The global Green Cement Market was valued at USD 49.52 billion in 2026 and is projected to reach USD 89.47 billion by 2036, growing at a CAGR of 7.71% during the forecast period. Green cement has evolved from a niche sustainable building material into a mainstream construction solution as governments, developers, and infrastructure operators increasingly prioritize carbon reduction and environmentally responsible construction practices. Unlike conventional Portland cement, green cement incorporates supplementary cementitious materials (SCMs) such as fly ash, ground granulated blast furnace slag (GGBFS), limestone, calcined clay, silica fume, and other industrial by-products to significantly reduce clinker content and lower carbon emissions.

The global cement industry is responsible for nearly 8% of worldwide carbon dioxide emissions, making decarbonization a critical priority for policymakers and industry stakeholders. Green cement offers a practical pathway toward reducing the environmental footprint of construction activities while maintaining structural performance, durability, and cost competitiveness. The market is benefiting from growing regulatory support, increasing adoption of green building certifications, carbon pricing mechanisms, and rising ESG-focused investments across residential, commercial, and infrastructure sectors.

The future outlook of the industry is increasingly influenced by three powerful forces: stricter environmental regulations, technological innovation in low-carbon cement production, and growing investor preference for sustainable construction materials. Programs such as the U.S. Buy Clean Initiative, the European Green Deal, and climate commitments under the Paris Agreement are transforming sustainability objectives into mandatory procurement requirements. Simultaneously, advancements in carbon capture utilization and storage (CCUS), clinker-free formulations, LC3 technologies, and AI-enabled manufacturing processes are reshaping the competitive landscape and accelerating the transition toward low-carbon construction materials.

Accelerated Adoption of Limestone Calcined Clay Cement (LC3)

LC3 technology is emerging as one of the most promising low-carbon cement solutions globally, capable of reducing carbon emissions by up to 40% compared to conventional Portland cement. Growing government support for sustainable infrastructure and public-sector green procurement programs is accelerating commercial deployment across developed and emerging economies. Growing investments in renewable energy infrastructure and sustainable construction materials are also supporting demand across the Solar Energy Storage Battery Market.

Carbon Capture, Utilization, and Storage (CCUS) Integration

Leading cement manufacturers are increasingly investing in CCUS technologies to significantly reduce process emissions. Major projects across Europe, North America, and Asia are demonstrating the commercial viability of carbon capture systems integrated directly into cement production facilities, helping producers move toward net-zero manufacturing targets.

ESG-Driven Financing Accelerating Market Adoption

Green bonds, sustainability-linked loans, and ESG-focused investment mandates are increasingly requiring developers and contractors to utilize low-carbon building materials. As a result, green cement is becoming an essential component of environmentally certified construction projects worldwide.

Expansion of Clinker-Free Cement Technologies

Clinker-free and ultra-low clinker formulations are gaining traction as manufacturers seek to eliminate the most carbon-intensive component of traditional cement production. Regulatory approvals and certification milestones are enabling broader adoption across infrastructure, commercial, and residential construction sectors.

Digitalization and AI-Enabled Manufacturing Optimization

Artificial intelligence, predictive analytics, and digital quality control systems are being deployed to optimize raw material blending, improve energy efficiency, reduce waste generation, and ensure consistent product performance across green cement manufacturing operations.

The Green Cement Market value chain begins with the sourcing of raw materials and supplementary cementitious materials (SCMs), which form the foundation of low-carbon cement production. Key inputs include fly ash from coal-fired power plants, ground granulated blast furnace slag (GGBFS) from steel manufacturing facilities, limestone, calcined clay, silica fume, recycled aggregates, and other industrial by-products. The availability, quality, and geographic proximity of these materials significantly influence production costs, supply chain efficiency, and the carbon footprint of final cement products. As traditional coal generation declines globally, producers are increasingly diversifying feedstock sources through alternative SCMs such as LC3 materials, reclaimed ash reserves, and innovative mineral additives.

The second stage involves cement manufacturing and processing, where producers integrate alternative materials into optimized cement formulations. Leading manufacturers are investing heavily in energy-efficient kilns, alternative fuels, carbon capture utilization and storage (CCUS) systems, digital process controls, and AI-driven quality management platforms to reduce emissions while maintaining product performance. This stage represents the largest opportunity for decarbonization, as conventional clinker production remains the most carbon-intensive component of the cement value chain. Companies capable of reducing clinker factors while maintaining strength, durability, and regulatory compliance are gaining a significant competitive advantage.

Distribution and logistics form the third stage of the value chain, encompassing bulk cement transportation, ready-mix concrete integration, regional distribution networks, and project-specific supply management. Because cement is a high-volume, low-margin product, transportation costs play a critical role in determining competitiveness. Producers increasingly establish manufacturing facilities close to urban centers, industrial hubs, and major infrastructure corridors to reduce logistics expenses and minimize transportation-related emissions. Strategic partnerships with construction firms, ready-mix suppliers, and infrastructure developers further strengthen market penetration and supply chain resilience.

The final stage consists of end-use applications across residential, commercial, industrial, and infrastructure construction sectors. Residential construction currently represents the largest demand segment, supported by green building certifications, sustainable housing initiatives, and ESG-focused development programs. Commercial buildings, transportation infrastructure, renewable energy projects, and public works increasingly specify low-carbon cement products to comply with environmental regulations and sustainability targets. Growing adoption of LEED, BREEAM, DGNB, and other green building frameworks is transforming procurement requirements and creating long-term demand for certified low-carbon construction materials.

Across the entire value chain, technology providers, carbon management companies, certification bodies, environmental consultants, and regulatory agencies play increasingly important supporting roles. Their contributions help manufacturers achieve compliance, improve environmental performance, secure sustainability certifications, and develop next-generation green cement solutions. As carbon pricing mechanisms, ESG financing, and climate regulations continue to expand globally, value creation within the green cement ecosystem is expected to shift toward innovation, emissions reduction capabilities, and lifecycle sustainability performance.

The growing focus on sustainable material science is also influencing adjacent cement applications beyond traditional construction. Advances in formulation technologies, durability enhancement, and specialty cement development are supporting innovation across sectors, including healthcare materials. Similar trends can be observed in the Dental Cement Market, where manufacturers are developing advanced bonding materials with improved performance, longevity, and environmental characteristics.

North America represents one of the most mature markets for green cement, supported by stringent environmental regulations, aggressive carbon reduction targets, and growing adoption of sustainable construction practices. The United States and Canada continue to promote low-carbon building materials through initiatives such as the U.S. EPA emission standards, the Buy Clean program, and Canada's Output-Based Pricing System. These policies are encouraging cement manufacturers to invest in carbon capture, utilization, and storage (CCUS) technologies, alternative fuels, and clinker reduction strategies. Non-residential construction remains a major demand center, driven by increasing adoption of LEED-certified buildings and public infrastructure projects that prioritize environmentally responsible materials. The United States dominates regional demand due to strong government support, a robust green building pipeline, and increasing ESG-driven procurement requirements.

Europe continues to lead global innovation in green cement production, driven by ambitious climate policies and strict emissions regulations. Frameworks such as the European Green Deal and the EU Emissions Trading System are accelerating the transition away from traditional clinker-intensive cement production toward low-carbon alternatives. Cement manufacturers across Germany, France, the United Kingdom, and Nordic countries are increasingly incorporating fly ash, slag, calcined clay, and recycled materials into production processes while simultaneously investing in CCUS technologies. The region's strong commitment to circular economy principles is encouraging greater utilization of industrial by-products and waste-derived materials. Demand remains particularly strong in infrastructure and commercial construction projects seeking compliance with BREEAM, DGNB, and other sustainability certification standards.

Asia Pacific accounts for the largest share of global green cement demand and is expected to remain the fastest-growing regional market throughout the forecast period. Rapid urbanization, large-scale infrastructure development, and increasing government support for sustainable construction are driving widespread adoption across China, India, Japan, South Korea, and Southeast Asia. The region benefits from abundant availability of supplementary cementitious materials such as fly ash and blast furnace slag, which help reduce production costs while lowering emissions. National carbon reduction targets, green infrastructure investments, and growing environmental awareness among developers are accelerating market expansion. Government-backed construction projects increasingly require low-carbon materials, creating substantial opportunities for green cement producers. Rapid infrastructure expansion and renewable energy deployment continue to create opportunities across the Distributed Solar Power Generation Market.

The Latin American green cement market is steadily expanding as governments strengthen environmental regulations and prioritize sustainable infrastructure development. Countries such as Brazil and Mexico are investing in transportation networks, affordable housing projects, and public infrastructure programs that increasingly incorporate environmentally friendly construction materials. Local cement manufacturers are gradually increasing the use of fly ash, slag, and alternative binders to reduce carbon emissions and improve sustainability performance. Although challenges related to limited technological infrastructure, inconsistent raw material availability, and fragmented regulatory frameworks remain, the long-term outlook remains positive as climate-focused investments continue to increase across the region.

The Middle East & Africa region is emerging as a promising market for green cement as governments pursue economic diversification strategies and sustainable urban development initiatives. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are promoting environmentally responsible construction through green building standards, energy-efficiency regulations, and carbon reduction programs. Large-scale smart city developments, transportation infrastructure projects, and commercial construction activities are creating demand for low-carbon cement products. While adoption is currently constrained by limited access to advanced manufacturing technologies and inconsistent availability of industrial by-products, increasing awareness of sustainable construction practices is expected to support gradual market expansion over the coming years.

The United States remains the largest market for green cement in North America, supported by strong regulatory backing, infrastructure modernization programs, and increasing adoption of sustainable building practices. Federal initiatives promoting low-carbon materials, combined with stricter emissions regulations, are encouraging construction companies and developers to incorporate green cement into both public and private sector projects. Leading manufacturers continue to invest in innovative technologies including carbon capture and storage, alternative fuel utilization, and advanced clinker substitution methods. The growing popularity of LEED-certified buildings and ESG-focused construction projects is further accelerating adoption, positioning green cement as a critical component of the nation's decarbonization strategy.

Germany continues to serve as a benchmark market for sustainable cement production and green construction practices. Government policies aligned with the Renewable Energy Sources Act and the EU's Fit for 55 program are driving significant investments in low-carbon building materials and industrial decarbonization technologies. Major producers are expanding the use of calcined clay, industrial by-products, and alternative clinker materials while simultaneously deploying CCUS technologies and energy-efficient kiln systems. Strong collaboration between government agencies, research institutions, and industry stakeholders has accelerated innovation, helping Germany maintain its leadership position in Europe's green cement transition.

Japan's green cement market is being shaped by ambitious carbon neutrality goals, advanced manufacturing capabilities, and a strong commitment to resource efficiency. Cement producers are increasingly utilizing municipal incinerator ash, recycled aggregates, construction waste, and industrial by-products to develop environmentally sustainable cement formulations. Investments in energy-efficient kiln technologies, waste valorization systems, and smart manufacturing solutions are improving production efficiency while reducing emissions. As Japan continues to strengthen its circular economy initiatives and sustainable construction policies, green cement is expected to play an increasingly important role in reducing the environmental footprint of the country's building and infrastructure sectors.

The Green Cement Market is expected to remain one of the fastest-growing segments within the sustainable construction materials industry as governments, developers, and investors prioritize carbon reduction initiatives. Adoption of LC3 technologies, carbon capture solutions, and alternative clinker formulations is expected to accelerate market transformation through 2036.

The Green Cement Market is undergoing a significant transformation as sustainability, carbon reduction performance, and regulatory compliance become primary competitive differentiators. Market participants are increasingly competing through the development of low-carbon cement formulations, alternative clinker technologies, carbon capture solutions, and circular economy initiatives rather than solely on pricing or production capacity. As governments tighten emissions regulations and construction companies adopt stricter ESG targets, manufacturers are investing heavily in technologies that reduce embodied carbon while maintaining structural performance and durability.

Leading producers are focusing on the increased utilization of supplementary cementitious materials (SCMs) such as fly ash, ground granulated blast furnace slag (GGBFS), calcined clay, silica fume, and recycled construction materials to lower clinker content and reduce lifecycle emissions. The ability to provide certified low-carbon products supported by Environmental Product Declarations (EPDs), LEED compliance, BREEAM certification compatibility, and other sustainability credentials has become a critical factor influencing purchasing decisions across residential, commercial, and infrastructure projects.

Technological innovation continues to reshape the competitive landscape. Major cement manufacturers are investing in carbon capture, utilization, and storage (CCUS) technologies, alternative fuel systems, AI-enabled process optimization, and next-generation clinker-free cement formulations. Companies that successfully integrate carbon reduction technologies while maintaining cost competitiveness and product performance are strengthening their market positions. Furthermore, strategic partnerships with governments, infrastructure developers, and green finance institutions are enabling manufacturers to capitalize on increasing demand for sustainable construction materials.

The market also benefits from growing adoption of circular economy practices, including the reuse of industrial by-products, construction waste recycling, and resource-efficient production processes. Manufacturers capable of securing reliable SCM supply chains, optimizing energy consumption, and scaling low-carbon production technologies are expected to gain long-term competitive advantages as environmental regulations continue to tighten globally.

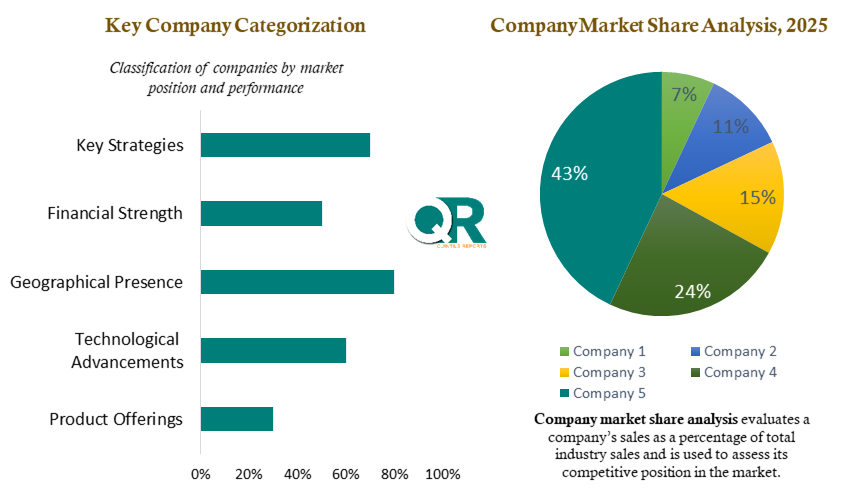

Key market participants include Holcim Ltd., Heidelberg Materials, CEMEX S.A.B. de C.V., Anhui Conch Cement Company, Votorantim Cimentos, UltraTech Cement Ltd., ACC Limited, Taiheiyo Cement Corporation, Calera Corporation, Solidia Technologies, Kiran Global Chem Limited, Ecocem Ireland Ltd., CarbonCure Technologies Inc., JK Cement, Navrattan Group, and other regional and emerging market participants.

Recent industry developments highlight the accelerating transition toward low-carbon cement production and carbon-neutral construction materials. In June 2025, Heidelberg Materials achieved a significant industry milestone by fully selling out the annual production capacity of its evoZero cement, recognized as one of the world's first net-zero cement products. Manufactured at the company's Brevik facility in Norway, evoZero is supported by a large-scale carbon capture and storage (CCS) operation under Norway's Longship project. The facility captures approximately 400,000 tonnes of CO₂ annually, representing nearly half of the plant's emissions, with permanent storage enabled through the Northern Lights infrastructure beneath the North Sea.

In July 2025, China introduced its first Renewable Portfolio Standards (RPS) framework for the cement and steel industries through the National Development and Reform Commission (NDRC). The policy establishes minimum renewable energy consumption requirements for industrial producers and represents a major step toward decarbonizing one of the world's largest cement markets. Provinces with significant renewable energy resources are required to achieve substantially higher renewable energy utilization rates, accelerating investments in cleaner manufacturing technologies and sustainable cement production practices.

These developments reflect broader industry trends focused on decarbonization, renewable energy integration, carbon capture deployment, and next-generation cement technologies. As environmental performance increasingly influences procurement decisions, manufacturers that combine sustainability leadership with operational efficiency and product innovation are expected to strengthen their competitive positioning within the global Green Cement Market.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 7.71 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Type |

|

| The Segment Covered by Raw Material |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report is built upon a rigorous research framework designed to provide accurate, objective, and actionable insights into the evolving Green Cement Market. The study combines extensive primary research with industry stakeholders—including cement manufacturers, construction companies, infrastructure developers, sustainability consultants, technology providers, and regulatory experts—with comprehensive secondary research from government publications, environmental agencies, industry associations, company reports, technical journals, and sustainability databases.

Our analysts evaluate market developments across the entire value chain, from raw material sourcing and supplementary cementitious materials (SCMs) to low-carbon cement production technologies, carbon capture initiatives, and end-use construction applications. Market estimates are validated using multiple data points, including production capacities, infrastructure investments, green building adoption trends, carbon pricing policies, and regional construction activity, ensuring a high degree of accuracy and reliability.

The report also incorporates detailed assessments of evolving regulatory frameworks such as the European Green Deal, Buy Clean initiatives, emissions trading systems, and global net-zero commitments that are reshaping the cement industry. Advanced forecasting models, demand-supply analysis, and data triangulation techniques are utilized to identify future growth opportunities, emerging technology trends, and competitive developments across key markets.

By combining quantitative market intelligence with qualitative industry expertise, this report delivers a balanced and forward-looking perspective that supports strategic planning, investment evaluation, product development, market entry decisions, and long-term business growth. Stakeholders can rely on this study as a trusted source of intelligence for navigating the transition toward sustainable and low-carbon construction materials.

Step 1: Secondary Research and Industry Intelligence Collection

The study begins with extensive secondary research to establish a strong understanding of the Green Cement Market. Information is gathered from cement industry associations, government infrastructure databases, environmental agencies, company annual reports, sustainability reports, technical journals, construction publications, carbon emissions studies, and green building certification organizations such as LEED, BREEAM, and DGNB. Regulatory frameworks including the European Green Deal, Buy Clean initiatives, carbon pricing mechanisms, and net-zero policies are also analyzed.

Step 2: Value Chain and Market Structure Assessment

A detailed evaluation of the green cement value chain is conducted, covering raw material suppliers, supplementary cementitious material (SCM) providers, cement manufacturers, technology providers, distributors, contractors, and end-use construction sectors. This step helps identify key market participants, supply chain dynamics, procurement trends, and revenue-generating segments.

Step 3: Primary Research and Industry Validation

Primary interviews are conducted with cement manufacturers, construction companies, infrastructure developers, sustainability consultants, civil engineers, procurement specialists, government officials, and industry experts. These discussions validate secondary findings and provide real-time insights into technology adoption, market demand, pricing trends, investment priorities, and future growth opportunities.

Step 4: Market Segmentation Analysis

The market is segmented by product type, technology, application, end-use industry, and region. Each segment is evaluated based on historical performance, current demand, regulatory influence, production capacity, and future growth potential. Special attention is given to fly ash-based cement, slag-based cement, LC3 cement, and other low-carbon cement technologies.

Step 5: Market Size Estimation

Market size calculations are performed using a combination of bottom-up and top-down methodologies. Revenue generated by key market participants, production volumes, cement consumption patterns, and regional construction spending are analyzed to determine current market value. Multiple data sources are cross-verified to improve accuracy.

Step 6: Demand-Supply and Pricing Analysis

The study evaluates supply availability of clinker substitutes such as fly ash, GGBFS, calcined clay, and silica fume. Demand trends across residential, commercial, industrial, and infrastructure sectors are assessed alongside pricing dynamics, raw material costs, transportation expenses, and regulatory impacts.

Step 7: Regional Market Assessment

Each region is analyzed based on construction activity, infrastructure investment, environmental regulations, green building adoption, carbon reduction targets, and government sustainability initiatives. Regional demand forecasts are developed using country-specific economic indicators and construction industry trends.

Step 8: Competitive Landscape Evaluation

Leading market participants are analyzed based on product portfolio, sustainability initiatives, production capacity, geographic presence, strategic partnerships, technological innovations, carbon reduction programs, and recent developments. Market positioning and competitive strategies are assessed to understand industry dynamics.

Step 9: Forecast Modeling and Future Trend Analysis

Advanced forecasting models are applied to evaluate future market growth. Key factors considered include urbanization, infrastructure spending, carbon pricing mechanisms, ESG-driven investments, government procurement policies, green building certifications, and advancements in low-carbon cement technologies.

Step 10: Data Triangulation and Quality Validation

All findings undergo rigorous data triangulation and validation using multiple independent sources, expert reviews, company disclosures, industry databases, and market benchmarks. This final step ensures consistency, reliability, and accuracy of market estimates, forecasts, and strategic insights presented in the report.

This report has been prepared by a team of experienced construction materials analysts, sustainability specialists, and infrastructure industry researchers with extensive expertise in low-carbon building materials, environmental regulations, circular economy initiatives, and global construction markets. Through continuous monitoring of market developments, technological innovations, regulatory changes, sustainability frameworks, and investment trends, the research team delivers objective, data-driven insights designed to support informed strategic decision-making across the green cement value chain.

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Green Cement Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Green Cement Market, by Region, (USD Million) 2017-2036

Table 9 Germany Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Green Cement Market, by Region, (USD Million) 2017-2036

Table 21 China Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Green Cement Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Green Cement Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Green Cement Market: Market Scenario

Fig.4 Global Green Cement Market Competitive Outlook

Fig.5 Global Green Cement Market Driver Analysis

Fig.6 Global Green Cement Market Restraint Analysis

Fig.7 Global Green Cement Market Opportunity Analysis

Fig.8 Global Green Cement Market Trends Analysis

Fig.9 Global Green Cement Market: Segment Analysis (Based on the Scope)

Fig.10 Global Green Cement Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Green Cement Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Green Cement Market, by Region, (USD Million) 2017-2036

Table 9 Germany Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Green Cement Market, by Region, (USD Million) 2017-2036

Table 21 China Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Green Cement Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Green Cement Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Green Cement Market: Market Scenario

Fig.4 Global Green Cement Market Competitive Outlook

Fig.5 Global Green Cement Market Driver Analysis

Fig.6 Global Green Cement Market Restraint Analysis

Fig.7 Global Green Cement Market Opportunity Analysis

Fig.8 Global Green Cement Market Trends Analysis

Fig.9 Global Green Cement Market: Segment Analysis (Based on the Scope)

Fig.10 Global Green Cement Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

The global Green Cement Market is projected to reach USD 89.47 billion by 2036, growing from USD 49.52 billion in 2026 at a CAGR of 7.71% during the forecast period. Market growth is driven by increasing demand for sustainable construction materials, stricter carbon emission regulations, and growing investments in green infrastructure.

The Green Cement Market is expected to grow at a CAGR of 7.71% from 2026 to 2036, supported by increasing adoption of low-carbon cement, government sustainability initiatives, and advancements in environmentally friendly cement manufacturing technologies.

The market is primarily driven by growing demand for sustainable construction materials, stringent environmental regulations, increasing green building projects, adoption of supplementary cementitious materials (SCMs), carbon capture technologies, and rising investments in infrastructure development worldwide.

Green cement is a sustainable alternative to conventional Portland cement that incorporates materials such as fly ash, slag, calcined clay, and other industrial by-products to reduce clinker content and carbon emissions. It offers comparable strength and durability while significantly lowering the environmental impact of construction.

North America currently leads the Green Cement Market due to strong environmental regulations, green building initiatives, and government procurement programs promoting low-carbon construction materials. Meanwhile, Asia-Pacific is expected to register the fastest growth owing to rapid urbanization and infrastructure expansion.

Major companies operating in the Green Cement Market include Holcim Ltd., Heidelberg Materials, CEMEX S.A.B. de C.V., Anhui Conch Cement Company, Votorantim Cimentos, UltraTech Cement Ltd., ACC Limited, Taiheiyo Cement Corporation, CarbonCure Technologies Inc., Ecocem Ireland Ltd., and JK Cement.

Green cement helps reduce greenhouse gas emissions, lowers energy consumption during production, utilizes recycled industrial materials, and supports green building certifications such as LEED and BREEAM. It plays a key role in achieving carbon reduction goals and promoting environmentally responsible infrastructure development.

Future growth opportunities include the adoption of LC3 (Limestone Calcined Clay Cement), carbon capture, utilization and storage (CCUS), clinker-free cement technologies, AI-enabled manufacturing, circular economy practices, and increasing investments in sustainable infrastructure and net-zero construction projects.

The global Green Cement Market was valued at USD 49.52 billion in 2026 and is projected to reach USD 89.47 billion by 2036, growing at a CAGR of 7.71% during the forecast period. Green cement has evolved from a niche sustainable building material into a mainstream construction solution as governments, developers, and infrastructure operators increasingly prioritize carbon reduction and environmentally responsible construction practices. Unlike conventional Portland cement, green cement incorporates supplementary cementitious materials (SCMs) such as fly ash, ground granulated blast furnace slag (GGBFS), limestone, calcined clay, silica fume, and other industrial by-products to significantly reduce clinker content and lower carbon emissions.

The global cement industry is responsible for nearly 8% of worldwide carbon dioxide emissions, making decarbonization a critical priority for policymakers and industry stakeholders. Green cement offers a practical pathway toward reducing the environmental footprint of construction activities while maintaining structural performance, durability, and cost competitiveness. The market is benefiting from growing regulatory support, increasing adoption of green building certifications, carbon pricing mechanisms, and rising ESG-focused investments across residential, commercial, and infrastructure sectors.

The future outlook of the industry is increasingly influenced by three powerful forces: stricter environmental regulations, technological innovation in low-carbon cement production, and growing investor preference for sustainable construction materials. Programs such as the U.S. Buy Clean Initiative, the European Green Deal, and climate commitments under the Paris Agreement are transforming sustainability objectives into mandatory procurement requirements. Simultaneously, advancements in carbon capture utilization and storage (CCUS), clinker-free formulations, LC3 technologies, and AI-enabled manufacturing processes are reshaping the competitive landscape and accelerating the transition toward low-carbon construction materials.

Accelerated Adoption of Limestone Calcined Clay Cement (LC3)

LC3 technology is emerging as one of the most promising low-carbon cement solutions globally, capable of reducing carbon emissions by up to 40% compared to conventional Portland cement. Growing government support for sustainable infrastructure and public-sector green procurement programs is accelerating commercial deployment across developed and emerging economies. Growing investments in renewable energy infrastructure and sustainable construction materials are also supporting demand across the Solar Energy Storage Battery Market.

Carbon Capture, Utilization, and Storage (CCUS) Integration

Leading cement manufacturers are increasingly investing in CCUS technologies to significantly reduce process emissions. Major projects across Europe, North America, and Asia are demonstrating the commercial viability of carbon capture systems integrated directly into cement production facilities, helping producers move toward net-zero manufacturing targets.

ESG-Driven Financing Accelerating Market Adoption

Green bonds, sustainability-linked loans, and ESG-focused investment mandates are increasingly requiring developers and contractors to utilize low-carbon building materials. As a result, green cement is becoming an essential component of environmentally certified construction projects worldwide.

Expansion of Clinker-Free Cement Technologies

Clinker-free and ultra-low clinker formulations are gaining traction as manufacturers seek to eliminate the most carbon-intensive component of traditional cement production. Regulatory approvals and certification milestones are enabling broader adoption across infrastructure, commercial, and residential construction sectors.

Digitalization and AI-Enabled Manufacturing Optimization

Artificial intelligence, predictive analytics, and digital quality control systems are being deployed to optimize raw material blending, improve energy efficiency, reduce waste generation, and ensure consistent product performance across green cement manufacturing operations.

The Green Cement Market value chain begins with the sourcing of raw materials and supplementary cementitious materials (SCMs), which form the foundation of low-carbon cement production. Key inputs include fly ash from coal-fired power plants, ground granulated blast furnace slag (GGBFS) from steel manufacturing facilities, limestone, calcined clay, silica fume, recycled aggregates, and other industrial by-products. The availability, quality, and geographic proximity of these materials significantly influence production costs, supply chain efficiency, and the carbon footprint of final cement products. As traditional coal generation declines globally, producers are increasingly diversifying feedstock sources through alternative SCMs such as LC3 materials, reclaimed ash reserves, and innovative mineral additives.

The second stage involves cement manufacturing and processing, where producers integrate alternative materials into optimized cement formulations. Leading manufacturers are investing heavily in energy-efficient kilns, alternative fuels, carbon capture utilization and storage (CCUS) systems, digital process controls, and AI-driven quality management platforms to reduce emissions while maintaining product performance. This stage represents the largest opportunity for decarbonization, as conventional clinker production remains the most carbon-intensive component of the cement value chain. Companies capable of reducing clinker factors while maintaining strength, durability, and regulatory compliance are gaining a significant competitive advantage.

Distribution and logistics form the third stage of the value chain, encompassing bulk cement transportation, ready-mix concrete integration, regional distribution networks, and project-specific supply management. Because cement is a high-volume, low-margin product, transportation costs play a critical role in determining competitiveness. Producers increasingly establish manufacturing facilities close to urban centers, industrial hubs, and major infrastructure corridors to reduce logistics expenses and minimize transportation-related emissions. Strategic partnerships with construction firms, ready-mix suppliers, and infrastructure developers further strengthen market penetration and supply chain resilience.

The final stage consists of end-use applications across residential, commercial, industrial, and infrastructure construction sectors. Residential construction currently represents the largest demand segment, supported by green building certifications, sustainable housing initiatives, and ESG-focused development programs. Commercial buildings, transportation infrastructure, renewable energy projects, and public works increasingly specify low-carbon cement products to comply with environmental regulations and sustainability targets. Growing adoption of LEED, BREEAM, DGNB, and other green building frameworks is transforming procurement requirements and creating long-term demand for certified low-carbon construction materials.

Across the entire value chain, technology providers, carbon management companies, certification bodies, environmental consultants, and regulatory agencies play increasingly important supporting roles. Their contributions help manufacturers achieve compliance, improve environmental performance, secure sustainability certifications, and develop next-generation green cement solutions. As carbon pricing mechanisms, ESG financing, and climate regulations continue to expand globally, value creation within the green cement ecosystem is expected to shift toward innovation, emissions reduction capabilities, and lifecycle sustainability performance.

The growing focus on sustainable material science is also influencing adjacent cement applications beyond traditional construction. Advances in formulation technologies, durability enhancement, and specialty cement development are supporting innovation across sectors, including healthcare materials. Similar trends can be observed in the Dental Cement Market, where manufacturers are developing advanced bonding materials with improved performance, longevity, and environmental characteristics.

North America represents one of the most mature markets for green cement, supported by stringent environmental regulations, aggressive carbon reduction targets, and growing adoption of sustainable construction practices. The United States and Canada continue to promote low-carbon building materials through initiatives such as the U.S. EPA emission standards, the Buy Clean program, and Canada's Output-Based Pricing System. These policies are encouraging cement manufacturers to invest in carbon capture, utilization, and storage (CCUS) technologies, alternative fuels, and clinker reduction strategies. Non-residential construction remains a major demand center, driven by increasing adoption of LEED-certified buildings and public infrastructure projects that prioritize environmentally responsible materials. The United States dominates regional demand due to strong government support, a robust green building pipeline, and increasing ESG-driven procurement requirements.

Europe continues to lead global innovation in green cement production, driven by ambitious climate policies and strict emissions regulations. Frameworks such as the European Green Deal and the EU Emissions Trading System are accelerating the transition away from traditional clinker-intensive cement production toward low-carbon alternatives. Cement manufacturers across Germany, France, the United Kingdom, and Nordic countries are increasingly incorporating fly ash, slag, calcined clay, and recycled materials into production processes while simultaneously investing in CCUS technologies. The region's strong commitment to circular economy principles is encouraging greater utilization of industrial by-products and waste-derived materials. Demand remains particularly strong in infrastructure and commercial construction projects seeking compliance with BREEAM, DGNB, and other sustainability certification standards.

Asia Pacific accounts for the largest share of global green cement demand and is expected to remain the fastest-growing regional market throughout the forecast period. Rapid urbanization, large-scale infrastructure development, and increasing government support for sustainable construction are driving widespread adoption across China, India, Japan, South Korea, and Southeast Asia. The region benefits from abundant availability of supplementary cementitious materials such as fly ash and blast furnace slag, which help reduce production costs while lowering emissions. National carbon reduction targets, green infrastructure investments, and growing environmental awareness among developers are accelerating market expansion. Government-backed construction projects increasingly require low-carbon materials, creating substantial opportunities for green cement producers. Rapid infrastructure expansion and renewable energy deployment continue to create opportunities across the Distributed Solar Power Generation Market.

The Latin American green cement market is steadily expanding as governments strengthen environmental regulations and prioritize sustainable infrastructure development. Countries such as Brazil and Mexico are investing in transportation networks, affordable housing projects, and public infrastructure programs that increasingly incorporate environmentally friendly construction materials. Local cement manufacturers are gradually increasing the use of fly ash, slag, and alternative binders to reduce carbon emissions and improve sustainability performance. Although challenges related to limited technological infrastructure, inconsistent raw material availability, and fragmented regulatory frameworks remain, the long-term outlook remains positive as climate-focused investments continue to increase across the region.

The Middle East & Africa region is emerging as a promising market for green cement as governments pursue economic diversification strategies and sustainable urban development initiatives. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are promoting environmentally responsible construction through green building standards, energy-efficiency regulations, and carbon reduction programs. Large-scale smart city developments, transportation infrastructure projects, and commercial construction activities are creating demand for low-carbon cement products. While adoption is currently constrained by limited access to advanced manufacturing technologies and inconsistent availability of industrial by-products, increasing awareness of sustainable construction practices is expected to support gradual market expansion over the coming years.

The United States remains the largest market for green cement in North America, supported by strong regulatory backing, infrastructure modernization programs, and increasing adoption of sustainable building practices. Federal initiatives promoting low-carbon materials, combined with stricter emissions regulations, are encouraging construction companies and developers to incorporate green cement into both public and private sector projects. Leading manufacturers continue to invest in innovative technologies including carbon capture and storage, alternative fuel utilization, and advanced clinker substitution methods. The growing popularity of LEED-certified buildings and ESG-focused construction projects is further accelerating adoption, positioning green cement as a critical component of the nation's decarbonization strategy.

Germany continues to serve as a benchmark market for sustainable cement production and green construction practices. Government policies aligned with the Renewable Energy Sources Act and the EU's Fit for 55 program are driving significant investments in low-carbon building materials and industrial decarbonization technologies. Major producers are expanding the use of calcined clay, industrial by-products, and alternative clinker materials while simultaneously deploying CCUS technologies and energy-efficient kiln systems. Strong collaboration between government agencies, research institutions, and industry stakeholders has accelerated innovation, helping Germany maintain its leadership position in Europe's green cement transition.

Japan's green cement market is being shaped by ambitious carbon neutrality goals, advanced manufacturing capabilities, and a strong commitment to resource efficiency. Cement producers are increasingly utilizing municipal incinerator ash, recycled aggregates, construction waste, and industrial by-products to develop environmentally sustainable cement formulations. Investments in energy-efficient kiln technologies, waste valorization systems, and smart manufacturing solutions are improving production efficiency while reducing emissions. As Japan continues to strengthen its circular economy initiatives and sustainable construction policies, green cement is expected to play an increasingly important role in reducing the environmental footprint of the country's building and infrastructure sectors.

The Green Cement Market is expected to remain one of the fastest-growing segments within the sustainable construction materials industry as governments, developers, and investors prioritize carbon reduction initiatives. Adoption of LC3 technologies, carbon capture solutions, and alternative clinker formulations is expected to accelerate market transformation through 2036.

The Green Cement Market is undergoing a significant transformation as sustainability, carbon reduction performance, and regulatory compliance become primary competitive differentiators. Market participants are increasingly competing through the development of low-carbon cement formulations, alternative clinker technologies, carbon capture solutions, and circular economy initiatives rather than solely on pricing or production capacity. As governments tighten emissions regulations and construction companies adopt stricter ESG targets, manufacturers are investing heavily in technologies that reduce embodied carbon while maintaining structural performance and durability.

Leading producers are focusing on the increased utilization of supplementary cementitious materials (SCMs) such as fly ash, ground granulated blast furnace slag (GGBFS), calcined clay, silica fume, and recycled construction materials to lower clinker content and reduce lifecycle emissions. The ability to provide certified low-carbon products supported by Environmental Product Declarations (EPDs), LEED compliance, BREEAM certification compatibility, and other sustainability credentials has become a critical factor influencing purchasing decisions across residential, commercial, and infrastructure projects.

Technological innovation continues to reshape the competitive landscape. Major cement manufacturers are investing in carbon capture, utilization, and storage (CCUS) technologies, alternative fuel systems, AI-enabled process optimization, and next-generation clinker-free cement formulations. Companies that successfully integrate carbon reduction technologies while maintaining cost competitiveness and product performance are strengthening their market positions. Furthermore, strategic partnerships with governments, infrastructure developers, and green finance institutions are enabling manufacturers to capitalize on increasing demand for sustainable construction materials.

The market also benefits from growing adoption of circular economy practices, including the reuse of industrial by-products, construction waste recycling, and resource-efficient production processes. Manufacturers capable of securing reliable SCM supply chains, optimizing energy consumption, and scaling low-carbon production technologies are expected to gain long-term competitive advantages as environmental regulations continue to tighten globally.

Key market participants include Holcim Ltd., Heidelberg Materials, CEMEX S.A.B. de C.V., Anhui Conch Cement Company, Votorantim Cimentos, UltraTech Cement Ltd., ACC Limited, Taiheiyo Cement Corporation, Calera Corporation, Solidia Technologies, Kiran Global Chem Limited, Ecocem Ireland Ltd., CarbonCure Technologies Inc., JK Cement, Navrattan Group, and other regional and emerging market participants.

Recent industry developments highlight the accelerating transition toward low-carbon cement production and carbon-neutral construction materials. In June 2025, Heidelberg Materials achieved a significant industry milestone by fully selling out the annual production capacity of its evoZero cement, recognized as one of the world's first net-zero cement products. Manufactured at the company's Brevik facility in Norway, evoZero is supported by a large-scale carbon capture and storage (CCS) operation under Norway's Longship project. The facility captures approximately 400,000 tonnes of CO₂ annually, representing nearly half of the plant's emissions, with permanent storage enabled through the Northern Lights infrastructure beneath the North Sea.

In July 2025, China introduced its first Renewable Portfolio Standards (RPS) framework for the cement and steel industries through the National Development and Reform Commission (NDRC). The policy establishes minimum renewable energy consumption requirements for industrial producers and represents a major step toward decarbonizing one of the world's largest cement markets. Provinces with significant renewable energy resources are required to achieve substantially higher renewable energy utilization rates, accelerating investments in cleaner manufacturing technologies and sustainable cement production practices.

These developments reflect broader industry trends focused on decarbonization, renewable energy integration, carbon capture deployment, and next-generation cement technologies. As environmental performance increasingly influences procurement decisions, manufacturers that combine sustainability leadership with operational efficiency and product innovation are expected to strengthen their competitive positioning within the global Green Cement Market.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 7.71 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Type |

|

| The Segment Covered by Raw Material |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report is built upon a rigorous research framework designed to provide accurate, objective, and actionable insights into the evolving Green Cement Market. The study combines extensive primary research with industry stakeholders—including cement manufacturers, construction companies, infrastructure developers, sustainability consultants, technology providers, and regulatory experts—with comprehensive secondary research from government publications, environmental agencies, industry associations, company reports, technical journals, and sustainability databases.

Our analysts evaluate market developments across the entire value chain, from raw material sourcing and supplementary cementitious materials (SCMs) to low-carbon cement production technologies, carbon capture initiatives, and end-use construction applications. Market estimates are validated using multiple data points, including production capacities, infrastructure investments, green building adoption trends, carbon pricing policies, and regional construction activity, ensuring a high degree of accuracy and reliability.

The report also incorporates detailed assessments of evolving regulatory frameworks such as the European Green Deal, Buy Clean initiatives, emissions trading systems, and global net-zero commitments that are reshaping the cement industry. Advanced forecasting models, demand-supply analysis, and data triangulation techniques are utilized to identify future growth opportunities, emerging technology trends, and competitive developments across key markets.

By combining quantitative market intelligence with qualitative industry expertise, this report delivers a balanced and forward-looking perspective that supports strategic planning, investment evaluation, product development, market entry decisions, and long-term business growth. Stakeholders can rely on this study as a trusted source of intelligence for navigating the transition toward sustainable and low-carbon construction materials.

Step 1: Secondary Research and Industry Intelligence Collection

The study begins with extensive secondary research to establish a strong understanding of the Green Cement Market. Information is gathered from cement industry associations, government infrastructure databases, environmental agencies, company annual reports, sustainability reports, technical journals, construction publications, carbon emissions studies, and green building certification organizations such as LEED, BREEAM, and DGNB. Regulatory frameworks including the European Green Deal, Buy Clean initiatives, carbon pricing mechanisms, and net-zero policies are also analyzed.

Step 2: Value Chain and Market Structure Assessment

A detailed evaluation of the green cement value chain is conducted, covering raw material suppliers, supplementary cementitious material (SCM) providers, cement manufacturers, technology providers, distributors, contractors, and end-use construction sectors. This step helps identify key market participants, supply chain dynamics, procurement trends, and revenue-generating segments.

Step 3: Primary Research and Industry Validation

Primary interviews are conducted with cement manufacturers, construction companies, infrastructure developers, sustainability consultants, civil engineers, procurement specialists, government officials, and industry experts. These discussions validate secondary findings and provide real-time insights into technology adoption, market demand, pricing trends, investment priorities, and future growth opportunities.

Step 4: Market Segmentation Analysis

The market is segmented by product type, technology, application, end-use industry, and region. Each segment is evaluated based on historical performance, current demand, regulatory influence, production capacity, and future growth potential. Special attention is given to fly ash-based cement, slag-based cement, LC3 cement, and other low-carbon cement technologies.

Step 5: Market Size Estimation

Market size calculations are performed using a combination of bottom-up and top-down methodologies. Revenue generated by key market participants, production volumes, cement consumption patterns, and regional construction spending are analyzed to determine current market value. Multiple data sources are cross-verified to improve accuracy.

Step 6: Demand-Supply and Pricing Analysis

The study evaluates supply availability of clinker substitutes such as fly ash, GGBFS, calcined clay, and silica fume. Demand trends across residential, commercial, industrial, and infrastructure sectors are assessed alongside pricing dynamics, raw material costs, transportation expenses, and regulatory impacts.

Step 7: Regional Market Assessment

Each region is analyzed based on construction activity, infrastructure investment, environmental regulations, green building adoption, carbon reduction targets, and government sustainability initiatives. Regional demand forecasts are developed using country-specific economic indicators and construction industry trends.

Step 8: Competitive Landscape Evaluation

Leading market participants are analyzed based on product portfolio, sustainability initiatives, production capacity, geographic presence, strategic partnerships, technological innovations, carbon reduction programs, and recent developments. Market positioning and competitive strategies are assessed to understand industry dynamics.

Step 9: Forecast Modeling and Future Trend Analysis

Advanced forecasting models are applied to evaluate future market growth. Key factors considered include urbanization, infrastructure spending, carbon pricing mechanisms, ESG-driven investments, government procurement policies, green building certifications, and advancements in low-carbon cement technologies.

Step 10: Data Triangulation and Quality Validation

All findings undergo rigorous data triangulation and validation using multiple independent sources, expert reviews, company disclosures, industry databases, and market benchmarks. This final step ensures consistency, reliability, and accuracy of market estimates, forecasts, and strategic insights presented in the report.

This report has been prepared by a team of experienced construction materials analysts, sustainability specialists, and infrastructure industry researchers with extensive expertise in low-carbon building materials, environmental regulations, circular economy initiatives, and global construction markets. Through continuous monitoring of market developments, technological innovations, regulatory changes, sustainability frameworks, and investment trends, the research team delivers objective, data-driven insights designed to support informed strategic decision-making across the green cement value chain.

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Green Cement Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Green Cement Market, by Region, (USD Million) 2017-2036

Table 9 Germany Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Green Cement Market, by Region, (USD Million) 2017-2036

Table 21 China Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Green Cement Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Green Cement Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Green Cement Market: Market Scenario

Fig.4 Global Green Cement Market Competitive Outlook

Fig.5 Global Green Cement Market Driver Analysis

Fig.6 Global Green Cement Market Restraint Analysis

Fig.7 Global Green Cement Market Opportunity Analysis

Fig.8 Global Green Cement Market Trends Analysis

Fig.9 Global Green Cement Market: Segment Analysis (Based on the Scope)

Fig.10 Global Green Cement Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Green Cement Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Green Cement Market, by Region, (USD Million) 2017-2036

Table 9 Germany Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Green Cement Market, by Region, (USD Million) 2017-2036

Table 21 China Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Green Cement Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Green Cement Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Green Cement Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Green Cement Market: Market Scenario

Fig.4 Global Green Cement Market Competitive Outlook

Fig.5 Global Green Cement Market Driver Analysis

Fig.6 Global Green Cement Market Restraint Analysis

Fig.7 Global Green Cement Market Opportunity Analysis

Fig.8 Global Green Cement Market Trends Analysis

Fig.9 Global Green Cement Market: Segment Analysis (Based on the Scope)

Fig.10 Global Green Cement Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America