The Global Flame and Detonation Arrestors Market was valued at USD 2.61 billion in 2026 and is projected to reach USD 4.71 billion by 2036, expanding at a CAGR of 6.26% during the forecast period from 2026 to 2036. The report provides in-depth insights into flame arrestors and detonation arrestor systems, covering market size, growth drivers, industry trends, and future opportunities across key regions.

The flame and detonation arrestors market refers to the global and regional market for safety devices designed to prevent flame propagation and detonation through pipelines, vents, and process equipment that handle flammable gases and vapors. These passive systems utilize engineered metal elements, such as crimped ribbon or mesh structures, to absorb heat and quench flames or shockwaves, effectively halting combustion before it can spread to hazardous areas. Flame and detonation arrestors can be installed either inline or at the end of a system, allowing normal gas flow while disrupting ignition paths.

These arrestors are essential across a range of industries including oil and gas, chemicals, petrochemicals, power generation, pharmaceuticals, and mining. They are used to protect systems such as storage tanks, vapor recovery units, flare stacks, and engine exhausts from flame or explosion backflow. The market includes various designs suitable for different pressure levels, flow rates, and operating environments, catering to applications that require strict compliance with industrial safety regulations.

The Flame and Detonation Arrestors Market is primarily driven by increasing emphasis on industrial safety standards and explosion prevention across hazardous environments. Regulatory frameworks such as ATEX in Europe and NFPA guidelines in North America are compelling industries to adopt advanced flame arrestor systems to ensure compliance and operational safety.

Industries including oil and gas pumps market, petrochemicals, and power generation are increasingly integrating flame and detonation arrestors into critical infrastructure such as pipelines, storage tanks, and processing units. This growing adoption is supported by rising investments in industrial automation and safety system upgrades.

Technological advancements, including corrosion-resistant materials, high-efficiency flame quenching elements, and IoT-enabled monitoring systems, are further enhancing the performance and reliability of these devices. As industrial risk management becomes a priority, the demand for advanced explosion protection systems is expected to grow steadily.

With increasing incidents of industrial explosions and stricter global safety regulations, flame and detonation arrestors are becoming critical components in modern industrial safety and risk management systems.

Additionally, advancements in industrial processing technologies, as highlighted in the microreactor systems used in the microreactor technology market, are increasing the demand for advanced safety systems.

Overall, these explosion protection systems are widely used in industries handling flammable gases to prevent fire hazards and ensure operational safety.

The growing importance of worker safety is also reflected in industries such as the sandblasting PPE market, where protective equipment is essential for hazardous operations.

North America dominates the flame and detonation arrestors market due to stringent industrial safety regulations and the presence of established oil and gas, chemical, and power generation sectors. The U.S. leads in the adoption of explosion protection devices, driven by NFPA standards and OSHA mandates.

The demand for industrial safety equipment such as flame arrestor systems is increasing due to stricter compliance requirements across global markets.

Europe follows closely, with strong demand fueled by EU directives on explosion prevention and the widespread presence of refineries, biogas plants, and chemical processing facilities. Germany, the UK, and the Netherlands are leading adopters due to their advanced industrial bases and strict adherence to ATEX regulations. Technological upgrades in manufacturing plants and energy facilities are propelling the need for reliable flame and detonation arrestors across the region.

Asia-Pacific is experiencing rapid growth in demand for flame and detonation arrestors, particularly in China, India, and Japan. The expansion of petrochemical complexes, rising investments in industrial infrastructure, and growing awareness of explosion safety are driving market penetration. China and India are focusing on aligning with international safety norms, especially in oil storage, refineries, and gas distribution networks, which boosts the installation of such systems.

Latin America is gradually embracing flame and detonation arrestors, especially in Brazil and Mexico, where refining and chemical industries are expanding. Adoption is being encouraged by efforts to modernize industrial facilities and reduce fire hazards in volatile environments. However, budget constraints and inconsistent safety enforcement can hinder faster uptake.

Middle East & Africa are showing growing interest in flame and detonation arrestors, primarily in oil-rich nations such as Saudi Arabia, the UAE, and Nigeria. The increasing development of oil and gas infrastructure, combined with the necessity to comply with safety regulations in hazardous environments, is fostering market growth. These systems are becoming integral to fire prevention strategies in refineries, storage terminals, and gas processing plants across the region.

In the United States, the implementation of strict industrial safety standards by agencies like OSHA and the NFPA is a major driver for the adoption of flame and detonation arrestors. These devices are essential for preventing explosions in pipelines, storage tanks, and other process equipment across industries such as petrochemicals, refining, and pharmaceuticals. Their growing use is closely tied to the increasing regulatory emphasis on workplace safety and risk mitigation.

Additionally, the expansion of oil and gas infrastructure especially in shale basins like the Permian and Eagle Ford is boosting the demand for reliable explosion prevention systems. As companies invest in new pipelines, gas processing facilities, and storage units, flame and detonation arrestors are being deployed extensively to enhance operational safety and comply with federal safety codes.

Germanys strong focus on industrial safety, particularly in hazardous environments, is a key driver for the increased adoption of flame and detonation arrestors. Compliance with the European Unions ATEX directives, which regulate equipment used in explosive atmospheres, has compelled companies in sectors such as chemical manufacturing, oil & gas, and pharmaceuticals to integrate these safety systems into their operations.

Moreover, the countrys advanced industrial base and significant investments in process automation have heightened the need for reliable explosion prevention mechanisms. As facilities modernize to meet both production efficiency and stringent environmental and safety requirements, the demand for flame and detonation arrestors continues to rise across the German industrial landscape.

Japans commitment to high safety standards, especially in industries dealing with flammable gases and volatile chemicals, significantly drives the adoption of flame and detonation arrestors. Regulatory bodies enforce strict compliance with fire and explosion prevention norms, encouraging industries like petrochemicals, oil refining, and pharmaceuticals to install advanced protective systems.

Additionally, Japans frequent exposure to natural disasters like earthquakes and its dense industrial zones have amplified the need for robust risk mitigation measures. This has led to a growing demand for reliable explosion arrestor technologies to ensure operational safety and continuity, reinforcing their importance in critical infrastructure across the country.

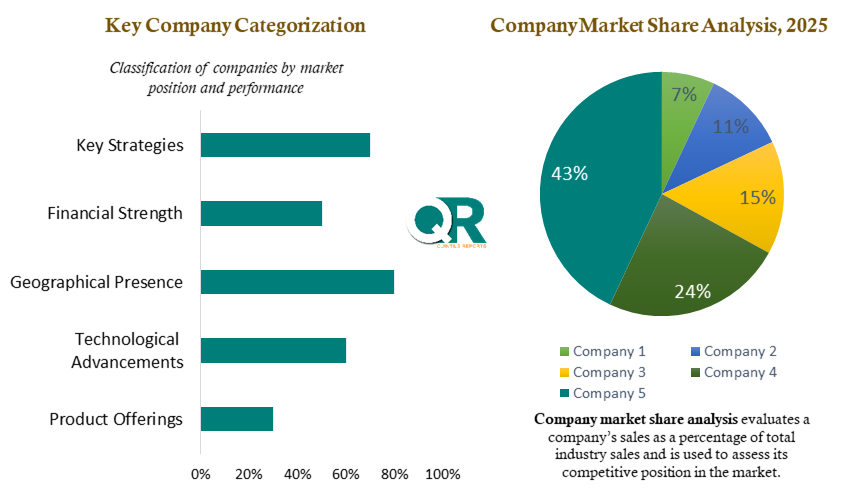

The Flame and Detonation Arrestors Market is highly competitive based on innovation in arrestor design, efficiency, and safety enhancements. Manufacturers are developing inline and end-of-line systems that meet rigorous standards and deliver over 95% flame or detonation prevention efficiency. Recent focus includes integrating IoT-enabled monitoring, predictive maintenance features, and modular skid-mounted solutions that support rapid deployment and high operational reliability across critical industrial sectors.

This shift allows companies to compete through deep technical expertise, scalable production capabilities, and configurability for specific flow rates and process conditions. Inline arrestors dominate with over 65% market share and are preferred for closed pipeline systems, while end-of-line devices are gaining ground rapidlyespecially in applications involving venting to atmosphere or storage tank protection.

Price competitiveness remains a critical factor, particularly for large safety system deployments in oil and gas, chemical, and petrochemical industries. Market concentration is moderate: leading firms hold around 3040% of global share, but regional and niche players aggressively compete on cost efficiency, especially in Asia-Pacific and Latin American markets.

An additional differentiator is geographic presence, service support, and turnkey integration. Companies offering local manufacturing hubs, retrofit solutions, installation services, remote diagnostics, and carbon credit validation are better able to serve global clients and reduce lead times while enhancing long-term relationships.

Sustainability positioning, regulatory alignment, and integration with broader safety or emissions-control systems are emerging as strategic advantages. Firms advancing smart arrestor designs, low-carbon processing, and systems that support hydrogen or energy recovery applications are gaining traction especially in regions with stringent industrial safety mandates such as North America, Europe, and Asia-Pacific.

Manufacturers are increasingly focusing on advanced explosion prevention equipment to improve operational safety and regulatory compliance.

Material innovations in industrial components, similar to developments in the aluminum billets market, are also influencing the design and durability of flame arrestor systems.

This section delivers an in-depth assessment of the competitive landscape within the Flame and Detonation Arrestors market. It identifies key players and evaluates their market positioning, strategic initiatives, and core strengths. The company profiles include business overview, product and service portfolios, financial performance, and geographic presence. The analysis also highlights recent developments such as partnerships, mergers, product launches, and expansion strategies, helping stakeholders understand competitive intensity and benchmark industry leaders.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 6.26 from 2026 to 2035 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2035 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2035 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Type |

|

| The Segment Covered by Orientation |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, and trends |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

The Flame and Detonation Arrestors market report provides detailed insights into market size, share, and growth trends for 2025, along with a comprehensive forecast outlook through 2035. The study combines historical analysis with future projections to deliver a complete market perspective. To request a sample PDF or obtain further information, contact our analyst team at sales@quintilereports.com.

List of Tables

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 21 China Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Flame and Detonation Arrestors Market: market scenario

Fig.4 Global Flame and Detonation Arrestors Market competitive outlook

Fig.5 Global Flame and Detonation Arrestors Market driver analysis

Fig.6 Global Flame and Detonation Arrestors Market restraint analysis

Fig.7 Global Flame and Detonation Arrestors Market opportunity analysis

Fig.8 Global Flame and Detonation Arrestors Market trends analysis

Fig.9 Global Flame and Detonation Arrestors Market: Segment Analysis (Based on the scope)

Fig.10 Global Flame and Detonation Arrestors Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

List of Tables

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 21 China Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Flame and Detonation Arrestors Market: market scenario

Fig.4 Global Flame and Detonation Arrestors Market competitive outlook

Fig.5 Global Flame and Detonation Arrestors Market driver analysis

Fig.6 Global Flame and Detonation Arrestors Market restraint analysis

Fig.7 Global Flame and Detonation Arrestors Market opportunity analysis

Fig.8 Global Flame and Detonation Arrestors Market trends analysis

Fig.9 Global Flame and Detonation Arrestors Market: Segment Analysis (Based on the scope)

Fig.10 Global Flame and Detonation Arrestors Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Major challenges include: (High installation and maintenance costs, Complex regulatory compliance, Performance degradation due to clogging and corrosion)

Key trends include: (Integration of IoT-enabled monitoring systems, Development of corrosion-resistant materials, Adoption of modular and high-efficiency arrestor designs)

The Flame and Detonation Arrestors Market refers to the global industry focused on the production and deployment of safety devices designed to prevent flame propagation and detonation in pipelines, storage systems, and industrial equipment handling flammable gases and vapors.

The Global Flame and Detonation Arrestors Market was valued at USD 2.61 billion in 2026 and is projected to reach USD 4.71 billion by 2036, expanding at a CAGR of 6.26% during the forecast period from 2026 to 2036. The report provides in-depth insights into flame arrestors and detonation arrestor systems, covering market size, growth drivers, industry trends, and future opportunities across key regions.

The flame and detonation arrestors market refers to the global and regional market for safety devices designed to prevent flame propagation and detonation through pipelines, vents, and process equipment that handle flammable gases and vapors. These passive systems utilize engineered metal elements, such as crimped ribbon or mesh structures, to absorb heat and quench flames or shockwaves, effectively halting combustion before it can spread to hazardous areas. Flame and detonation arrestors can be installed either inline or at the end of a system, allowing normal gas flow while disrupting ignition paths.

These arrestors are essential across a range of industries including oil and gas, chemicals, petrochemicals, power generation, pharmaceuticals, and mining. They are used to protect systems such as storage tanks, vapor recovery units, flare stacks, and engine exhausts from flame or explosion backflow. The market includes various designs suitable for different pressure levels, flow rates, and operating environments, catering to applications that require strict compliance with industrial safety regulations.

The Flame and Detonation Arrestors Market is primarily driven by increasing emphasis on industrial safety standards and explosion prevention across hazardous environments. Regulatory frameworks such as ATEX in Europe and NFPA guidelines in North America are compelling industries to adopt advanced flame arrestor systems to ensure compliance and operational safety.

Industries including oil and gas pumps market, petrochemicals, and power generation are increasingly integrating flame and detonation arrestors into critical infrastructure such as pipelines, storage tanks, and processing units. This growing adoption is supported by rising investments in industrial automation and safety system upgrades.

Technological advancements, including corrosion-resistant materials, high-efficiency flame quenching elements, and IoT-enabled monitoring systems, are further enhancing the performance and reliability of these devices. As industrial risk management becomes a priority, the demand for advanced explosion protection systems is expected to grow steadily.

With increasing incidents of industrial explosions and stricter global safety regulations, flame and detonation arrestors are becoming critical components in modern industrial safety and risk management systems.

Additionally, advancements in industrial processing technologies, as highlighted in the microreactor systems used in the microreactor technology market, are increasing the demand for advanced safety systems.

Overall, these explosion protection systems are widely used in industries handling flammable gases to prevent fire hazards and ensure operational safety.

The growing importance of worker safety is also reflected in industries such as the sandblasting PPE market, where protective equipment is essential for hazardous operations.

North America dominates the flame and detonation arrestors market due to stringent industrial safety regulations and the presence of established oil and gas, chemical, and power generation sectors. The U.S. leads in the adoption of explosion protection devices, driven by NFPA standards and OSHA mandates.

The demand for industrial safety equipment such as flame arrestor systems is increasing due to stricter compliance requirements across global markets.

Europe follows closely, with strong demand fueled by EU directives on explosion prevention and the widespread presence of refineries, biogas plants, and chemical processing facilities. Germany, the UK, and the Netherlands are leading adopters due to their advanced industrial bases and strict adherence to ATEX regulations. Technological upgrades in manufacturing plants and energy facilities are propelling the need for reliable flame and detonation arrestors across the region.

Asia-Pacific is experiencing rapid growth in demand for flame and detonation arrestors, particularly in China, India, and Japan. The expansion of petrochemical complexes, rising investments in industrial infrastructure, and growing awareness of explosion safety are driving market penetration. China and India are focusing on aligning with international safety norms, especially in oil storage, refineries, and gas distribution networks, which boosts the installation of such systems.

Latin America is gradually embracing flame and detonation arrestors, especially in Brazil and Mexico, where refining and chemical industries are expanding. Adoption is being encouraged by efforts to modernize industrial facilities and reduce fire hazards in volatile environments. However, budget constraints and inconsistent safety enforcement can hinder faster uptake.

Middle East & Africa are showing growing interest in flame and detonation arrestors, primarily in oil-rich nations such as Saudi Arabia, the UAE, and Nigeria. The increasing development of oil and gas infrastructure, combined with the necessity to comply with safety regulations in hazardous environments, is fostering market growth. These systems are becoming integral to fire prevention strategies in refineries, storage terminals, and gas processing plants across the region.

In the United States, the implementation of strict industrial safety standards by agencies like OSHA and the NFPA is a major driver for the adoption of flame and detonation arrestors. These devices are essential for preventing explosions in pipelines, storage tanks, and other process equipment across industries such as petrochemicals, refining, and pharmaceuticals. Their growing use is closely tied to the increasing regulatory emphasis on workplace safety and risk mitigation.

Additionally, the expansion of oil and gas infrastructure especially in shale basins like the Permian and Eagle Ford is boosting the demand for reliable explosion prevention systems. As companies invest in new pipelines, gas processing facilities, and storage units, flame and detonation arrestors are being deployed extensively to enhance operational safety and comply with federal safety codes.

Germanys strong focus on industrial safety, particularly in hazardous environments, is a key driver for the increased adoption of flame and detonation arrestors. Compliance with the European Unions ATEX directives, which regulate equipment used in explosive atmospheres, has compelled companies in sectors such as chemical manufacturing, oil & gas, and pharmaceuticals to integrate these safety systems into their operations.

Moreover, the countrys advanced industrial base and significant investments in process automation have heightened the need for reliable explosion prevention mechanisms. As facilities modernize to meet both production efficiency and stringent environmental and safety requirements, the demand for flame and detonation arrestors continues to rise across the German industrial landscape.

Japans commitment to high safety standards, especially in industries dealing with flammable gases and volatile chemicals, significantly drives the adoption of flame and detonation arrestors. Regulatory bodies enforce strict compliance with fire and explosion prevention norms, encouraging industries like petrochemicals, oil refining, and pharmaceuticals to install advanced protective systems.

Additionally, Japans frequent exposure to natural disasters like earthquakes and its dense industrial zones have amplified the need for robust risk mitigation measures. This has led to a growing demand for reliable explosion arrestor technologies to ensure operational safety and continuity, reinforcing their importance in critical infrastructure across the country.

The Flame and Detonation Arrestors Market is highly competitive based on innovation in arrestor design, efficiency, and safety enhancements. Manufacturers are developing inline and end-of-line systems that meet rigorous standards and deliver over 95% flame or detonation prevention efficiency. Recent focus includes integrating IoT-enabled monitoring, predictive maintenance features, and modular skid-mounted solutions that support rapid deployment and high operational reliability across critical industrial sectors.

This shift allows companies to compete through deep technical expertise, scalable production capabilities, and configurability for specific flow rates and process conditions. Inline arrestors dominate with over 65% market share and are preferred for closed pipeline systems, while end-of-line devices are gaining ground rapidlyespecially in applications involving venting to atmosphere or storage tank protection.

Price competitiveness remains a critical factor, particularly for large safety system deployments in oil and gas, chemical, and petrochemical industries. Market concentration is moderate: leading firms hold around 3040% of global share, but regional and niche players aggressively compete on cost efficiency, especially in Asia-Pacific and Latin American markets.

An additional differentiator is geographic presence, service support, and turnkey integration. Companies offering local manufacturing hubs, retrofit solutions, installation services, remote diagnostics, and carbon credit validation are better able to serve global clients and reduce lead times while enhancing long-term relationships.

Sustainability positioning, regulatory alignment, and integration with broader safety or emissions-control systems are emerging as strategic advantages. Firms advancing smart arrestor designs, low-carbon processing, and systems that support hydrogen or energy recovery applications are gaining traction especially in regions with stringent industrial safety mandates such as North America, Europe, and Asia-Pacific.

Manufacturers are increasingly focusing on advanced explosion prevention equipment to improve operational safety and regulatory compliance.

Material innovations in industrial components, similar to developments in the aluminum billets market, are also influencing the design and durability of flame arrestor systems.

This section delivers an in-depth assessment of the competitive landscape within the Flame and Detonation Arrestors market. It identifies key players and evaluates their market positioning, strategic initiatives, and core strengths. The company profiles include business overview, product and service portfolios, financial performance, and geographic presence. The analysis also highlights recent developments such as partnerships, mergers, product launches, and expansion strategies, helping stakeholders understand competitive intensity and benchmark industry leaders.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 6.26 from 2026 to 2035 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2035 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2035 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Type |

|

| The Segment Covered by Orientation |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, and trends |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

The Flame and Detonation Arrestors market report provides detailed insights into market size, share, and growth trends for 2025, along with a comprehensive forecast outlook through 2035. The study combines historical analysis with future projections to deliver a complete market perspective. To request a sample PDF or obtain further information, contact our analyst team at sales@quintilereports.com.

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 21 China Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Flame and Detonation Arrestors Market: market scenario

Fig.4 Global Flame and Detonation Arrestors Market competitive outlook

Fig.5 Global Flame and Detonation Arrestors Market driver analysis

Fig.6 Global Flame and Detonation Arrestors Market restraint analysis

Fig.7 Global Flame and Detonation Arrestors Market opportunity analysis

Fig.8 Global Flame and Detonation Arrestors Market trends analysis

Fig.9 Global Flame and Detonation Arrestors Market: Segment Analysis (Based on the scope)

Fig.10 Global Flame and Detonation Arrestors Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 21 China Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global Flame and Detonation Arrestors Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global Flame and Detonation Arrestors Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Flame and Detonation Arrestors Market: market scenario

Fig.4 Global Flame and Detonation Arrestors Market competitive outlook

Fig.5 Global Flame and Detonation Arrestors Market driver analysis

Fig.6 Global Flame and Detonation Arrestors Market restraint analysis

Fig.7 Global Flame and Detonation Arrestors Market opportunity analysis

Fig.8 Global Flame and Detonation Arrestors Market trends analysis

Fig.9 Global Flame and Detonation Arrestors Market: Segment Analysis (Based on the scope)

Fig.10 Global Flame and Detonation Arrestors Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

A license granted to one user. Rules or conditions might be applied for e.g. the use of electric files (PDFs) or printings, depending on product.

A license granted to multiple users.

A license granted to a single business site/establishment.

A license granted to all employees within organisation access to the product.

Immediate / Within 24-48 hours - Working days

Online Payments with PayPal and CCavenue

You can order a report by picking any of the payment methods which is bank wire or online payment through any Debit/Credit card or PayPal.

Hard Copy

Aramid Fiber Market Overview The global Aramid Fiber Market was valued at USD 4.98 billion in 2026 a

Read MoreConcrete Market Overview The global concrete market forms the backbone of modern construction, provi

Read MoreSilicon Carbide Market Overview The global Silicon Carbide (SiC) Market was valued at USD 7.52 billi

Read More