The global Semiconductor Manufacturing Equipment Market was valued at USD 120.21 billion in 2026 and is projected to reach USD 276.01 billion by 2036, expanding at a robust CAGR of 8.05% during the forecast period. The market is experiencing unprecedented growth as semiconductor manufacturers accelerate investments in advanced fabrication technologies to support rising demand for artificial intelligence (AI), high-performance computing, 5G infrastructure, autonomous vehicles, cloud data centers, and next-generation consumer electronics.

Semiconductor manufacturing equipment forms the foundation of the global electronics ecosystem, enabling the production of increasingly sophisticated chips through highly precise fabrication, assembly, packaging, and testing processes. As the industry advances toward smaller process nodes, higher transistor densities, and advanced packaging architectures, demand for cutting-edge lithography, deposition, etching, metrology, inspection, and testing equipment continues to surge. Furthermore, government-backed semiconductor initiatives, supply chain localization strategies, and large-scale fab construction projects worldwide are expected to drive substantial equipment spending throughout the forecast period.

The semiconductor manufacturing equipment industry is undergoing a transformative phase fueled by rapid technological innovation and escalating chip demand across multiple end-use sectors. The transition toward sub-5nm and emerging 2nm process technologies is significantly increasing the complexity of semiconductor fabrication, requiring advanced manufacturing tools capable of delivering unprecedented levels of precision, yield optimization, and process control.

At the same time, the explosive growth of artificial intelligence, machine learning, edge computing, electric vehicles, and 5G connectivity is creating strong demand for both leading-edge and mature-node semiconductors. This trend is encouraging foundries, integrated device manufacturers (IDMs), and outsourced semiconductor assembly and test (OSAT) providers to expand production capacity and invest heavily in advanced manufacturing equipment. The industry's growing adoption of smart factories, AI-powered process monitoring, robotics, and predictive maintenance solutions is further enhancing operational efficiency while supporting long-term market expansion.

The semiconductor manufacturing equipment market is segmented by equipment type, process, dimension, component, and end-use industry, reflecting the increasing complexity of semiconductor fabrication and packaging technologies. By equipment type, the market is broadly categorized into front-end and back-end equipment. Front-end equipment accounts for the largest share of industry revenue, as it is essential for wafer fabrication and advanced node production. Within this segment, lithography equipment remains a critical investment area due to the growing adoption of Extreme Ultraviolet (EUV) and Deep Ultraviolet (DUV) technologies for manufacturing advanced chips at smaller process nodes. Deposition equipment, including Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD) systems, continues to witness strong demand as chipmakers require highly precise thin-film deposition processes for next-generation semiconductor architectures. Etching, cleaning, ion implantation, and metrology & inspection equipment are also experiencing significant adoption as manufacturers focus on improving yield rates, process precision, and defect control.

The back-end equipment segment is gaining momentum with the rapid advancement of advanced packaging technologies. Assembly and packaging equipment, dicing systems, bonding equipment, and testing platforms play a crucial role in ensuring semiconductor performance, reliability, and miniaturization. Growing demand for heterogeneous integration, chiplet-based architectures, and advanced packaging solutions is driving investments in sophisticated back-end manufacturing tools. As semiconductor companies increasingly adopt advanced packaging techniques to enhance performance and power efficiency, demand for high-precision testing and bonding equipment is expected to rise substantially throughout the forecast period.

Based on process, the market is divided into front-end and back-end manufacturing operations. Front-end processes continue to dominate equipment spending due to the high capital intensity associated with wafer fabrication. Deposition technologies such as ALD and CVD are witnessing strong growth as manufacturers transition toward advanced process nodes requiring atomic-level precision. Lithography remains one of the most technologically advanced and capital-intensive segments, with EUV systems becoming increasingly important for producing leading-edge semiconductors. Etching processes, including plasma etch and gas chemical etch systems, are gaining prominence as chip designs become more complex and require highly accurate pattern transfer capabilities.

Cleaning equipment also represents a critical component of semiconductor manufacturing, as contamination control directly impacts production yield and device performance. Technologies such as single-wafer cleaning systems, cryokinetic cleaning systems, and batch spray cleaning systems are increasingly adopted to support advanced semiconductor production. Meanwhile, testing equipment continues to experience strong demand throughout both front-end and back-end operations, ensuring quality assurance, performance validation, and defect detection before products reach end markets.

Based on dimension, the market is segmented into 2D, 2.5D, and 3D semiconductor packaging technologies. Traditional 2D packaging continues to maintain a substantial market presence due to its widespread use in mainstream semiconductor applications. However, the increasing need for higher performance, reduced power consumption, and greater integration density is accelerating adoption of 2.5D and 3D packaging solutions. These advanced packaging approaches enable multiple chips to be integrated within compact form factors, making them highly suitable for artificial intelligence, high-performance computing, and data center applications. As demand for advanced computing capabilities grows, equipment supporting 2.5D and 3D integration technologies is expected to experience significant growth opportunities.

By component, the market is segmented into memory, logic, analog, MEMS, sensors, and other semiconductor devices. Logic devices account for a substantial share of equipment demand due to increasing production of processors used in artificial intelligence, cloud computing, and consumer electronics. Memory components continue to generate significant investments as demand for high-capacity DRAM and NAND flash technologies expands globally. Analog semiconductors remain critical across automotive, industrial, and telecommunications applications, while MEMS and sensor devices are witnessing growing demand due to their widespread use in smartphones, wearable devices, industrial automation systems, and connected vehicles. The diversification of semiconductor applications across industries continues to drive investments in specialized manufacturing equipment tailored to different component categories.

Based on end use, the semiconductor manufacturing equipment market serves consumer electronics, automotive, industrial, telecommunication, healthcare, aerospace & defense, and other sectors. Consumer electronics remains the largest end-use segment due to continuous demand for smartphones, laptops, tablets, gaming devices, and smart home technologies. The automotive sector is emerging as one of the fastest-growing segments, driven by the increasing semiconductor content in electric vehicles, autonomous driving systems, advanced driver assistance systems (ADAS), and vehicle connectivity platforms.

Telecommunication applications are generating substantial demand for advanced semiconductors as global 5G deployment accelerates and network infrastructure expands. The industrial sector is increasingly adopting semiconductor-enabled automation, robotics, and smart manufacturing solutions, further supporting equipment demand. Healthcare applications are benefiting from the growing use of medical imaging systems, diagnostic devices, wearable health technologies, and telemedicine infrastructure. Meanwhile, aerospace and defense organizations continue to invest in high-performance and mission-critical semiconductor technologies, creating additional opportunities for advanced semiconductor manufacturing equipment providers. Collectively, these diverse end-use industries are reinforcing long-term growth prospects for the global semiconductor manufacturing equipment market.

Asia-Pacific continues to dominate the semiconductor manufacturing equipment market due to the presence of leading semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan. The region benefits from strong government support, extensive supply chain networks, and continuous investments in advanced fabrication facilities. Chinas semiconductor self-sufficiency initiatives and large-scale capacity expansion programs are creating significant demand for manufacturing equipment across multiple process technologies.

North America is experiencing a resurgence in semiconductor manufacturing activity driven by strategic reshoring efforts and substantial public-sector funding. The United States continues to invest heavily in advanced fabrication facilities, semiconductor research centers, and workforce development programs under the CHIPS and Science Act. These initiatives are stimulating demand for advanced lithography, deposition, etching, and metrology equipment.

Europe is strengthening its semiconductor manufacturing ecosystem through the European Chips Act and collaborative technology development initiatives. Germany, the Netherlands, France, and other key markets are focusing on advanced process technologies, sustainable manufacturing practices, and supply chain resilience. The region's emphasis on technological sovereignty is expected to drive long-term equipment investments.

Japan and South Korea maintain their leadership positions in semiconductor equipment innovation, particularly across lithography, inspection, testing, and advanced manufacturing technologies. Meanwhile, Latin America and the Middle East & Africa are gradually expanding their participation in the semiconductor value chain through investments in electronics manufacturing, testing facilities, and technology infrastructure.

The rapid adoption of artificial intelligence, machine learning, and high-performance computing applications is driving substantial demand for advanced semiconductor devices. This trend is encouraging chip manufacturers to invest heavily in next-generation fabrication equipment capable of supporting complex chip architectures and higher transistor densities.

The transition toward sub-5nm, 3nm, and emerging 2nm semiconductor technologies is accelerating demand for advanced lithography, deposition, etching, and metrology equipment. Foundries and integrated device manufacturers are expanding fabrication capabilities to maintain competitiveness in leading-edge semiconductor production.

Governments across North America, Europe, and Asia-Pacific are implementing semiconductor incentive programs to strengthen domestic manufacturing capabilities and reduce supply chain dependencies. Initiatives such as the CHIPS Act and similar regional funding programs are driving significant investments in fabrication facilities and manufacturing equipment.

Growing cloud computing adoption, AI workloads, and digital transformation initiatives are fueling data center expansion worldwide. This surge in demand for high-performance processors, memory devices, and networking chips is creating strong opportunities for semiconductor equipment suppliers.

Semiconductor manufacturing equipment represents one of the most capital-intensive segments within the technology industry. The substantial cost of advanced lithography systems, inspection tools, and fabrication equipment can limit adoption, particularly among smaller semiconductor manufacturers.

Increasing geopolitical tensions and export regulations surrounding advanced semiconductor technologies are creating challenges for equipment manufacturers and chip producers. Restrictions on the sale of certain manufacturing tools may impact market expansion and international trade activities.

The semiconductor equipment industry relies on highly specialized global supply chains involving precision components, advanced materials, and critical technologies. Supply chain disruptions, logistics challenges, and material shortages can affect production schedules and equipment deliveries.

The industry's transition toward 2nm and beyond presents significant opportunities for equipment vendors developing advanced lithography, deposition, etching, and inspection solutions. Demand for highly sophisticated manufacturing technologies is expected to increase substantially as chipmakers pursue greater performance and energy efficiency.

Increasing adoption of 2.5D and 3D packaging, chiplet architectures, and heterogeneous integration is creating strong demand for advanced assembly, bonding, testing, and packaging equipment. Advanced packaging is becoming a critical enabler of semiconductor innovation beyond traditional node scaling.

Countries worldwide are investing in domestic semiconductor manufacturing to improve supply chain resilience and reduce reliance on foreign suppliers. These localization initiatives are driving new fab construction projects and creating long-term opportunities for semiconductor equipment providers.

The increasing semiconductor content in electric vehicles, autonomous driving systems, advanced driver assistance systems (ADAS), and connected vehicle technologies is creating significant growth opportunities. Automotive manufacturers continue to require advanced chips, driving investment in both mature-node and leading-edge semiconductor production capacity.

The increasing semiconductor content in electric vehicles, autonomous driving systems, advanced driver assistance systems (ADAS), and connected vehicle technologies is creating significant growth opportunities. Automotive manufacturers continue to require advanced chips, driving investment in both mature-node and leading-edge semiconductor production capacity.

The semiconductor manufacturing equipment market is highly concentrated and technology-driven, with competition centered on innovation, precision engineering, process expertise, and customer support capabilities. Leading manufacturers continuously invest billions of dollars in research and development to support next-generation semiconductor process technologies and increasingly complex chip architectures.

Equipment suppliers are focusing on developing advanced EUV lithography systems, high-precision deposition tools, AI-enabled inspection platforms, next-generation metrology systems, and advanced packaging solutions. The ability to support leading-edge process nodes, improve production yields, and reduce manufacturing costs remains a critical differentiator within the industry.

Strategic collaborations among equipment manufacturers, semiconductor foundries, integrated device manufacturers, and research institutions continue to accelerate technology development. Companies that provide comprehensive service ecosystems, global support infrastructure, and long-term process optimization capabilities are expected to maintain strong competitive positions as semiconductor manufacturing complexity continues to increase.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 8.05 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Equipment Type |

|

| The Segment Covered by Process |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report is built upon a rigorous research methodology designed to provide highly accurate, unbiased, and actionable market intelligence. The study combines extensive primary interviews with industry executives, semiconductor manufacturers, equipment suppliers, technology experts, and industry consultants alongside detailed secondary research from verified sources.

Every market estimate and forecast undergoes comprehensive validation using advanced analytical models, market triangulation techniques, and cross-verification processes. This ensures a high degree of reliability, consistency, and transparency throughout the study.

By integrating quantitative market analysis with qualitative industry expertise, the report delivers meaningful insights into technology trends, investment patterns, competitive developments, and future growth opportunities across the global semiconductor manufacturing equipment industry.

The research methodology for this study incorporates a combination of primary and secondary research techniques to ensure comprehensive market coverage and forecast accuracy. Secondary research includes analysis of company annual reports, semiconductor industry databases, government policy documents, trade publications, financial filings, technical journals, and industry association reports.

Primary research consists of extensive interviews with senior executives, process engineers, equipment manufacturers, semiconductor foundries, integrated device manufacturers, technology consultants, and industry specialists. These discussions provide valuable insights into inve

List of Tables

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 9 Germany Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 21 China Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Semiconductor Manufacturing Equipment Market: market scenario

Fig.4 Global Semiconductor Manufacturing Equipment Market competitive outlook

Fig.5 Global Semiconductor Manufacturing Equipment Market driver analysis

Fig.6 Global Semiconductor Manufacturing Equipment Market restraint analysis

Fig.7 Global Semiconductor Manufacturing Equipment Market opportunity analysis

Fig.8 Global Semiconductor Manufacturing Equipment Market trends analysis

Fig.9 Global Semiconductor Manufacturing Equipment Market: Segment Analysis (Based on the scope)

Fig.10 Global Semiconductor Manufacturing Equipment Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

List of Tables

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 9 Germany Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 21 China Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Semiconductor Manufacturing Equipment Market: market scenario

Fig.4 Global Semiconductor Manufacturing Equipment Market competitive outlook

Fig.5 Global Semiconductor Manufacturing Equipment Market driver analysis

Fig.6 Global Semiconductor Manufacturing Equipment Market restraint analysis

Fig.7 Global Semiconductor Manufacturing Equipment Market opportunity analysis

Fig.8 Global Semiconductor Manufacturing Equipment Market trends analysis

Fig.9 Global Semiconductor Manufacturing Equipment Market: Segment Analysis (Based on the scope)

Fig.10 Global Semiconductor Manufacturing Equipment Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

The global Semiconductor Manufacturing Equipment Market is projected to reach USD 276.01 billion by 2036, growing from USD 120.21 billion in 2026. Market growth is being driven by rising investments in advanced semiconductor fabrication facilities, increasing demand for AI and high-performance computing chips, and ongoing semiconductor localization initiatives.

The Semiconductor Manufacturing Equipment Market is expected to expand at a CAGR of 8.05% between 2026 and 2036. Growing adoption of advanced process nodes, increasing semiconductor demand across industries, and government-supported fab expansion projects are supporting long-term market growth.

Key growth drivers include increasing demand for artificial intelligence (AI) chips, expansion of cloud data centers, deployment of 5G infrastructure, growth in electric and autonomous vehicles, government semiconductor incentive programs, and rising investments in advanced semiconductor fabrication technologies.

Front-end semiconductor manufacturing equipment accounts for the largest share of the market due to its critical role in wafer fabrication and advanced chip production. Lithography, deposition, etching, metrology, and inspection systems remain major investment areas as manufacturers transition toward smaller process nodes and more complex chip architectures.

Asia-Pacific leads the global Semiconductor Manufacturing Equipment Market due to its extensive semiconductor manufacturing ecosystem, strong government support, and significant investments in fabrication facilities across China, Taiwan, South Korea, and Japan. The region remains the world's largest hub for semiconductor production and equipment deployment.

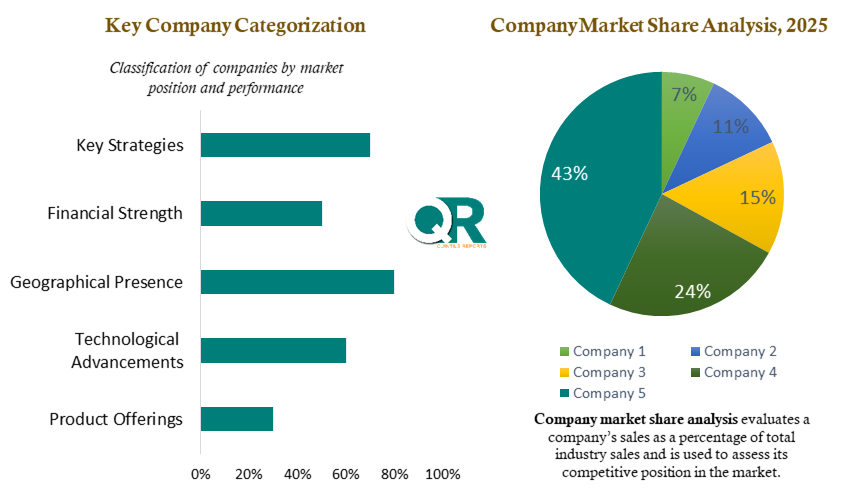

Major companies operating in the Semiconductor Manufacturing Equipment Market include ASML Holding N.V., Applied Materials Inc., Tokyo Electron Limited, Lam Research Corporation, KLA Corporation, Teradyne Inc., and Advantest Corporation.

Artificial intelligence is significantly increasing demand for advanced semiconductors used in AI training, machine learning, cloud computing, and high-performance computing applications. As semiconductor manufacturers expand production of AI-focused chips, investments in advanced lithography, deposition, etching, inspection, testing, and packaging equipment are accelerating to support next-generation semiconductor manufacturing requirements.

The global Semiconductor Manufacturing Equipment Market was valued at USD 120.21 billion in 2026 and is projected to reach USD 276.01 billion by 2036, expanding at a robust CAGR of 8.05% during the forecast period. The market is experiencing unprecedented growth as semiconductor manufacturers accelerate investments in advanced fabrication technologies to support rising demand for artificial intelligence (AI), high-performance computing, 5G infrastructure, autonomous vehicles, cloud data centers, and next-generation consumer electronics.

Semiconductor manufacturing equipment forms the foundation of the global electronics ecosystem, enabling the production of increasingly sophisticated chips through highly precise fabrication, assembly, packaging, and testing processes. As the industry advances toward smaller process nodes, higher transistor densities, and advanced packaging architectures, demand for cutting-edge lithography, deposition, etching, metrology, inspection, and testing equipment continues to surge. Furthermore, government-backed semiconductor initiatives, supply chain localization strategies, and large-scale fab construction projects worldwide are expected to drive substantial equipment spending throughout the forecast period.

The semiconductor manufacturing equipment industry is undergoing a transformative phase fueled by rapid technological innovation and escalating chip demand across multiple end-use sectors. The transition toward sub-5nm and emerging 2nm process technologies is significantly increasing the complexity of semiconductor fabrication, requiring advanced manufacturing tools capable of delivering unprecedented levels of precision, yield optimization, and process control.

At the same time, the explosive growth of artificial intelligence, machine learning, edge computing, electric vehicles, and 5G connectivity is creating strong demand for both leading-edge and mature-node semiconductors. This trend is encouraging foundries, integrated device manufacturers (IDMs), and outsourced semiconductor assembly and test (OSAT) providers to expand production capacity and invest heavily in advanced manufacturing equipment. The industry's growing adoption of smart factories, AI-powered process monitoring, robotics, and predictive maintenance solutions is further enhancing operational efficiency while supporting long-term market expansion.

The semiconductor manufacturing equipment market is segmented by equipment type, process, dimension, component, and end-use industry, reflecting the increasing complexity of semiconductor fabrication and packaging technologies. By equipment type, the market is broadly categorized into front-end and back-end equipment. Front-end equipment accounts for the largest share of industry revenue, as it is essential for wafer fabrication and advanced node production. Within this segment, lithography equipment remains a critical investment area due to the growing adoption of Extreme Ultraviolet (EUV) and Deep Ultraviolet (DUV) technologies for manufacturing advanced chips at smaller process nodes. Deposition equipment, including Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD) systems, continues to witness strong demand as chipmakers require highly precise thin-film deposition processes for next-generation semiconductor architectures. Etching, cleaning, ion implantation, and metrology & inspection equipment are also experiencing significant adoption as manufacturers focus on improving yield rates, process precision, and defect control.

The back-end equipment segment is gaining momentum with the rapid advancement of advanced packaging technologies. Assembly and packaging equipment, dicing systems, bonding equipment, and testing platforms play a crucial role in ensuring semiconductor performance, reliability, and miniaturization. Growing demand for heterogeneous integration, chiplet-based architectures, and advanced packaging solutions is driving investments in sophisticated back-end manufacturing tools. As semiconductor companies increasingly adopt advanced packaging techniques to enhance performance and power efficiency, demand for high-precision testing and bonding equipment is expected to rise substantially throughout the forecast period.

Based on process, the market is divided into front-end and back-end manufacturing operations. Front-end processes continue to dominate equipment spending due to the high capital intensity associated with wafer fabrication. Deposition technologies such as ALD and CVD are witnessing strong growth as manufacturers transition toward advanced process nodes requiring atomic-level precision. Lithography remains one of the most technologically advanced and capital-intensive segments, with EUV systems becoming increasingly important for producing leading-edge semiconductors. Etching processes, including plasma etch and gas chemical etch systems, are gaining prominence as chip designs become more complex and require highly accurate pattern transfer capabilities.

Cleaning equipment also represents a critical component of semiconductor manufacturing, as contamination control directly impacts production yield and device performance. Technologies such as single-wafer cleaning systems, cryokinetic cleaning systems, and batch spray cleaning systems are increasingly adopted to support advanced semiconductor production. Meanwhile, testing equipment continues to experience strong demand throughout both front-end and back-end operations, ensuring quality assurance, performance validation, and defect detection before products reach end markets.

Based on dimension, the market is segmented into 2D, 2.5D, and 3D semiconductor packaging technologies. Traditional 2D packaging continues to maintain a substantial market presence due to its widespread use in mainstream semiconductor applications. However, the increasing need for higher performance, reduced power consumption, and greater integration density is accelerating adoption of 2.5D and 3D packaging solutions. These advanced packaging approaches enable multiple chips to be integrated within compact form factors, making them highly suitable for artificial intelligence, high-performance computing, and data center applications. As demand for advanced computing capabilities grows, equipment supporting 2.5D and 3D integration technologies is expected to experience significant growth opportunities.

By component, the market is segmented into memory, logic, analog, MEMS, sensors, and other semiconductor devices. Logic devices account for a substantial share of equipment demand due to increasing production of processors used in artificial intelligence, cloud computing, and consumer electronics. Memory components continue to generate significant investments as demand for high-capacity DRAM and NAND flash technologies expands globally. Analog semiconductors remain critical across automotive, industrial, and telecommunications applications, while MEMS and sensor devices are witnessing growing demand due to their widespread use in smartphones, wearable devices, industrial automation systems, and connected vehicles. The diversification of semiconductor applications across industries continues to drive investments in specialized manufacturing equipment tailored to different component categories.

Based on end use, the semiconductor manufacturing equipment market serves consumer electronics, automotive, industrial, telecommunication, healthcare, aerospace & defense, and other sectors. Consumer electronics remains the largest end-use segment due to continuous demand for smartphones, laptops, tablets, gaming devices, and smart home technologies. The automotive sector is emerging as one of the fastest-growing segments, driven by the increasing semiconductor content in electric vehicles, autonomous driving systems, advanced driver assistance systems (ADAS), and vehicle connectivity platforms.

Telecommunication applications are generating substantial demand for advanced semiconductors as global 5G deployment accelerates and network infrastructure expands. The industrial sector is increasingly adopting semiconductor-enabled automation, robotics, and smart manufacturing solutions, further supporting equipment demand. Healthcare applications are benefiting from the growing use of medical imaging systems, diagnostic devices, wearable health technologies, and telemedicine infrastructure. Meanwhile, aerospace and defense organizations continue to invest in high-performance and mission-critical semiconductor technologies, creating additional opportunities for advanced semiconductor manufacturing equipment providers. Collectively, these diverse end-use industries are reinforcing long-term growth prospects for the global semiconductor manufacturing equipment market.

Asia-Pacific continues to dominate the semiconductor manufacturing equipment market due to the presence of leading semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan. The region benefits from strong government support, extensive supply chain networks, and continuous investments in advanced fabrication facilities. Chinas semiconductor self-sufficiency initiatives and large-scale capacity expansion programs are creating significant demand for manufacturing equipment across multiple process technologies.

North America is experiencing a resurgence in semiconductor manufacturing activity driven by strategic reshoring efforts and substantial public-sector funding. The United States continues to invest heavily in advanced fabrication facilities, semiconductor research centers, and workforce development programs under the CHIPS and Science Act. These initiatives are stimulating demand for advanced lithography, deposition, etching, and metrology equipment.

Europe is strengthening its semiconductor manufacturing ecosystem through the European Chips Act and collaborative technology development initiatives. Germany, the Netherlands, France, and other key markets are focusing on advanced process technologies, sustainable manufacturing practices, and supply chain resilience. The region's emphasis on technological sovereignty is expected to drive long-term equipment investments.

Japan and South Korea maintain their leadership positions in semiconductor equipment innovation, particularly across lithography, inspection, testing, and advanced manufacturing technologies. Meanwhile, Latin America and the Middle East & Africa are gradually expanding their participation in the semiconductor value chain through investments in electronics manufacturing, testing facilities, and technology infrastructure.

The rapid adoption of artificial intelligence, machine learning, and high-performance computing applications is driving substantial demand for advanced semiconductor devices. This trend is encouraging chip manufacturers to invest heavily in next-generation fabrication equipment capable of supporting complex chip architectures and higher transistor densities.

The transition toward sub-5nm, 3nm, and emerging 2nm semiconductor technologies is accelerating demand for advanced lithography, deposition, etching, and metrology equipment. Foundries and integrated device manufacturers are expanding fabrication capabilities to maintain competitiveness in leading-edge semiconductor production.

Governments across North America, Europe, and Asia-Pacific are implementing semiconductor incentive programs to strengthen domestic manufacturing capabilities and reduce supply chain dependencies. Initiatives such as the CHIPS Act and similar regional funding programs are driving significant investments in fabrication facilities and manufacturing equipment.

Growing cloud computing adoption, AI workloads, and digital transformation initiatives are fueling data center expansion worldwide. This surge in demand for high-performance processors, memory devices, and networking chips is creating strong opportunities for semiconductor equipment suppliers.

Semiconductor manufacturing equipment represents one of the most capital-intensive segments within the technology industry. The substantial cost of advanced lithography systems, inspection tools, and fabrication equipment can limit adoption, particularly among smaller semiconductor manufacturers.

Increasing geopolitical tensions and export regulations surrounding advanced semiconductor technologies are creating challenges for equipment manufacturers and chip producers. Restrictions on the sale of certain manufacturing tools may impact market expansion and international trade activities.

The semiconductor equipment industry relies on highly specialized global supply chains involving precision components, advanced materials, and critical technologies. Supply chain disruptions, logistics challenges, and material shortages can affect production schedules and equipment deliveries.

The industry's transition toward 2nm and beyond presents significant opportunities for equipment vendors developing advanced lithography, deposition, etching, and inspection solutions. Demand for highly sophisticated manufacturing technologies is expected to increase substantially as chipmakers pursue greater performance and energy efficiency.

Increasing adoption of 2.5D and 3D packaging, chiplet architectures, and heterogeneous integration is creating strong demand for advanced assembly, bonding, testing, and packaging equipment. Advanced packaging is becoming a critical enabler of semiconductor innovation beyond traditional node scaling.

Countries worldwide are investing in domestic semiconductor manufacturing to improve supply chain resilience and reduce reliance on foreign suppliers. These localization initiatives are driving new fab construction projects and creating long-term opportunities for semiconductor equipment providers.

The increasing semiconductor content in electric vehicles, autonomous driving systems, advanced driver assistance systems (ADAS), and connected vehicle technologies is creating significant growth opportunities. Automotive manufacturers continue to require advanced chips, driving investment in both mature-node and leading-edge semiconductor production capacity.

The increasing semiconductor content in electric vehicles, autonomous driving systems, advanced driver assistance systems (ADAS), and connected vehicle technologies is creating significant growth opportunities. Automotive manufacturers continue to require advanced chips, driving investment in both mature-node and leading-edge semiconductor production capacity.

The semiconductor manufacturing equipment market is highly concentrated and technology-driven, with competition centered on innovation, precision engineering, process expertise, and customer support capabilities. Leading manufacturers continuously invest billions of dollars in research and development to support next-generation semiconductor process technologies and increasingly complex chip architectures.

Equipment suppliers are focusing on developing advanced EUV lithography systems, high-precision deposition tools, AI-enabled inspection platforms, next-generation metrology systems, and advanced packaging solutions. The ability to support leading-edge process nodes, improve production yields, and reduce manufacturing costs remains a critical differentiator within the industry.

Strategic collaborations among equipment manufacturers, semiconductor foundries, integrated device manufacturers, and research institutions continue to accelerate technology development. Companies that provide comprehensive service ecosystems, global support infrastructure, and long-term process optimization capabilities are expected to maintain strong competitive positions as semiconductor manufacturing complexity continues to increase.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 8.05 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Equipment Type |

|

| The Segment Covered by Process |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This report is built upon a rigorous research methodology designed to provide highly accurate, unbiased, and actionable market intelligence. The study combines extensive primary interviews with industry executives, semiconductor manufacturers, equipment suppliers, technology experts, and industry consultants alongside detailed secondary research from verified sources.

Every market estimate and forecast undergoes comprehensive validation using advanced analytical models, market triangulation techniques, and cross-verification processes. This ensures a high degree of reliability, consistency, and transparency throughout the study.

By integrating quantitative market analysis with qualitative industry expertise, the report delivers meaningful insights into technology trends, investment patterns, competitive developments, and future growth opportunities across the global semiconductor manufacturing equipment industry.

The research methodology for this study incorporates a combination of primary and secondary research techniques to ensure comprehensive market coverage and forecast accuracy. Secondary research includes analysis of company annual reports, semiconductor industry databases, government policy documents, trade publications, financial filings, technical journals, and industry association reports.

Primary research consists of extensive interviews with senior executives, process engineers, equipment manufacturers, semiconductor foundries, integrated device manufacturers, technology consultants, and industry specialists. These discussions provide valuable insights into inve

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 9 Germany Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 21 China Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Semiconductor Manufacturing Equipment Market: market scenario

Fig.4 Global Semiconductor Manufacturing Equipment Market competitive outlook

Fig.5 Global Semiconductor Manufacturing Equipment Market driver analysis

Fig.6 Global Semiconductor Manufacturing Equipment Market restraint analysis

Fig.7 Global Semiconductor Manufacturing Equipment Market opportunity analysis

Fig.8 Global Semiconductor Manufacturing Equipment Market trends analysis

Fig.9 Global Semiconductor Manufacturing Equipment Market: Segment Analysis (Based on the scope)

Fig.10 Global Semiconductor Manufacturing Equipment Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 4 North America Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 5 U.S. Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 6 Canada Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 7 Europe Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 8 Europe Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 9 Germany Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 10 U.K. Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 11 France Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 12 Italy Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 13 Spain Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 14 Sweden Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 15 Denmark Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 16 Norway Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 17 The Netherlands Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 18 Russia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 19 Asia Pacific Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 20 Asia Pacific Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 21 China Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 22 Japan Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 23 India Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 24 Australia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 25 South Korea Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 26 Thailand Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 27 Latin America Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 28 Latin America Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 29 Brazil Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 30 Mexico Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 31 Argentina Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 32 Middle East and Africa Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 33 Middle East and Africa Global Semiconductor Manufacturing Equipment Market, by Region, (USD Million) 2017-2036

Table 34 South Africa Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 35 Saudi Arabia Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 36 UAE Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 37 Kuwait Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Table 38 Turkey Global Semiconductor Manufacturing Equipment Market, by Segment Analysis, (USD Million) 2017-2036

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Semiconductor Manufacturing Equipment Market: market scenario

Fig.4 Global Semiconductor Manufacturing Equipment Market competitive outlook

Fig.5 Global Semiconductor Manufacturing Equipment Market driver analysis

Fig.6 Global Semiconductor Manufacturing Equipment Market restraint analysis

Fig.7 Global Semiconductor Manufacturing Equipment Market opportunity analysis

Fig.8 Global Semiconductor Manufacturing Equipment Market trends analysis

Fig.9 Global Semiconductor Manufacturing Equipment Market: Segment Analysis (Based on the scope)

Fig.10 Global Semiconductor Manufacturing Equipment Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2036

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2036

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2036

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2036

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2036

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

A license granted to one user. Rules or conditions might be applied for e.g. the use of electric files (PDFs) or printings, depending on product.

A license granted to multiple users.

A license granted to a single business site/establishment.

A license granted to all employees within organisation access to the product.

Immediate / Within 24-48 hours - Working days

Online Payments with PayPal and CCavenue

You can order a report by picking any of the payment methods which is bank wire or online payment through any Debit/Credit card or PayPal.

Hard Copy