestic semiconductor production. The increasing construction of hyperscale AI data centers and high-performance computing (HPC) facilities has created substantial demand for SiC-based power semiconductors capable of delivering superior energy efficiency, faster switching frequencies, and improved thermal management. These devices play a critical role in power conversion systems, server power supplies, cooling infrastructure, and high-voltage electrical distribution within next-generation computing environments.

The country is also strengthening its domestic SiC manufacturing ecosystem through significant investments in wafer fabrication, crystal growth technologies, and vertically integrated semiconductor production. Major manufacturing hubs across North Carolina, Texas, Arizona, and California continue to expand production capacity to support growing demand from electric vehicles, industrial automation, aerospace, and defense applications. Government initiatives promoting semiconductor localization and supply chain resilience are further reinforcing the United States' position as one of the world's leading centers for silicon carbide innovation and commercial production.

Germany has emerged as one of Europe's most important silicon carbide markets, driven by its globally competitive automotive industry, advanced manufacturing capabilities, and commitment to industrial decarbonization. The rapid transition toward electric mobility has significantly increased demand for SiC-based power electronics used in traction inverters, onboard chargers, DC fast-charging systems, and battery management solutions. Compared with conventional silicon devices, silicon carbide semiconductors improve vehicle efficiency, extend driving range, and enable faster charging while reducing system weight and energy losses.

Leading automotive manufacturers and semiconductor companies are investing heavily in next-generation SiC technologies, including 200 mm wafer production, advanced MOSFETs, Schottky barrier diodes, and high-voltage power modules. Germany's strong collaboration between automotive OEMs, semiconductor manufacturers, research institutions, and government-supported innovation programs continues to accelerate commercialization of advanced silicon carbide technologies. Growing investments in renewable energy, industrial automation, railway electrification, and smart manufacturing are further expanding application opportunities across multiple industrial sectors.

Japan continues to strengthen its position as a global leader in silicon carbide innovation through its advanced semiconductor manufacturing ecosystem, precision engineering expertise, and continuous investment in wide-bandgap semiconductor technologies. Silicon carbide has become increasingly important across semiconductor fabrication equipment, industrial automation systems, power control applications, robotics, and high-performance electronic devices due to its exceptional thermal conductivity, high voltage tolerance, and operational reliability under extreme conditions.

Japanese manufacturers are expanding production of high-purity silicon carbide substrates, epitaxial wafers, and advanced semiconductor materials to support domestic chip manufacturing and global export demand. Significant investments in 150 mm and 200 mm SiC wafer technologies are improving production efficiency while supporting the development of next-generation power semiconductors for electric vehicles, renewable energy systems, industrial equipment, and telecommunications infrastructure. Government initiatives focused on strengthening domestic semiconductor supply chains, increasing research and development, and enhancing manufacturing competitiveness continue to reinforce Japan's strategic role in the global silicon carbide industry. Through continuous technological innovation and collaboration between semiconductor companies, equipment manufacturers, and research institutions, Japan remains a key driver of future advancements in high-performance silicon carbide technologies.

The Silicon Carbide (SiC) Market is highly technology-intensive, with competition centered on device performance, wafer quality, manufacturing scalability, and application-specific innovation. As demand for high-efficiency power electronics accelerates across electric vehicles, renewable energy systems, industrial automation, aerospace, and telecommunications, manufacturers are focusing on developing next-generation SiC MOSFETs, Schottky diodes, power modules, and high-voltage semiconductor devices capable of delivering superior thermal conductivity, faster switching speeds, and lower energy losses. Companies offering high-reliability products for demanding applications continue to strengthen their competitive position.

Manufacturing capability has emerged as another critical competitive differentiator. Leading market participants are investing heavily in advanced crystal growth technologies, defect reduction techniques, epitaxial wafer production, and the transition from 150 mm to 200 mm silicon carbide wafers. Larger wafer formats improve manufacturing yields, reduce production costs, and enable higher-volume semiconductor fabrication, supporting broader adoption across automotive, industrial, and consumer electronics markets. Companies capable of scaling production while maintaining superior wafer quality are expected to gain long-term market advantages.

Supply chain resilience and regional manufacturing expansion have become increasingly important amid geopolitical uncertainties and growing semiconductor localization initiatives. Major manufacturers are establishing new fabrication facilities, expanding regional production capacity, and forming strategic partnerships across North America, Europe, and Asia-Pacific to reduce supply chain risks and strengthen access to critical semiconductor materials. Government-backed programs supporting domestic semiconductor manufacturing, including incentive schemes and industrial investment policies, are further accelerating capacity expansion and regional diversification.

Innovation remains at the core of market competition, with companies investing significantly in research and development, intellectual property portfolios, and collaborative product development. Strategic partnerships between semiconductor manufacturers, automotive OEMs, renewable energy companies, industrial equipment suppliers, and research institutions are accelerating commercialization of advanced silicon carbide technologies while reducing development cycles. In addition, growing emphasis on sustainable manufacturing, low-carbon production processes, and energy-efficient fabrication technologies is creating new opportunities for competitive differentiation as environmental performance becomes increasingly important across the semiconductor value chain.

Key market participants include Wolfspeed, Inc., Infineon Technologies AG, ON Semiconductor, STMicroelectronics N.V., ROHM Co., Ltd., Fuji Electric Co., Ltd., General Electric, Toshiba Corporation, Renesas Electronics Corporation, Microchip Technology Inc., Mitsubishi Electric Corporation, Norstel AB, Dow Inc., Silicon Carbide Products, Inc., Grindwell Norton Ltd., and other global and regional semiconductor manufacturers.

Recent strategic developments demonstrate the industry's strong focus on manufacturing scale, electric vehicle innovation, and sustainable semiconductor production. In February 2025, Infineon Technologies AG announced the commercial readiness of its 200 mm (8-inch) silicon carbide wafer manufacturing platform, with initial product deliveries targeting renewable energy systems, electric vehicles, and railway applications. Simultaneously, the company continued expanding its manufacturing operations in Malaysia to support high-volume production and improve manufacturing efficiency.

In June 2025, Infineon Technologies AG partnered with Tata Elxsi to jointly develop application-ready electric vehicle solutions for the Indian market. The collaboration integrates advanced silicon carbide technologies into high-voltage traction inverters, battery management systems, and onboard charging platforms, highlighting the growing role of SiC semiconductors in next-generation electric mobility.

In July 2025, Resonac Holdings Corporation and Tohoku University initiated collaborative research focused on manufacturing silicon carbide semiconductor materials using waste silicon and captured carbon dioxide through advanced carbon recycling technologies. The initiative aims to significantly reduce carbon emissions associated with SiC production while supporting sustainable semiconductor manufacturing. During the same period, Resonac also announced progress in developing 8-inch silicon carbide epitaxial wafer technology, reinforcing the industry's transition toward larger wafer platforms and more efficient large-scale semiconductor production.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 10.41 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Product Type |

|

| The Segment Covered by Device Type |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report delivers a comprehensive and evidence-based assessment of the global Silicon Carbide (SiC) Market, combining extensive primary research with in-depth secondary analysis to provide accurate, reliable, and actionable market intelligence. The research draws upon insights from semiconductor manufacturers, silicon carbide wafer producers, power electronics suppliers, automotive OEMs, renewable energy developers, technology providers, distributors, and industry experts to present a balanced view of current market dynamics and future growth prospects.

The study evaluates the complete silicon carbide value chain, including raw material sourcing, crystal growth, substrate manufacturing, epitaxial wafer production, semiconductor device fabrication, module packaging, and end-use applications across electric vehicles, renewable energy, industrial automation, aerospace, telecommunications, and high-performance computing. Each market estimate is validated using production capacity assessments, wafer shipment analysis, semiconductor demand trends, investment activity, and regional manufacturing developments to ensure a high level of analytical accuracy.

The report also incorporates detailed analysis of technological advancements such as 200 mm silicon carbide wafer commercialization, next-generation MOSFET and Schottky diode development, wide-bandgap semiconductor innovation, and sustainable manufacturing initiatives. In addition, evolving government policies, semiconductor incentive programs, electric vehicle adoption, renewable energy investments, and supply chain localization strategies are thoroughly assessed to provide forward-looking market insights.

Using advanced forecasting models, data triangulation techniques, and expert validation, this report offers dependable market projections and strategic intelligence that support product development, investment planning, capacity expansion, competitive benchmarking, and long-term business decision-making. It serves as a trusted resource for manufacturers, investors, technology providers, policymakers, and other stakeholders seeking to capitalize on the rapidly evolving opportunities within the global Silicon Carbide Market.

This study on the Silicon Carbide Market was developed using a comprehensive research framework that integrates primary research, secondary intelligence gathering, and advanced quantitative analysis to deliver accurate and reliable market insights. The research process began with an extensiv

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 9 Germany Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 21 China Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Silicon Carbide Market: Market Scenario

Fig.4 Global Silicon Carbide Market Competitive Outlook

Fig.5 Global Silicon Carbide Market Driver Analysis

Fig.6 Global Silicon Carbide Market Restraint Analysis

Fig.7 Global Silicon Carbide Market Opportunity Analysis

Fig.8 Global Silicon Carbide Market Trends Analysis

Fig.9 Global Silicon Carbide Market: Segment Analysis (Based on the Scope)

Fig.10 Global Silicon Carbide Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 9 Germany Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 21 China Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Silicon Carbide Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Silicon Carbide Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Silicon Carbide Market: Market Scenario

Fig.4 Global Silicon Carbide Market Competitive Outlook

Fig.5 Global Silicon Carbide Market Driver Analysis

Fig.6 Global Silicon Carbide Market Restraint Analysis

Fig.7 Global Silicon Carbide Market Opportunity Analysis

Fig.8 Global Silicon Carbide Market Trends Analysis

Fig.9 Global Silicon Carbide Market: Segment Analysis (Based on the Scope)

Fig.10 Global Silicon Carbide Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

A license granted to one user. Rules or conditions might be applied for e.g. the use of electric files (PDFs) or printings, depending on product.

A license granted to multiple users.

A license granted to a single business site/establishment.

A license granted to all employees within organisation access to the product.

Immediate / Within 24-48 hours - Working days

Online Payments with PayPal and CCavenue

You can order a report by picking any of the payment methods which is bank wire or online payment through any Debit/Credit card or PayPal.

Hard Copy