The global Gas Separation Membrane Market was valued at USD 3.21 billion in 2026 and is projected to reach USD 6.47 billion by 2036, registering a CAGR of 7.72% during the forecast period. The market is experiencing steady expansion as industries increasingly adopt energy-efficient and environmentally sustainable gas processing technologies. Gas separation membranes enable the selective separation of gases from complex mixtures, supporting applications such as hydrogen purification, nitrogen generation, carbon dioxide capture, natural gas sweetening, oxygen enrichment, and biogas upgrading.

As industries seek to reduce emissions, improve process efficiency, and comply with increasingly stringent environmental regulations, membrane-based separation technologies are gaining preference over conventional gas processing methods. Their compact footprint, modular design, low energy consumption, and chemical-free operation make them particularly attractive for decentralized and industrial-scale gas treatment applications.

The growing emphasis on carbon reduction and clean energy development is further accelerating market adoption. Gas separation membranes are increasingly utilized in carbon capture and storage (CCS) projects, hydrogen production facilities, renewable natural gas processing, and industrial gas recovery systems. These technologies help improve operational efficiency while supporting sustainability objectives across multiple industries.

Additionally, rising investments in hydrogen infrastructure, renewable energy systems, carbon capture projects, and industrial gas generation are expected to create substantial growth opportunities throughout the forecast period. As governments and industries continue advancing decarbonization initiatives and energy transition strategies, gas separation membrane technologies are expected to play an increasingly important role in enabling cleaner and more efficient gas processing solutions worldwide.

The global Gas Separation Membrane Market is expected to witness steady growth throughout the forecast period, supported by increasing demand for efficient, cost-effective, and environmentally sustainable gas processing technologies. Industries across energy, chemicals, oil & gas, power generation, and manufacturing sectors are increasingly adopting membrane-based separation systems to improve operational efficiency, reduce energy consumption, and comply with evolving environmental regulations.

Growth is driven by increasing hydrogen production, carbon capture projects, renewable gas development, and industrial process optimization initiatives. The rising emphasis on clean hydrogen production and hydrogen purification is creating significant demand for advanced membrane technologies capable of delivering high-purity gas streams while reducing processing costs.

The market is also benefiting from growing investments in carbon capture, utilization, and storage (CCUS) projects, where gas separation membranes play a critical role in capturing and separating carbon dioxide emissions from industrial processes. Additionally, expanding renewable natural gas, biogas upgrading, and methane recovery projects are further supporting adoption across both industrial and utility-scale applications.

As industries continue prioritizing energy efficiency, emissions reduction, and process optimization, gas separation membrane technologies are expected to become increasingly important within modern gas treatment infrastructure. Their modular design, compact footprint, scalability, and lower operating costs compared to conventional separation methods are anticipated to support long-term market expansion through 2036.

The gas separation membrane industry is benefiting from accelerating investments in hydrogen infrastructure, carbon capture projects, renewable natural gas production, and industrial decarbonization initiatives. As industries seek energy-efficient alternatives to conventional gas processing technologies, membrane systems are becoming increasingly important across refining, petrochemicals, power generation, and clean energy applications.

Advancements in membrane materials, combined with growing regulatory pressure to reduce emissions, are expected to support long-term adoption of gas separation technologies. The market is also benefiting from increased deployment of decentralized gas processing systems and on-site industrial gas generation facilities.

Increasing demand for low-carbon industrial processes is accelerating adoption across the global gas separation membrane market. Industries are increasingly seeking technologies that can improve process efficiency while reducing energy consumption and emissions. Gas separation membranes provide an efficient alternative to conventional gas separation technologies such as cryogenic distillation and pressure swing adsorption, particularly in applications requiring flexible, modular, and energy-efficient operation.

Hydrogen purification has emerged as one of the most significant growth segments, supported by national hydrogen strategies across North America, Europe, and Asia-Pacific. Membrane systems are increasingly deployed in hydrogen production facilities, refineries, chemical plants, and fuel cell infrastructure to recover and purify hydrogen streams. Their ability to deliver high-purity hydrogen with lower operating costs and reduced environmental impact is strengthening market demand.

Simultaneously, rising demand for renewable natural gas and biomethane is driving adoption of membrane-based biogas upgrading technologies capable of separating methane from carbon dioxide and impurities. These systems play a critical role in converting biogas into pipeline-quality renewable gas while supporting circular economy and sustainability objectives.

As investments in hydrogen infrastructure, carbon capture projects, renewable gas development, and industrial decarbonization initiatives continue to expand, gas separation membranes are expected to witness increasing deployment across a wide range of applications. These developments position gas separation membranes as a critical enabling technology within the global decarbonization landscape and a key contributor to future low-carbon industrial systems.

Governments and industries are increasingly investing in carbon capture technologies to meet climate targets and reduce greenhouse gas emissions. Gas separation membranes provide an energy-efficient method for carbon dioxide removal from natural gas streams, industrial exhaust gases, and biogas facilities.

Hydrogen is emerging as a critical component of global energy transition strategies. Membrane systems play a vital role in hydrogen purification, recovery, and processing, supporting fuel cell applications, industrial hydrogen production, and clean energy infrastructure.

Industries such as electronics, pharmaceuticals, food processing, and wastewater treatment are increasingly adopting membrane-based nitrogen and oxygen generation systems to improve operational efficiency and reduce dependence on bulk gas supply.

Renewable energy policies and biomethane injection targets are driving demand for membrane systems capable of upgrading raw biogas into pipeline-quality renewable natural gas.

Variations in pressure, temperature, moisture, and contaminant levels can affect membrane performance and separation efficiency, requiring additional pretreatment infrastructure.

In large-scale applications requiring ultra-high purity levels, conventional technologies such as cryogenic separation and adsorption systems may remain more economically attractive.

Exposure to aggressive chemicals, oil contaminants, sulfur compounds, and extreme temperatures can reduce membrane lifespan and increase maintenance requirements.

In regions with low energy costs or limited environmental regulations, membrane systems may face slower adoption due to longer payback periods compared to conventional technologies.

Investments in hydrogen hubs, refueling stations, and industrial hydrogen production facilities are expected to create significant opportunities for membrane manufacturers.

Increasing biomethane production and renewable gas injection targets are driving demand for advanced membrane upgrading systems worldwide.

Innovations in mixed-matrix membranes, ceramic membranes, and hybrid materials are enhancing gas selectivity, durability, and operational performance across diverse applications.

As industries pursue sustainability goals and carbon neutrality commitments, gas separation membranes are expected to play a growing role in energy-efficient gas processing and emissions reduction initiatives.

North America continues to strengthen its position in the gas separation membrane market through expanding hydrogen production, carbon capture projects, and renewable natural gas infrastructure. The United States remains a major adopter of membrane technologies across refining, petrochemicals, natural gas processing, and emerging hydrogen hubs supported by federal clean energy initiatives.

Europe is experiencing strong growth driven by ambitious climate targets and industrial decarbonization strategies. Germany, France, the Netherlands, and the Nordic countries are investing heavily in hydrogen ecosystems, biomethane production, and carbon capture technologies that rely on advanced gas separation systems.

Asia-Pacific dominates global consumption due to its extensive industrial base and growing natural gas processing requirements. China leads regional demand across petrochemicals, refining, and chemical manufacturing, while Japan and South Korea focus on advanced membrane technologies supporting hydrogen purification and industrial gas generation.

Latin America is gradually increasing adoption of membrane-based gas treatment systems, particularly within agricultural biogas projects, fertilizer production, and refining operations. Meanwhile, the Middle East and Africa continue to deploy membrane technologies across oil & gas facilities, industrial gas processing plants, and emerging hydrogen production projects.

The gas separation membrane market is highly technology-driven, with competition centered around membrane selectivity, permeability, durability, and lifecycle performance. Manufacturers are investing heavily in advanced polymeric, ceramic, and mixed-matrix membrane technologies designed to improve efficiency while reducing operating costs.

Strategic partnerships between membrane suppliers, industrial gas companies, hydrogen developers, and energy infrastructure operators are accelerating technology commercialization. Companies capable of delivering complete turnkey solutions, including membrane modules, compression systems, controls, and remote monitoring capabilities, are gaining a competitive advantage.

The industry is also witnessing increasing focus on sustainability and regulatory compliance. Suppliers offering solutions that support carbon reduction, hydrogen production, renewable gas upgrading, and low-emission industrial processes are securing stronger market positions and long-term customer relationships.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 7.72 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Product Type |

|

| The Segment Covered by Material Type |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report is developed using a comprehensive research framework combining primary interviews, industry consultations, technical assessments, and secondary research from verified sources. The analysis incorporates perspectives from membrane manufacturers, industrial gas companies, energy developers, engineering firms, and industry experts to provide balanced and actionable market intelligence.

All market estimates and forecasts undergo rigorous validation through market triangulation, technology assessment, demand-supply analysis, and expert review processes. This methodology ensures high levels of accuracy, reliability, and transparency for strategic decision-making.

The study utilizes both qualitative and quantitative research methodologies to evaluate market performance and future growth prospects. Secondary research includes analysis of industry reports, company filings, patent databases, government policies, trade publications, and technical literature related to gas separation technologies.

Primary research involves interviews with senior executives, membrane technology specialists, industrial gas operators, hydrogen developers, EPC contractors, and regulatory stakeholders. Advanced forecasting models, regional demand analysis, technology adoption assessments, and market validation techniques are applied to generate accurate and dependable market projections.

This report has been prepared by a team of experienced industrial technology analysts, membrane separation specialists, and energy transition researchers with deep expertise in gas processing, clean energy technologies, and industrial sustainability solutions.

Through rigorous research methodologies and continuous monitoring of technological advancements, regulatory developments, investment trends, and industrial adoption patterns, the team delivers objective, data-driven insights that support informed business and investment decisions.

Combining technical expertise with advanced market intelligence capabilities, our analysts provide comprehensive assessments of market dynamics, competitive developments, emerging technologies, and future growth opportunities. This commitment to analytical excellence, transparency, and industry relevance ensures that the report serves as a trusted resource for manufacturers, technology providers, investors, energy companies, industrial operators, and policymakers worldwide.

Chapter 1. Executive Summary

1.1 Market Snapshot

1.2 Market Size & Forecast (2026-2036)

1.3 Key Findings

1.4 Analyst Insights

1.5 Strategic Recommendations

1.6 Winning Imperatives for Industry Participants

Chapter 2. Market Introduction

2.1 Market Definition

2.2 Market Scope

2.3 Market Segmentation Overview

2.4 Industry Value Chain Analysis

2.5 Industry Ecosystem Analysis

2.6 Stakeholder Analysis

Chapter 3. Research Methodology

3.1 Research Framework

3.2 Primary Research Methodology

3.3 Secondary Research Methodology

3.4 Data Triangulation Process

3.5 Market Size Estimation

3.6 Forecasting Assumptions

Chapter 4. Market Dynamics

4.1 Market Drivers

4.1.1 Rising Carbon Capture and Emissions Reduction Initiatives

4.1.2 Growing Hydrogen Economy Development

4.1.3 Expansion of Industrial Gas Generation Applications

4.1.4 Increasing Adoption of Biogas Upgrading Technologies

4.2 Market Restraints

4.2.1 Sensitivity to Feed Gas Conditions

4.2.2 Competition from Conventional Separation Technologies

4.2.3 Membrane Degradation in Harsh Operating Environments

4.2.4 Return on Investment Challenges

4.3 Market Opportunities

4.3.1 Expansion of Global Hydrogen Infrastructure

4.3.2 Growth of Renewable Natural Gas and Biomethane Projects

4.3.3 Development of Advanced Membrane Materials

4.3.4 Industrial Decarbonization and Clean Manufacturing

4.4 Industry Impact Analysis

4.5 Growth Analysis

4.6 Porterâs Five Forces Analysis

4.7 PESTLE Analysis

4.8 Supply Chain Analysis

4.9 Pricing Trend Analysis

Chapter 5. Global Gas Separation Membrane Market Size & Forecast (2026-2036)

5.1 Market Revenue Analysis (USD Billion)

5.2 Historical Market Analysis (2017-2024)

5.3 Base Year Analysis (2025)

5.4 Forecast Analysis (2026-2036)

5.5 Incremental Revenue Opportunity

5.6 Market Attractiveness Analysis

Chapter 6. Global Gas Separation Membrane Market Analysis, By Product Type

6.1 Overview

6.2 Polymeric Membranes

6.3 Inorganic Membranes

6.4 Metallic Membranes

Chapter 7. Global Gas Separation Membrane Market Analysis, By Material Type

7.1 Overview

7.2 Polyimide & Polyaramide

7.3 Cellulose Acetate

7.4 Polysulfone

7.5 Polycarbonate

7.6 Others

Chapter 8. Global Gas Separation Membrane Market Analysis, By Module Type

8.1 Overview

8.2 Hollow Fiber

8.3 Spiral Wound

8.4 Plate and Frame

8.5 Others

Chapter 9. Global Gas Separation Membrane Market Analysis, By Application

9.1 Overview

9.2 Nitrogen Separation

9.3 Oxygen Separation

9.4 Acid Gas Separation

9.5 Hydrogen Separation

9.6 Carbon Dioxide Removal

9.7 Vapor/Gas Separation

9.8 Air Dehydration

9.9 Others

Chapter 10. Global Gas Separation Membrane Market Analysis, By End-Use Industry

10.1 Overview

10.2 Chemicals

10.3 Petrochemicals and Oil & Gas

10.4 Food & Beverage

10.5 Power Generation

10.6 Pharmaceuticals

10.7 Pollution Control

10.8 Electronics

10.9 Wastewater Treatment

10.10 Others

Chapter 11. Regional Market Analysis

11.1 Global Regional Overview

11.2 North America

11.2.1 United States

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 United Kingdom

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Russia

11.3.7 Sweden

11.3.8 Denmark

11.3.9 Norway

11.3.10 Rest of Europe

11.4 Asia Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 Australia

11.4.5 South Korea

11.4.6 Thailand

11.4.7 Rest of Asia Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Colombia

11.5.5 Rest of Latin America

11.6 Middle East & Africa

11.6.1 South Africa

11.6.2 Saudi Arabia

11.6.3 UAE

11.6.4 Kuwait

11.6.5 Rest of Middle East & Africa

Chapter 12. Competitive Landscape

12.1 Market Share Analysis

12.2 Competitive Benchmarking

12.3 Strategic Developments

12.4 Mergers & Acquisitions

12.5 Partnerships & Collaborations

12.6 Investment & Expansion Strategies

12.7 Competitive Dashboard

Chapter 13. Company Profiles

13.1 Air Products and Chemicals, Inc.

13.2 Air Liquide Advanced Separations

13.3 Honeywell UOP

13.4 UBE Industries Ltd.

13.5 Parker Hannifin Corporation

13.6 Schlumberger Ltd.

13.7 Fujifilm Manufacturing Europe B.V.

13.8 Membrane Technology and Research, Inc.

13.9 Evonik Industries AG

13.10 DIC Corporation

13.11 Generon IGS

13.12 Hitachi Zosen Corporation

13.13 Zhejiang Yuanda Air Separation Equipment Co., Ltd.

13.14 Atlas Copco

13.15 Borsig GmbH

Chapter 14. Technology Trends & Industry Outlook

14.1 Advances in Polymeric Membrane Technologies

14.2 Development of Mixed-Matrix Membranes

14.3 Ceramic and Metallic Membrane Innovations

14.4 Carbon Capture & CCUS Technology Integration

14.5 Hydrogen Purification Technology Trends

14.6 Renewable Gas & Biomethane Upgrading Outlook

14.7 Future Industry Outlook

Chapter 15. Appendix

15.1 List of Abbreviations

15.2 List of Tables

15.3 List of Figures

15.4 References & Data Sources

15.5 Disclaimer

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 9 Germany Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 21 China Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Gas Separation Membrane Market: Market Scenario

Fig.4 Global Gas Separation Membrane Market Competitive Outlook

Fig.5 Global Gas Separation Membrane Market Driver Analysis

Fig.6 Global Gas Separation Membrane Market Restraint Analysis

Fig.7 Global Gas Separation Membrane Market Opportunity Analysis

Fig.8 Global Gas Separation Membrane Market Trends Analysis

Fig.9 Global Gas Separation Membrane Market: Segment Analysis (Based on the Scope)

Fig.10 Global Gas Separation Membrane Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

The global Gas Separation Membrane Market is projected to reach USD 6.47 billion by 2036, growing from USD 3.21 billion in 2026.

The Gas Separation Membrane Market is expected to register a CAGR of 7.72% between 2026 and 2036.

Key growth drivers include rising investments in hydrogen infrastructure, carbon capture and storage (CCS), renewable natural gas production, industrial decarbonization initiatives, and increasing demand for energy-efficient gas processing technologies.

Gas separation membranes are used for hydrogen purification, nitrogen generation, oxygen enrichment, carbon dioxide removal, natural gas sweetening, biogas upgrading, and industrial gas recovery applications.

Gas separation membranes play a critical role in hydrogen purification, recovery, and processing by delivering high-purity hydrogen streams with lower energy consumption and operating costs compared to conventional separation methods.

Asia-Pacific dominates the Gas Separation Membrane Market due to its large industrial base, expanding chemical manufacturing sector, and growing natural gas processing capacity.

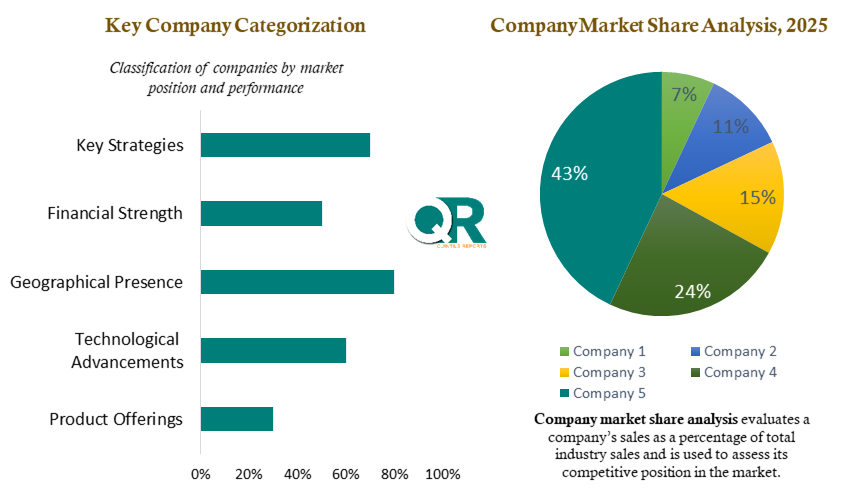

Major companies include Air Products and Chemicals, Inc., Air Liquide Advanced Separations, Honeywell UOP, Parker Hannifin Corporation, Evonik Industries AG, and other leading membrane technology providers.

The expansion of carbon capture, utilization, and storage (CCUS) projects is increasing demand for gas separation membranes, as these systems efficiently separate and capture carbon dioxide emissions from industrial processes and natural gas streams.

The global Gas Separation Membrane Market was valued at USD 3.21 billion in 2026 and is projected to reach USD 6.47 billion by 2036, registering a CAGR of 7.72% during the forecast period. The market is experiencing steady expansion as industries increasingly adopt energy-efficient and environmentally sustainable gas processing technologies. Gas separation membranes enable the selective separation of gases from complex mixtures, supporting applications such as hydrogen purification, nitrogen generation, carbon dioxide capture, natural gas sweetening, oxygen enrichment, and biogas upgrading.

As industries seek to reduce emissions, improve process efficiency, and comply with increasingly stringent environmental regulations, membrane-based separation technologies are gaining preference over conventional gas processing methods. Their compact footprint, modular design, low energy consumption, and chemical-free operation make them particularly attractive for decentralized and industrial-scale gas treatment applications.

The growing emphasis on carbon reduction and clean energy development is further accelerating market adoption. Gas separation membranes are increasingly utilized in carbon capture and storage (CCS) projects, hydrogen production facilities, renewable natural gas processing, and industrial gas recovery systems. These technologies help improve operational efficiency while supporting sustainability objectives across multiple industries.

Additionally, rising investments in hydrogen infrastructure, renewable energy systems, carbon capture projects, and industrial gas generation are expected to create substantial growth opportunities throughout the forecast period. As governments and industries continue advancing decarbonization initiatives and energy transition strategies, gas separation membrane technologies are expected to play an increasingly important role in enabling cleaner and more efficient gas processing solutions worldwide.

The global Gas Separation Membrane Market is expected to witness steady growth throughout the forecast period, supported by increasing demand for efficient, cost-effective, and environmentally sustainable gas processing technologies. Industries across energy, chemicals, oil & gas, power generation, and manufacturing sectors are increasingly adopting membrane-based separation systems to improve operational efficiency, reduce energy consumption, and comply with evolving environmental regulations.

Growth is driven by increasing hydrogen production, carbon capture projects, renewable gas development, and industrial process optimization initiatives. The rising emphasis on clean hydrogen production and hydrogen purification is creating significant demand for advanced membrane technologies capable of delivering high-purity gas streams while reducing processing costs.

The market is also benefiting from growing investments in carbon capture, utilization, and storage (CCUS) projects, where gas separation membranes play a critical role in capturing and separating carbon dioxide emissions from industrial processes. Additionally, expanding renewable natural gas, biogas upgrading, and methane recovery projects are further supporting adoption across both industrial and utility-scale applications.

As industries continue prioritizing energy efficiency, emissions reduction, and process optimization, gas separation membrane technologies are expected to become increasingly important within modern gas treatment infrastructure. Their modular design, compact footprint, scalability, and lower operating costs compared to conventional separation methods are anticipated to support long-term market expansion through 2036.

The gas separation membrane industry is benefiting from accelerating investments in hydrogen infrastructure, carbon capture projects, renewable natural gas production, and industrial decarbonization initiatives. As industries seek energy-efficient alternatives to conventional gas processing technologies, membrane systems are becoming increasingly important across refining, petrochemicals, power generation, and clean energy applications.

Advancements in membrane materials, combined with growing regulatory pressure to reduce emissions, are expected to support long-term adoption of gas separation technologies. The market is also benefiting from increased deployment of decentralized gas processing systems and on-site industrial gas generation facilities.

Increasing demand for low-carbon industrial processes is accelerating adoption across the global gas separation membrane market. Industries are increasingly seeking technologies that can improve process efficiency while reducing energy consumption and emissions. Gas separation membranes provide an efficient alternative to conventional gas separation technologies such as cryogenic distillation and pressure swing adsorption, particularly in applications requiring flexible, modular, and energy-efficient operation.

Hydrogen purification has emerged as one of the most significant growth segments, supported by national hydrogen strategies across North America, Europe, and Asia-Pacific. Membrane systems are increasingly deployed in hydrogen production facilities, refineries, chemical plants, and fuel cell infrastructure to recover and purify hydrogen streams. Their ability to deliver high-purity hydrogen with lower operating costs and reduced environmental impact is strengthening market demand.

Simultaneously, rising demand for renewable natural gas and biomethane is driving adoption of membrane-based biogas upgrading technologies capable of separating methane from carbon dioxide and impurities. These systems play a critical role in converting biogas into pipeline-quality renewable gas while supporting circular economy and sustainability objectives.

As investments in hydrogen infrastructure, carbon capture projects, renewable gas development, and industrial decarbonization initiatives continue to expand, gas separation membranes are expected to witness increasing deployment across a wide range of applications. These developments position gas separation membranes as a critical enabling technology within the global decarbonization landscape and a key contributor to future low-carbon industrial systems.

Governments and industries are increasingly investing in carbon capture technologies to meet climate targets and reduce greenhouse gas emissions. Gas separation membranes provide an energy-efficient method for carbon dioxide removal from natural gas streams, industrial exhaust gases, and biogas facilities.

Hydrogen is emerging as a critical component of global energy transition strategies. Membrane systems play a vital role in hydrogen purification, recovery, and processing, supporting fuel cell applications, industrial hydrogen production, and clean energy infrastructure.

Industries such as electronics, pharmaceuticals, food processing, and wastewater treatment are increasingly adopting membrane-based nitrogen and oxygen generation systems to improve operational efficiency and reduce dependence on bulk gas supply.

Renewable energy policies and biomethane injection targets are driving demand for membrane systems capable of upgrading raw biogas into pipeline-quality renewable natural gas.

Variations in pressure, temperature, moisture, and contaminant levels can affect membrane performance and separation efficiency, requiring additional pretreatment infrastructure.

In large-scale applications requiring ultra-high purity levels, conventional technologies such as cryogenic separation and adsorption systems may remain more economically attractive.

Exposure to aggressive chemicals, oil contaminants, sulfur compounds, and extreme temperatures can reduce membrane lifespan and increase maintenance requirements.

In regions with low energy costs or limited environmental regulations, membrane systems may face slower adoption due to longer payback periods compared to conventional technologies.

Investments in hydrogen hubs, refueling stations, and industrial hydrogen production facilities are expected to create significant opportunities for membrane manufacturers.

Increasing biomethane production and renewable gas injection targets are driving demand for advanced membrane upgrading systems worldwide.

Innovations in mixed-matrix membranes, ceramic membranes, and hybrid materials are enhancing gas selectivity, durability, and operational performance across diverse applications.

As industries pursue sustainability goals and carbon neutrality commitments, gas separation membranes are expected to play a growing role in energy-efficient gas processing and emissions reduction initiatives.

North America continues to strengthen its position in the gas separation membrane market through expanding hydrogen production, carbon capture projects, and renewable natural gas infrastructure. The United States remains a major adopter of membrane technologies across refining, petrochemicals, natural gas processing, and emerging hydrogen hubs supported by federal clean energy initiatives.

Europe is experiencing strong growth driven by ambitious climate targets and industrial decarbonization strategies. Germany, France, the Netherlands, and the Nordic countries are investing heavily in hydrogen ecosystems, biomethane production, and carbon capture technologies that rely on advanced gas separation systems.

Asia-Pacific dominates global consumption due to its extensive industrial base and growing natural gas processing requirements. China leads regional demand across petrochemicals, refining, and chemical manufacturing, while Japan and South Korea focus on advanced membrane technologies supporting hydrogen purification and industrial gas generation.

Latin America is gradually increasing adoption of membrane-based gas treatment systems, particularly within agricultural biogas projects, fertilizer production, and refining operations. Meanwhile, the Middle East and Africa continue to deploy membrane technologies across oil & gas facilities, industrial gas processing plants, and emerging hydrogen production projects.

The gas separation membrane market is highly technology-driven, with competition centered around membrane selectivity, permeability, durability, and lifecycle performance. Manufacturers are investing heavily in advanced polymeric, ceramic, and mixed-matrix membrane technologies designed to improve efficiency while reducing operating costs.

Strategic partnerships between membrane suppliers, industrial gas companies, hydrogen developers, and energy infrastructure operators are accelerating technology commercialization. Companies capable of delivering complete turnkey solutions, including membrane modules, compression systems, controls, and remote monitoring capabilities, are gaining a competitive advantage.

The industry is also witnessing increasing focus on sustainability and regulatory compliance. Suppliers offering solutions that support carbon reduction, hydrogen production, renewable gas upgrading, and low-emission industrial processes are securing stronger market positions and long-term customer relationships.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 7.72 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Product Type |

|

| The Segment Covered by Material Type |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report is developed using a comprehensive research framework combining primary interviews, industry consultations, technical assessments, and secondary research from verified sources. The analysis incorporates perspectives from membrane manufacturers, industrial gas companies, energy developers, engineering firms, and industry experts to provide balanced and actionable market intelligence.

All market estimates and forecasts undergo rigorous validation through market triangulation, technology assessment, demand-supply analysis, and expert review processes. This methodology ensures high levels of accuracy, reliability, and transparency for strategic decision-making.

The study utilizes both qualitative and quantitative research methodologies to evaluate market performance and future growth prospects. Secondary research includes analysis of industry reports, company filings, patent databases, government policies, trade publications, and technical literature related to gas separation technologies.

Primary research involves interviews with senior executives, membrane technology specialists, industrial gas operators, hydrogen developers, EPC contractors, and regulatory stakeholders. Advanced forecasting models, regional demand analysis, technology adoption assessments, and market validation techniques are applied to generate accurate and dependable market projections.

This report has been prepared by a team of experienced industrial technology analysts, membrane separation specialists, and energy transition researchers with deep expertise in gas processing, clean energy technologies, and industrial sustainability solutions.

Through rigorous research methodologies and continuous monitoring of technological advancements, regulatory developments, investment trends, and industrial adoption patterns, the team delivers objective, data-driven insights that support informed business and investment decisions.

Combining technical expertise with advanced market intelligence capabilities, our analysts provide comprehensive assessments of market dynamics, competitive developments, emerging technologies, and future growth opportunities. This commitment to analytical excellence, transparency, and industry relevance ensures that the report serves as a trusted resource for manufacturers, technology providers, investors, energy companies, industrial operators, and policymakers worldwide.

Chapter 1. Executive Summary

1.1 Market Snapshot

1.2 Market Size & Forecast (2026-2036)

1.3 Key Findings

1.4 Analyst Insights

1.5 Strategic Recommendations

1.6 Winning Imperatives for Industry Participants

Chapter 2. Market Introduction

2.1 Market Definition

2.2 Market Scope

2.3 Market Segmentation Overview

2.4 Industry Value Chain Analysis

2.5 Industry Ecosystem Analysis

2.6 Stakeholder Analysis

Chapter 3. Research Methodology

3.1 Research Framework

3.2 Primary Research Methodology

3.3 Secondary Research Methodology

3.4 Data Triangulation Process

3.5 Market Size Estimation

3.6 Forecasting Assumptions

Chapter 4. Market Dynamics

4.1 Market Drivers

4.1.1 Rising Carbon Capture and Emissions Reduction Initiatives

4.1.2 Growing Hydrogen Economy Development

4.1.3 Expansion of Industrial Gas Generation Applications

4.1.4 Increasing Adoption of Biogas Upgrading Technologies

4.2 Market Restraints

4.2.1 Sensitivity to Feed Gas Conditions

4.2.2 Competition from Conventional Separation Technologies

4.2.3 Membrane Degradation in Harsh Operating Environments

4.2.4 Return on Investment Challenges

4.3 Market Opportunities

4.3.1 Expansion of Global Hydrogen Infrastructure

4.3.2 Growth of Renewable Natural Gas and Biomethane Projects

4.3.3 Development of Advanced Membrane Materials

4.3.4 Industrial Decarbonization and Clean Manufacturing

4.4 Industry Impact Analysis

4.5 Growth Analysis

4.6 Porterâs Five Forces Analysis

4.7 PESTLE Analysis

4.8 Supply Chain Analysis

4.9 Pricing Trend Analysis

Chapter 5. Global Gas Separation Membrane Market Size & Forecast (2026-2036)

5.1 Market Revenue Analysis (USD Billion)

5.2 Historical Market Analysis (2017-2024)

5.3 Base Year Analysis (2025)

5.4 Forecast Analysis (2026-2036)

5.5 Incremental Revenue Opportunity

5.6 Market Attractiveness Analysis

Chapter 6. Global Gas Separation Membrane Market Analysis, By Product Type

6.1 Overview

6.2 Polymeric Membranes

6.3 Inorganic Membranes

6.4 Metallic Membranes

Chapter 7. Global Gas Separation Membrane Market Analysis, By Material Type

7.1 Overview

7.2 Polyimide & Polyaramide

7.3 Cellulose Acetate

7.4 Polysulfone

7.5 Polycarbonate

7.6 Others

Chapter 8. Global Gas Separation Membrane Market Analysis, By Module Type

8.1 Overview

8.2 Hollow Fiber

8.3 Spiral Wound

8.4 Plate and Frame

8.5 Others

Chapter 9. Global Gas Separation Membrane Market Analysis, By Application

9.1 Overview

9.2 Nitrogen Separation

9.3 Oxygen Separation

9.4 Acid Gas Separation

9.5 Hydrogen Separation

9.6 Carbon Dioxide Removal

9.7 Vapor/Gas Separation

9.8 Air Dehydration

9.9 Others

Chapter 10. Global Gas Separation Membrane Market Analysis, By End-Use Industry

10.1 Overview

10.2 Chemicals

10.3 Petrochemicals and Oil & Gas

10.4 Food & Beverage

10.5 Power Generation

10.6 Pharmaceuticals

10.7 Pollution Control

10.8 Electronics

10.9 Wastewater Treatment

10.10 Others

Chapter 11. Regional Market Analysis

11.1 Global Regional Overview

11.2 North America

11.2.1 United States

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 United Kingdom

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Russia

11.3.7 Sweden

11.3.8 Denmark

11.3.9 Norway

11.3.10 Rest of Europe

11.4 Asia Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 Australia

11.4.5 South Korea

11.4.6 Thailand

11.4.7 Rest of Asia Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Colombia

11.5.5 Rest of Latin America

11.6 Middle East & Africa

11.6.1 South Africa

11.6.2 Saudi Arabia

11.6.3 UAE

11.6.4 Kuwait

11.6.5 Rest of Middle East & Africa

Chapter 12. Competitive Landscape

12.1 Market Share Analysis

12.2 Competitive Benchmarking

12.3 Strategic Developments

12.4 Mergers & Acquisitions

12.5 Partnerships & Collaborations

12.6 Investment & Expansion Strategies

12.7 Competitive Dashboard

Chapter 13. Company Profiles

13.1 Air Products and Chemicals, Inc.

13.2 Air Liquide Advanced Separations

13.3 Honeywell UOP

13.4 UBE Industries Ltd.

13.5 Parker Hannifin Corporation

13.6 Schlumberger Ltd.

13.7 Fujifilm Manufacturing Europe B.V.

13.8 Membrane Technology and Research, Inc.

13.9 Evonik Industries AG

13.10 DIC Corporation

13.11 Generon IGS

13.12 Hitachi Zosen Corporation

13.13 Zhejiang Yuanda Air Separation Equipment Co., Ltd.

13.14 Atlas Copco

13.15 Borsig GmbH

Chapter 14. Technology Trends & Industry Outlook

14.1 Advances in Polymeric Membrane Technologies

14.2 Development of Mixed-Matrix Membranes

14.3 Ceramic and Metallic Membrane Innovations

14.4 Carbon Capture & CCUS Technology Integration

14.5 Hydrogen Purification Technology Trends

14.6 Renewable Gas & Biomethane Upgrading Outlook

14.7 Future Industry Outlook

Chapter 15. Appendix

15.1 List of Abbreviations

15.2 List of Tables

15.3 List of Figures

15.4 References & Data Sources

15.5 Disclaimer

Table 1 List of Abbreviation and Acronyms

Table 2 List of Sources

Table 3 North America Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 9 Germany Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 21 China Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Global Gas Separation Membrane Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Global Gas Separation Membrane Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market Research Process

Fig.2 Market Research Approaches

Fig.3 Global Gas Separation Membrane Market: Market Scenario

Fig.4 Global Gas Separation Membrane Market Competitive Outlook

Fig.5 Global Gas Separation Membrane Market Driver Analysis

Fig.6 Global Gas Separation Membrane Market Restraint Analysis

Fig.7 Global Gas Separation Membrane Market Opportunity Analysis

Fig.8 Global Gas Separation Membrane Market Trends Analysis

Fig.9 Global Gas Separation Membrane Market: Segment Analysis (Based on the Scope)

Fig.10 Global Gas Separation Membrane Market: Regional Analysis

Fig.11 Global Market Shares and Leading Market Players

Fig.12 North America Market Share and Leading Players

Fig.13 Europe Market Share and Leading Players

Fig.14 Asia Pacific Market Share and Leading Players

Fig.15 Latin America Market Share and Leading Players

Fig.16 Middle East & Africa Market Share and Leading Players

Fig.17 North America, by Country

Fig.18 North America

Fig.19 North America Market Estimates and Forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe Market Estimates and Forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific Market Estimates and Forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America Market Estimates and Forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa Market Estimates and Forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

A license granted to one user. Rules or conditions might be applied for e.g. the use of electric files (PDFs) or printings, depending on product.

A license granted to multiple users.

A license granted to a single business site/establishment.

A license granted to all employees within organisation access to the product.

Immediate / Within 24-48 hours - Working days

Online Payments with PayPal and CCavenue

You can order a report by picking any of the payment methods which is bank wire or online payment through any Debit/Credit card or PayPal.

Hard Copy