The global Copper Market was valued at USD 265.50 billion in 2026 and is projected to reach USD 634.47 billion by 2036, registering a robust CAGR of 8.81% during the forecast period. Copper remains one of the world's most strategically important industrial metals due to its superior electrical conductivity, thermal efficiency, corrosion resistance, and recyclability. The metal plays a fundamental role across construction, power generation, electrical infrastructure, transportation, electronics, telecommunications, and industrial manufacturing sectors.

The market is entering a period of accelerated growth as global economies pursue electrification, renewable energy adoption, and carbon reduction initiatives. Increasing investments in electric vehicles, power transmission networks, smart grids, and clean energy infrastructure are significantly expanding copper demand. Simultaneously, rapid urbanization, industrialization, and technological innovation continue to strengthen consumption across both developed and emerging economies.

Copper has emerged as a critical enabler of the global energy transition due to its extensive use in renewable power systems, electric mobility solutions, and advanced electrical infrastructure. Electric vehicles require substantially more copper than conventional internal combustion engine vehicles, while solar farms, wind turbines, battery storage systems, and grid modernization projects rely heavily on copper-intensive components.

The growing digital economy is also supporting demand growth. Data centers, telecommunications infrastructure, semiconductors, consumer electronics, and industrial automation systems increasingly depend on copper for efficient energy transfer and connectivity. As governments continue to invest in sustainable infrastructure and industrial electrification programs, copper demand is expected to rise steadily throughout the forecast period.

Asia-Pacific remains the dominant force in the global copper market, accounting for the largest share of both production and consumption. China continues to lead global demand due to extensive infrastructure projects, renewable energy investments, electric vehicle manufacturing, and electronics production. India is also emerging as a significant growth market, supported by industrial expansion, urbanization, and power sector modernization initiatives.

North America is witnessing increasing copper demand due to government-backed infrastructure programs, grid modernization projects, and clean energy investments. The United States is actively strengthening domestic supply chains to support EV manufacturing, renewable energy deployment, and advanced industrial applications. Canada contributes significantly through mining activities and refining capacity expansion.

Europe continues to experience strong demand driven by renewable energy targets, industrial electrification, and electric mobility adoption. Germany, France, and the United Kingdom remain key consumers due to their investments in sustainable infrastructure and clean energy systems. The region's emphasis on recycling and circular economy practices further supports market stability.

Latin America remains a cornerstone of global copper production, with Chile and Peru serving as major exporters and mining investment destinations. Meanwhile, the Middle East and Africa are gradually increasing copper consumption through infrastructure development, renewable energy projects, and industrial diversification initiatives.

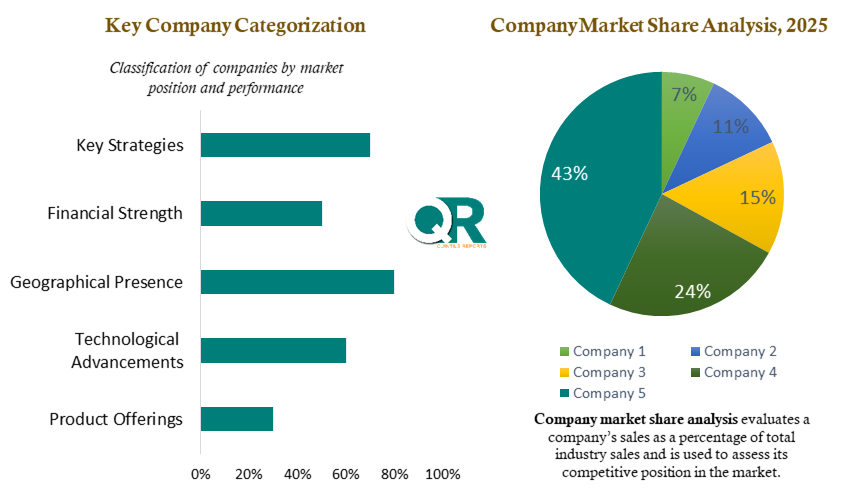

The copper market is highly competitive, characterized by the presence of global mining companies, integrated metal producers, refiners, and recycling specialists. Competitive differentiation increasingly depends on production efficiency, resource availability, sustainability initiatives, and downstream integration capabilities.

Major market participants are investing in mine expansions, new exploration projects, refining capacity upgrades, and recycling technologies to secure long-term supply. Companies are also adopting digital mining solutions, automation technologies, and carbon reduction strategies to improve operational efficiency and environmental performance.

Sustainability has become a critical competitive factor as customers increasingly prioritize responsibly sourced materials and low-carbon supply chains. Organizations with strong ESG performance, recycling capabilities, and transparent sourcing practices are expected to strengthen their market positions as demand for sustainable materials continues to grow.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 8.81 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Copper Type |

|

| The Segment Covered by Product Type |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report is developed using a comprehensive research framework that integrates extensive primary interviews, industry consultations, and detailed secondary research from reputable sources. The analysis combines quantitative market modeling with qualitative industry expertise to deliver reliable and actionable intelligence.

All market estimates undergo rigorous validation processes, including data triangulation, trend analysis, supply-demand assessments, and expert review. This methodology ensures a high degree of accuracy, consistency, and transparency, enabling stakeholders to make informed strategic decisions.

The study employs a structured combination of primary and secondary research methodologies. Secondary research includes the analysis of mining industry reports, government publications, commodity databases, corporate disclosures, trade statistics, and industry journals. Primary research involves interviews with mining executives, metal traders, refiners, manufacturers, industry experts, and procurement specialists.

Advanced forecasting models, demand-supply analysis, regional consumption assessments, and macroeconomic evaluations are applied to generate market projections. Data validation through triangulation and expert verification further strengthens the reliability of the report's findings.

This report has been prepared by a team of experienced metals and mining analysts, commodity market specialists, and industry researchers with extensive expertise in global resource markets. The research team combines technical knowledge, market intelligence, and advanced analytical methodologies to provide accurate, objective, and actionable insights.

Through continuous monitoring of commodity trends, mining investments, regulatory developments, sustainability initiatives, and technological advancements, our analysts deliver strategic intelligence that helps stakeholders navigate evolving market conditions and capitalize on emerging opportunities. The report reflects a commitment to research excellence, transparency, and industry relevance, making it a trusted resource for investors, producers, manufacturers, policymakers, and industry participants worldwide.

1. Executive Summary

1.1 Market Overview

1.2 Market Definition and Scope

1.3 Key Findings and Strategic Insights

1.4 Market Size Analysis (20262036)

1.5 Growth Outlook and Revenue Opportunity

1.6 Key Demand Drivers

1.7 Market Challenges and Risks

1.8 Emerging Opportunities

1.9 Regional Market Snapshot

1.10 Competitive Landscape Overview

2. Introduction to the Global Copper Market

2.1 Overview of Copper Industry

2.2 Importance of Copper in the Global Economy

2.3 Physical and Chemical Properties of Copper

2.4 Copper Value Chain Analysis

2.5 Historical Market Evolution

2.6 Current Industry Structure

2.7 Stakeholder Ecosystem Analysis

3. Market Size and Forecast Analysis

3.1 Global Market Revenue Analysis (20262036)

3.2 Historical Market Performance (20172024)

3.3 Base Year Assessment (2025)

3.4 Forecast Methodology

3.5 CAGR Analysis (20262036)

3.6 Incremental Revenue Opportunity Analysis

3.7 Demand-Supply Forecast Assessment

3.8 Scenario Analysis (Optimistic, Base, Conservative)

4. Industry Dynamics

4.1 Market Drivers

4.1.1 Renewable Energy Infrastructure Expansion

4.1.2 Rising Electric Vehicle Adoption

4.1.3 Grid Modernization Initiatives

4.1.4 Construction and Urbanization Growth

4.1.5 Industrial Automation Expansion

4.1.6 Telecommunications Infrastructure Development

4.2 Market Restraints

4.2.1 Copper Price Volatility

4.2.2 Environmental Regulations and Compliance Costs

4.2.3 Declining Ore Grades

4.2.4 Rising Mining and Processing Costs

4.2.5 Geopolitical Risks and Trade Disruptions

4.3 Market Opportunities

4.3.1 Energy Transition Investments

4.3.2 Growth in Copper Recycling

4.3.3 EV Charging Infrastructure Development

4.3.4 Smart Cities Expansion

4.3.5 Data Center Growth

4.3.6 Digital Infrastructure Investments

5. Market Trends and Emerging Technologies

5.1 Electrification Megatrend

5.2 Renewable Energy Adoption Trends

5.3 Copper Recycling and Circular Economy

5.4 Sustainable Mining Technologies

5.5 Digital Mining Solutions and Automation

5.6 AI and Data-Driven Mining Operations

5.7 ESG and Responsible Sourcing Trends

5.8 Low-Carbon Copper Production Initiatives

6. Copper Demand Analysis by Application

6.1 Electrical and Electronics Industry

6.2 Power Generation and Transmission

6.3 Renewable Energy Systems

6.4 Electric Vehicles and Automotive Industry

6.5 Building and Construction Sector

6.6 Telecommunications Infrastructure

6.7 Data Centers and Cloud Infrastructure

6.8 Industrial Machinery and Equipment

6.9 Consumer Goods and Appliances

6.10 Emerging Applications

7. Supply Chain and Value Chain Analysis

7.1 Copper Mining Industry Structure

7.2 Ore Extraction Process

7.3 Smelting and Refining Operations

7.4 Distribution Network Analysis

7.5 End-User Consumption Analysis

7.6 Supply Chain Risk Assessment

7.7 Logistics and Transportation Challenges

7.8 Raw Material Availability Analysis

8. Market Segmentation by Copper Type

8.1 Primary Copper

8.1.1 Market Size and Forecast

8.1.2 Production Analysis

8.1.3 Key Applications

8.1.4 Regional Demand Trends

8.2 Secondary Copper

8.2.1 Market Size and Forecast

8.2.2 Recycling Industry Assessment

8.2.3 Sustainability Benefits

8.2.4 Growth Prospects

9. Market Segmentation by Product Type

9.1 Cathodes & Blister Copper

9.1.1 Market Overview

9.1.2 Production Trends

9.1.3 Demand Analysis

9.2 Refined Copper

9.2.1 Market Size and Forecast

9.2.2 Industrial Applications

9.2.3 Growth Drivers

9.3 Copper Scrap

9.3.1 Recycling Market Analysis

9.3.2 Supply Dynamics

9.3.3 Circular Economy Impact

10. Market Segmentation by Copper Product Form

10.1 Wire

10.2 Rods

10.3 Bars & Sections

10.4 Flat Rolled Products

10.5 Tubes

10.6 Foils

For Each Segment:

Market Size & Forecast

Demand Analysis

Key Applications

Regional Outlook

Growth Opportunities

11. Market Segmentation by Form

11.1 Rods & Bars

11.2 Plates & Sheets

11.3 Wires & Cables

11.4 Tubes & Pipes

11.5 Foils & Strips

11.6 Powders

Each Segment Includes:

Revenue Analysis

Volume Analysis

Industry Applications

Regional Demand Trends

12. Market Segmentation by End-Use Industry

12.1 Electrical & Electronics

Cables

Wiring Systems

Transformers

12.2 Industrial Equipment

12.3 Transport

12.4 Infrastructure

12.5 Building & Construction

12.6 Renewable Energy

Solar Power Systems

Wind Energy Installations

Energy Storage Systems

12.7 Automotive

Electric Vehicles

Motors

Charging Infrastructure

12.8 Power Generation & Transmission

12.9 Telecommunications & Data Centers

12.10 Consumer Goods & Appliances

12.11 Others

13. Regional Market Analysis

13.1 North America

13.1.1 Market Overview

13.1.2 United States Analysis

13.1.3 Canada Analysis

13.1.4 Key Investments

13.1.5 Growth Opportunities

13.2 Europe

13.2.1 Market Overview

13.2.2 Germany

13.2.3 United Kingdom

13.2.4 France

13.2.5 Italy

13.2.6 Spain

13.2.7 Rest of Europe

13.3 Asia-Pacific

13.3.1 Market Overview

13.3.2 China

13.3.3 India

13.3.4 Japan

13.3.5 South Korea

13.3.6 Australia

13.3.7 Southeast Asia

13.4 Latin America

13.4.1 Brazil

13.4.2 Mexico

13.4.3 Argentina

13.4.4 Chile

13.4.5 Peru

13.5 Middle East & Africa

13.5.1 Saudi Arabia

13.5.2 UAE

13.5.3 South Africa

13.5.4 Rest of MEA

14. Country-Level Market Analysis

14.1 Top Copper Consuming Countries

14.2 Top Copper Producing Countries

14.3 Import-Export Analysis

14.4 Regulatory Landscape by Country

14.5 Investment Trends by Country

15. Competitive Landscape

15.1 Market Structure Analysis

15.2 Competitive Benchmarking

15.3 Market Share Analysis

15.4 Strategic Developments

15.5 Mergers & Acquisitions

15.6 Capacity Expansion Projects

15.7 New Exploration Projects

15.8 Sustainability Initiatives

16. Company Profiles

Profile Structure for Each Company:

Company Overview

Business Description

Product Portfolio

Financial Performance

Geographic Presence

Production Capacity

Strategic Initiatives

SWOT Analysis

Key Companies

Codelco

Freeport-McMoRan

BHP Group

Glencore plc

Southern Copper Corporation

Anglo American plc

Antofagasta plc

First Quantum Minerals Ltd.

Jiangxi Copper Corporation

Hindustan Copper Limited

Additional market participants

17. Sustainability and ESG Analysis

17.1 Environmental Impact Assessment

17.2 Carbon Emission Reduction Strategies

17.3 Responsible Mining Practices

17.4 Water Resource Management

17.5 Recycling and Circular Economy

17.6 ESG Benchmarking

18. Regulatory Framework

18.1 Mining Regulations

18.2 Environmental Policies

18.3 Trade Policies and Tariffs

18.4 Sustainability Standards

18.5 International Compliance Requirements

19. Strategic Recommendations

19.1 Investment Opportunities

19.2 Market Entry Strategies

19.3 Growth Strategies for Producers

19.4 Supply Security Recommendations

19.5 Sustainability Roadmap

19.6 Risk Mitigation Strategies

20. Research Methodology

20.1 Research Framework

20.2 Primary Research Methodology

20.3 Secondary Research Sources

20.4 Data Collection Process

20.5 Forecasting Models

20.6 Data Validation and Triangulation

20.7 Assumptions and Limitations

21. Appendix

21.1 Abbreviations and Acronyms

21.2 Glossary of Terms

21.3 List of Tables

21.4 List of Figures

21.5 References

21.6 About the Research Team

21.7 Customization Options

List of Tables

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 21 China Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global India Outdoor Air Pollution Control Market: market scenario

Fig.4 Global India Outdoor Air Pollution Control Market competitive outlook

Fig.5 Global India Outdoor Air Pollution Control Market driver analysis

Fig.6 Global India Outdoor Air Pollution Control Market restraint analysis

Fig.7 Global India Outdoor Air Pollution Control Market opportunity analysis

Fig.8 Global India Outdoor Air Pollution Control Market trends analysis

Fig.9 Global India Outdoor Air Pollution Control Market: Segment Analysis (Based on the scope)

Fig.10 Global India Outdoor Air Pollution Control Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

The global Copper Market is projected to grow from USD 265.50 billion in 2026 to approximately USD 634.47 billion by 2036, driven by increasing demand from electric vehicles, renewable energy projects, power infrastructure, and industrial applications.

The Copper Market is expected to register a compound annual growth rate (CAGR) of 8.81% during the forecast period from 2026 to 2036.

Key factors driving market growth include the rapid adoption of electric vehicles, expansion of renewable energy infrastructure, modernization of power grids, increasing urbanization, growth in construction activities, and rising demand from data centers, telecommunications, and industrial manufacturing sectors.

Copper is essential for electric vehicles and renewable energy systems due to its superior electrical conductivity and durability. EVs require significantly more copper than conventional vehicles for motors, batteries, charging systems, and wiring. Similarly, solar panels, wind turbines, battery storage systems, and transmission networks rely heavily on copper for efficient energy generation and distribution.

Asia-Pacific dominates the global Copper Market, led by China’s extensive infrastructure development, renewable energy investments, electric vehicle production, and electronics manufacturing. India is also emerging as a major growth market due to rapid industrialization and urban expansion.

Major companies operating in the Copper Market include Codelco, Freeport-McMoRan, BHP Group, Glencore plc, Southern Copper Corporation, Anglo American plc, Antofagasta plc, First Quantum Minerals Ltd., Jiangxi Copper Corporation, KGHM Polska Miedź S.A., Hindustan Copper Limited, and Aurubis AG.

Copper recycling is playing an increasingly important role in market growth by supporting sustainability goals, reducing environmental impact, and helping meet rising demand. Recycled copper retains nearly all of its original properties, making it a cost-effective and environmentally responsible alternative to primary copper production.

Significant opportunities exist in smart grid deployment, renewable energy integration, electric vehicle charging infrastructure, energy storage systems, and transmission network modernization. As governments invest in electrification and energy transition initiatives, demand for copper-intensive electrical equipment, cables, transformers, and grid technologies is expected to increase substantially.

The global Copper Market was valued at USD 265.50 billion in 2026 and is projected to reach USD 634.47 billion by 2036, registering a robust CAGR of 8.81% during the forecast period. Copper remains one of the world's most strategically important industrial metals due to its superior electrical conductivity, thermal efficiency, corrosion resistance, and recyclability. The metal plays a fundamental role across construction, power generation, electrical infrastructure, transportation, electronics, telecommunications, and industrial manufacturing sectors.

The market is entering a period of accelerated growth as global economies pursue electrification, renewable energy adoption, and carbon reduction initiatives. Increasing investments in electric vehicles, power transmission networks, smart grids, and clean energy infrastructure are significantly expanding copper demand. Simultaneously, rapid urbanization, industrialization, and technological innovation continue to strengthen consumption across both developed and emerging economies.

Copper has emerged as a critical enabler of the global energy transition due to its extensive use in renewable power systems, electric mobility solutions, and advanced electrical infrastructure. Electric vehicles require substantially more copper than conventional internal combustion engine vehicles, while solar farms, wind turbines, battery storage systems, and grid modernization projects rely heavily on copper-intensive components.

The growing digital economy is also supporting demand growth. Data centers, telecommunications infrastructure, semiconductors, consumer electronics, and industrial automation systems increasingly depend on copper for efficient energy transfer and connectivity. As governments continue to invest in sustainable infrastructure and industrial electrification programs, copper demand is expected to rise steadily throughout the forecast period.

Asia-Pacific remains the dominant force in the global copper market, accounting for the largest share of both production and consumption. China continues to lead global demand due to extensive infrastructure projects, renewable energy investments, electric vehicle manufacturing, and electronics production. India is also emerging as a significant growth market, supported by industrial expansion, urbanization, and power sector modernization initiatives.

North America is witnessing increasing copper demand due to government-backed infrastructure programs, grid modernization projects, and clean energy investments. The United States is actively strengthening domestic supply chains to support EV manufacturing, renewable energy deployment, and advanced industrial applications. Canada contributes significantly through mining activities and refining capacity expansion.

Europe continues to experience strong demand driven by renewable energy targets, industrial electrification, and electric mobility adoption. Germany, France, and the United Kingdom remain key consumers due to their investments in sustainable infrastructure and clean energy systems. The region's emphasis on recycling and circular economy practices further supports market stability.

Latin America remains a cornerstone of global copper production, with Chile and Peru serving as major exporters and mining investment destinations. Meanwhile, the Middle East and Africa are gradually increasing copper consumption through infrastructure development, renewable energy projects, and industrial diversification initiatives.

The copper market is highly competitive, characterized by the presence of global mining companies, integrated metal producers, refiners, and recycling specialists. Competitive differentiation increasingly depends on production efficiency, resource availability, sustainability initiatives, and downstream integration capabilities.

Major market participants are investing in mine expansions, new exploration projects, refining capacity upgrades, and recycling technologies to secure long-term supply. Companies are also adopting digital mining solutions, automation technologies, and carbon reduction strategies to improve operational efficiency and environmental performance.

Sustainability has become a critical competitive factor as customers increasingly prioritize responsibly sourced materials and low-carbon supply chains. Organizations with strong ESG performance, recycling capabilities, and transparent sourcing practices are expected to strengthen their market positions as demand for sustainable materials continues to grow.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 8.81 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Copper Type |

|

| The Segment Covered by Product Type |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report is developed using a comprehensive research framework that integrates extensive primary interviews, industry consultations, and detailed secondary research from reputable sources. The analysis combines quantitative market modeling with qualitative industry expertise to deliver reliable and actionable intelligence.

All market estimates undergo rigorous validation processes, including data triangulation, trend analysis, supply-demand assessments, and expert review. This methodology ensures a high degree of accuracy, consistency, and transparency, enabling stakeholders to make informed strategic decisions.

The study employs a structured combination of primary and secondary research methodologies. Secondary research includes the analysis of mining industry reports, government publications, commodity databases, corporate disclosures, trade statistics, and industry journals. Primary research involves interviews with mining executives, metal traders, refiners, manufacturers, industry experts, and procurement specialists.

Advanced forecasting models, demand-supply analysis, regional consumption assessments, and macroeconomic evaluations are applied to generate market projections. Data validation through triangulation and expert verification further strengthens the reliability of the report's findings.

This report has been prepared by a team of experienced metals and mining analysts, commodity market specialists, and industry researchers with extensive expertise in global resource markets. The research team combines technical knowledge, market intelligence, and advanced analytical methodologies to provide accurate, objective, and actionable insights.

Through continuous monitoring of commodity trends, mining investments, regulatory developments, sustainability initiatives, and technological advancements, our analysts deliver strategic intelligence that helps stakeholders navigate evolving market conditions and capitalize on emerging opportunities. The report reflects a commitment to research excellence, transparency, and industry relevance, making it a trusted resource for investors, producers, manufacturers, policymakers, and industry participants worldwide.

1. Executive Summary

1.1 Market Overview

1.2 Market Definition and Scope

1.3 Key Findings and Strategic Insights

1.4 Market Size Analysis (20262036)

1.5 Growth Outlook and Revenue Opportunity

1.6 Key Demand Drivers

1.7 Market Challenges and Risks

1.8 Emerging Opportunities

1.9 Regional Market Snapshot

1.10 Competitive Landscape Overview

2. Introduction to the Global Copper Market

2.1 Overview of Copper Industry

2.2 Importance of Copper in the Global Economy

2.3 Physical and Chemical Properties of Copper

2.4 Copper Value Chain Analysis

2.5 Historical Market Evolution

2.6 Current Industry Structure

2.7 Stakeholder Ecosystem Analysis

3. Market Size and Forecast Analysis

3.1 Global Market Revenue Analysis (20262036)

3.2 Historical Market Performance (20172024)

3.3 Base Year Assessment (2025)

3.4 Forecast Methodology

3.5 CAGR Analysis (20262036)

3.6 Incremental Revenue Opportunity Analysis

3.7 Demand-Supply Forecast Assessment

3.8 Scenario Analysis (Optimistic, Base, Conservative)

4. Industry Dynamics

4.1 Market Drivers

4.1.1 Renewable Energy Infrastructure Expansion

4.1.2 Rising Electric Vehicle Adoption

4.1.3 Grid Modernization Initiatives

4.1.4 Construction and Urbanization Growth

4.1.5 Industrial Automation Expansion

4.1.6 Telecommunications Infrastructure Development

4.2 Market Restraints

4.2.1 Copper Price Volatility

4.2.2 Environmental Regulations and Compliance Costs

4.2.3 Declining Ore Grades

4.2.4 Rising Mining and Processing Costs

4.2.5 Geopolitical Risks and Trade Disruptions

4.3 Market Opportunities

4.3.1 Energy Transition Investments

4.3.2 Growth in Copper Recycling

4.3.3 EV Charging Infrastructure Development

4.3.4 Smart Cities Expansion

4.3.5 Data Center Growth

4.3.6 Digital Infrastructure Investments

5. Market Trends and Emerging Technologies

5.1 Electrification Megatrend

5.2 Renewable Energy Adoption Trends

5.3 Copper Recycling and Circular Economy

5.4 Sustainable Mining Technologies

5.5 Digital Mining Solutions and Automation

5.6 AI and Data-Driven Mining Operations

5.7 ESG and Responsible Sourcing Trends

5.8 Low-Carbon Copper Production Initiatives

6. Copper Demand Analysis by Application

6.1 Electrical and Electronics Industry

6.2 Power Generation and Transmission

6.3 Renewable Energy Systems

6.4 Electric Vehicles and Automotive Industry

6.5 Building and Construction Sector

6.6 Telecommunications Infrastructure

6.7 Data Centers and Cloud Infrastructure

6.8 Industrial Machinery and Equipment

6.9 Consumer Goods and Appliances

6.10 Emerging Applications

7. Supply Chain and Value Chain Analysis

7.1 Copper Mining Industry Structure

7.2 Ore Extraction Process

7.3 Smelting and Refining Operations

7.4 Distribution Network Analysis

7.5 End-User Consumption Analysis

7.6 Supply Chain Risk Assessment

7.7 Logistics and Transportation Challenges

7.8 Raw Material Availability Analysis

8. Market Segmentation by Copper Type

8.1 Primary Copper

8.1.1 Market Size and Forecast

8.1.2 Production Analysis

8.1.3 Key Applications

8.1.4 Regional Demand Trends

8.2 Secondary Copper

8.2.1 Market Size and Forecast

8.2.2 Recycling Industry Assessment

8.2.3 Sustainability Benefits

8.2.4 Growth Prospects

9. Market Segmentation by Product Type

9.1 Cathodes & Blister Copper

9.1.1 Market Overview

9.1.2 Production Trends

9.1.3 Demand Analysis

9.2 Refined Copper

9.2.1 Market Size and Forecast

9.2.2 Industrial Applications

9.2.3 Growth Drivers

9.3 Copper Scrap

9.3.1 Recycling Market Analysis

9.3.2 Supply Dynamics

9.3.3 Circular Economy Impact

10. Market Segmentation by Copper Product Form

10.1 Wire

10.2 Rods

10.3 Bars & Sections

10.4 Flat Rolled Products

10.5 Tubes

10.6 Foils

For Each Segment:

Market Size & Forecast

Demand Analysis

Key Applications

Regional Outlook

Growth Opportunities

11. Market Segmentation by Form

11.1 Rods & Bars

11.2 Plates & Sheets

11.3 Wires & Cables

11.4 Tubes & Pipes

11.5 Foils & Strips

11.6 Powders

Each Segment Includes:

Revenue Analysis

Volume Analysis

Industry Applications

Regional Demand Trends

12. Market Segmentation by End-Use Industry

12.1 Electrical & Electronics

Cables

Wiring Systems

Transformers

12.2 Industrial Equipment

12.3 Transport

12.4 Infrastructure

12.5 Building & Construction

12.6 Renewable Energy

Solar Power Systems

Wind Energy Installations

Energy Storage Systems

12.7 Automotive

Electric Vehicles

Motors

Charging Infrastructure

12.8 Power Generation & Transmission

12.9 Telecommunications & Data Centers

12.10 Consumer Goods & Appliances

12.11 Others

13. Regional Market Analysis

13.1 North America

13.1.1 Market Overview

13.1.2 United States Analysis

13.1.3 Canada Analysis

13.1.4 Key Investments

13.1.5 Growth Opportunities

13.2 Europe

13.2.1 Market Overview

13.2.2 Germany

13.2.3 United Kingdom

13.2.4 France

13.2.5 Italy

13.2.6 Spain

13.2.7 Rest of Europe

13.3 Asia-Pacific

13.3.1 Market Overview

13.3.2 China

13.3.3 India

13.3.4 Japan

13.3.5 South Korea

13.3.6 Australia

13.3.7 Southeast Asia

13.4 Latin America

13.4.1 Brazil

13.4.2 Mexico

13.4.3 Argentina

13.4.4 Chile

13.4.5 Peru

13.5 Middle East & Africa

13.5.1 Saudi Arabia

13.5.2 UAE

13.5.3 South Africa

13.5.4 Rest of MEA

14. Country-Level Market Analysis

14.1 Top Copper Consuming Countries

14.2 Top Copper Producing Countries

14.3 Import-Export Analysis

14.4 Regulatory Landscape by Country

14.5 Investment Trends by Country

15. Competitive Landscape

15.1 Market Structure Analysis

15.2 Competitive Benchmarking

15.3 Market Share Analysis

15.4 Strategic Developments

15.5 Mergers & Acquisitions

15.6 Capacity Expansion Projects

15.7 New Exploration Projects

15.8 Sustainability Initiatives

16. Company Profiles

Profile Structure for Each Company:

Company Overview

Business Description

Product Portfolio

Financial Performance

Geographic Presence

Production Capacity

Strategic Initiatives

SWOT Analysis

Key Companies

Codelco

Freeport-McMoRan

BHP Group

Glencore plc

Southern Copper Corporation

Anglo American plc

Antofagasta plc

First Quantum Minerals Ltd.

Jiangxi Copper Corporation

Hindustan Copper Limited

Additional market participants

17. Sustainability and ESG Analysis

17.1 Environmental Impact Assessment

17.2 Carbon Emission Reduction Strategies

17.3 Responsible Mining Practices

17.4 Water Resource Management

17.5 Recycling and Circular Economy

17.6 ESG Benchmarking

18. Regulatory Framework

18.1 Mining Regulations

18.2 Environmental Policies

18.3 Trade Policies and Tariffs

18.4 Sustainability Standards

18.5 International Compliance Requirements

19. Strategic Recommendations

19.1 Investment Opportunities

19.2 Market Entry Strategies

19.3 Growth Strategies for Producers

19.4 Supply Security Recommendations

19.5 Sustainability Roadmap

19.6 Risk Mitigation Strategies

20. Research Methodology

20.1 Research Framework

20.2 Primary Research Methodology

20.3 Secondary Research Sources

20.4 Data Collection Process

20.5 Forecasting Models

20.6 Data Validation and Triangulation

20.7 Assumptions and Limitations

21. Appendix

21.1 Abbreviations and Acronyms

21.2 Glossary of Terms

21.3 List of Tables

21.4 List of Figures

21.5 References

21.6 About the Research Team

21.7 Customization Options

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 21 China Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global India Outdoor Air Pollution Control Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global India Outdoor Air Pollution Control Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global India Outdoor Air Pollution Control Market: market scenario

Fig.4 Global India Outdoor Air Pollution Control Market competitive outlook

Fig.5 Global India Outdoor Air Pollution Control Market driver analysis

Fig.6 Global India Outdoor Air Pollution Control Market restraint analysis

Fig.7 Global India Outdoor Air Pollution Control Market opportunity analysis

Fig.8 Global India Outdoor Air Pollution Control Market trends analysis

Fig.9 Global India Outdoor Air Pollution Control Market: Segment Analysis (Based on the scope)

Fig.10 Global India Outdoor Air Pollution Control Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

A license granted to one user. Rules or conditions might be applied for e.g. the use of electric files (PDFs) or printings, depending on product.

A license granted to multiple users.

A license granted to a single business site/establishment.

A license granted to all employees within organisation access to the product.

Immediate / Within 24-48 hours - Working days

Online Payments with PayPal and CCavenue

You can order a report by picking any of the payment methods which is bank wire or online payment through any Debit/Credit card or PayPal.

Hard Copy