The global Fresh Yeast Market was valued at USD 4.10 Billion in 2026 and is projected to reach USD 8.81 Billion by 2036, growing at a CAGR of 7.72% over the forecast period. Doubling in value over a single decade is no small feat for what is, at its core, one of humanity's oldest fermentation tools but fresh yeast is proving that tradition and growth can absolutely coexist.

The numbers are compelling, but the more interesting story is why. Behind that trajectory sits a global shift in how people relate to food: a renewed appetite for handcrafted breads, clean ingredients, and cooking from scratch. Fresh yeast sits right at the center of that shift.

This report provides detailed Fresh Yeast market size analysis, growth trends, competitive benchmarking, and future industry outlook.

Fresh yeast, also referred to as baker's yeast or compressed yeast, is a living, biologically active form of Saccharomyces cerevisiae the same species of single-celled fungi central to human food production for thousands of years. Unlike dried counterparts, fresh yeast is sold in its hydrated, metabolically active state, with yeast cells alive and ready to ferment sugars immediately upon contact with the right environment.

Fresh yeast carries a moisture content of approximately 70%, giving it that soft, crumbly, pale beige texture most bakers recognize. It is commercially available in three main forms:

What fundamentally sets fresh yeast apart from active dry or instant yeast is biological state. Dehydration arrests yeast cell metabolism and extends shelf life but introduces measurable loss of leavening power. Fresh yeast cells are whole, viable, and metabolically primed, delivering faster fermentation onset, more even gas production, and particularly in enriched or laminated doughs a cleaner, more complex flavor profile. The live cells consume fermentable sugars and produce carbon dioxide (creating structure and lightness) and ethanol (contributing aroma and depth), along with organic acids and esters that chemical leaveners simply cannot replicate.

The trade-off is perishability. Fresh yeast requires continuous refrigeration between 0C and 8C, with a shelf life of just 2 to 4 weeks versus 12 years for dry yeast. That cold-chain dependency makes it logistically demanding, which is why dry alternatives have gained ground in home baking and remote markets. Beyond baking, fresh yeast serves beverage fermentation, bioethanol production, and nutraceutical formulations valued for B vitamins, proteins, and probiotic characteristics. The closely related Yeast Extracts and Beta Glucan market spanning bakery, health food, cosmetics, and medicines shares many of fresh yeast's end-use growth drivers.

The fresh yeast market's growth is driven by several reinforcing trends happening simultaneously.

No honest market analysis glosses over the friction points and fresh yeast has some genuine structural ones.

North America's fresh yeast market is being shaped by two converging forces: the professionalization of the artisan bakery sector and the sustained post-pandemic interest in home baking. The U.S. in particular has seen a wave of independent bakeries built around long-fermentation, naturally leavened, and enriched-dough products that genuinely benefit from fresh yeast's fermentation characteristics.

At the retail level, fresh yeast availability remains patchy compared to Europe not every grocery chain stocks it, and formats are often limited. But that's slowly changing as specialty food retailers expand baking ingredient ranges and direct-to-consumer delivery grows. Professional supply channels restaurant depots, foodservice distributors, specialty baking suppliers remain the backbone of North American volumes.

Europe is where fresh yeast is most deeply embedded in food culture. Countries like France, Germany, Italy, Poland, and the Czech Republic have baking traditions where fresh yeast isn't a specialty ingredient it's the standard. German rye and wheat breads, French viennoiserie, Italian slow-fermented pizza doughs all built around fresh yeast, and none showing signs of changing.

The clean-label movement has reinforced fresh yeast's position further. As consumers demand shorter, more transparent ingredient lists, fresh yeast a single natural, recognizable ingredient fits perfectly. Organic and artisan bakeries have made it a deliberate marketing differentiator, and that resonates strongly with European consumers who scrutinize food provenance.

India, China, Japan, and South Korea are all seeing bakery sectors expand rapidly driven by urbanization, rising disposable incomes, and growing Western food culture influence among younger demographics. Small and medium-sized bakeries are opening at pace across Indian and Chinese cities, many adopting fresh yeast for the texture and flavor advantages it delivers over dry alternatives.

Japan deserves specific attention. Social media, cooking shows, and a cultural appreciation for craft and precision have combined to build a meaningful retail fresh yeast market. Japanese consumers respond strongly to quality signals, and fresh yeast's association with superior baking results has made it a genuine preference in specialty and mainstream grocery retail alike.

Brazil and Argentina have deep food traditions built around fresh-baked goods from Brazilian po de queijo and regional breads to Argentine facturas and medialunas. Local bakeries have historically preferred fresh yeast, and that preference remains firmly intact. Growth may not match Asia-Pacific's pace, but demand is stable and culturally reinforced in ways that make it structurally durable for the long term.

Urban centers across the Middle East particularly Saudi Arabia, the UAE, and Egypt are seeing bakery and foodservice sectors expand as consumer spending on premium food rises. Traditional breads like pita, khubz, and flatbreads are dietary staples across the region, and fresh yeast remains the preferred leavening agent for many of these products. In Sub-Saharan Africa, cold-chain limitations remain a constraint, though urban South Africa and parts of East Africa are tracking upward as food retail and refrigeration investment improves.

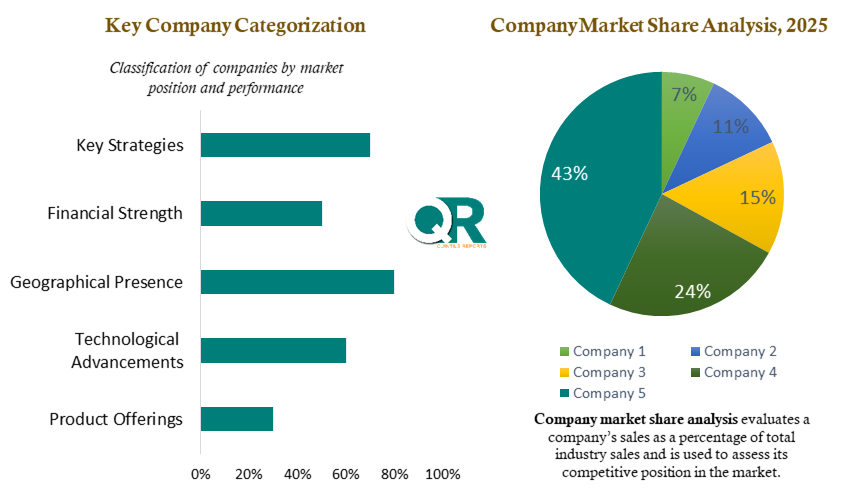

The fresh yeast market is dominated by a relatively small group of large, globally integrated producers but competition within that group is genuinely intense, playing out across several distinct dimensions.

Two recent developments signal where competitive priorities sit. In October 2024, Lesaffre completed the acquisition of dsm-firmenich's yeast extract business integrating processing technology, R&D teams, and product lines into its Biospringer unit, significantly strengthening its position in savory fermentation ingredients and signaling continued consolidation at the market's top. In March 2025, Angel Yeast Co. Ltd. was awarded Best Ingredient Innovation at the World Food Innovation Awards for its yeast-derived protein product AngeoPro recognized for high digestibility, neutral flavor, a complete amino acid profile, and strong sustainability credentials pointing to growing industry interest in yeast as a protein source well beyond baking.

Primary interviews conducted with fresh yeast producers, commercial bakery procurement teams, and foodservice ingredient distributors during Q1 2026 indicate that demand is increasingly shifting toward consistent, high-performance leavening solutions with transparent sourcing credentials, verified strain quality, and clean-label compliance across both artisan and industrial baking operations.

Several bakery procurement managers and foodservice buyers interviewed across North America and Europe also reported growing preference for fresh yeast suppliers offering reliable cold-chain delivery, flexible product formats including compressed block, crumbled, and cream yeast and dedicated technical support for large-scale baking applications.

This section provides a comprehensive analysis of the competitive landscape, highlighting how leading companies differentiate themselves through strategies such as organic certification, cold-press and enzymatic extraction technologies, clean-label positioning, non-GMO and allergen-free formulations, flavor innovation, and value-based product offerings. The assessment helps stakeholders evaluate product innovation, operational capabilities, brand positioning, and overall competitive performance within the market.

The company profiles cover key aspects including business overview, product and service portfolios, financial performance, regional presence, and strategic priorities. Interviews with nutraceutical brand executives and wellness product manufacturers revealed that transparency around sourcing, extraction methods, and third-party testing is becoming a major purchasing factor among health-conscious consumers.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 7.72 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Nature |

|

| The Segment Covered by Type |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This Fresh Yeast Market report is developed using a combination of primary and secondary research methodologies designed to ensure accuracy, analytical depth, and real-world market relevance:

Ongoing analyst monitoring of wellness retail channels and distributor feedback suggests that functional mushroom products are increasingly transitioning from niche supplement categories into mainstream daily wellness routines.

Fresh yeast is deceptively simple a refrigerated block of living cells with a short shelf life yet the market around it is growing steadily toward USD 8.81 Billion by 2036, built on craft baking's global expansion, clean-label demand, and the enduring preference of serious bakers for ingredients that genuinely perform. Cold-chain complexity, dry yeast competition, and dietary trend shifts create real friction but as long as people care about bread quality, and all signs suggest more do, not fewer, fresh yeast holds its ground.

Data references: Global Fresh Yeast Market valuation (USD 4.10 Billion, 2026) and forecast (USD 8.81 Billion, 2036) at a CAGR of 7.72%.

Author: Anaya Shetty, Senior Market Analyst Food & Nutrition Industry | Last Updated: April 2026 | Reviewed By: Vasu Sharma, Research Director Food Ingredients & Bakery, Quintile Reports.

The Fresh Yeast Market report covers size, share, and growth trends from 2026 to 2036, with historical analysis (2017-2024) for stakeholders and decision-makers. Contact sales@quintilereports.com for a sample PDF.

List of Tables

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 21 China Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Fresh Yeast Market: market scenario

Fig.4 Global Fresh Yeast Market competitive outlook

Fig.5 Global Fresh Yeast Market driver analysis

Fig.6 Global Fresh Yeast Market restraint analysis

Fig.7 Global Fresh Yeast Market opportunity analysis

Fig.8 Global Fresh Yeast Market trends analysis

Fig.9 Global Fresh Yeast Market: Segment Analysis (Based on the scope)

Fig.10 Global Fresh Yeast Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

List of Tables

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 21 China Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Fresh Yeast Market: market scenario

Fig.4 Global Fresh Yeast Market competitive outlook

Fig.5 Global Fresh Yeast Market driver analysis

Fig.6 Global Fresh Yeast Market restraint analysis

Fig.7 Global Fresh Yeast Market opportunity analysis

Fig.8 Global Fresh Yeast Market trends analysis

Fig.9 Global Fresh Yeast Market: Segment Analysis (Based on the scope)

Fig.10 Global Fresh Yeast Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

The global Fresh Yeast Market was valued at USD 4.10 Billion in 2026 and is projected to reach USD 8.81 Billion by 2036, growing at a CAGR of 7.72% over the forecast period. This growth is underpinned by rising demand from artisan and commercial bakeries, expanding foodservice sectors, and increasing consumer preference for clean-label, natural leavening ingredients.

Fresh yeast — also known as compressed or baker's yeast — is a biologically active form of Saccharomyces cerevisiae sold in its hydrated, living state with approximately 70% moisture content. Unlike dry or instant yeast, which undergoes dehydration to extend shelf life, fresh yeast cells are metabolically primed and ready to ferment immediately — delivering faster fermentation onset, more even gas production, and a cleaner, more complex flavor profile. The trade-off is a short shelf life of 2 to 4 weeks and strict refrigeration requirements between 0°C and 8°C.

Fresh yeast is commercially available in three primary formats: Compressed blocks — the most widely used format across professional and artisan bakeries, available in retail and large commercial slab sizes. Crumbled fresh yeast — a looser, granular format suited for direct incorporation into large-batch mixing without pre-dissolving. Cream yeast — a liquid slurry format used in high-volume industrial baking operations, offering precise dosing through continuous mixing systems.

Several converging trends are fueling fresh yeast market growth, including the global artisanal bakery renaissance, the sustained post-pandemic home baking culture, rising clean-label formulation demand from consumers and retailers, foodservice sector expansion into in-house bakery operations, and growing awareness of yeast's nutritional credentials — including B vitamins, complete proteins, and prebiotic compounds.

The market faces several structural challenges. Perishability and cold-chain dependency limit distribution reach in regions with inconsistent refrigeration infrastructure. Competition from dry and instant yeast — which offer longer shelf life and greater retail convenience — remains persistent. Molasses supply volatility creates upstream cost instability, and the growing adoption of gluten-free, low-carb, and ketogenic diets poses a longer-term structural headwind by gradually eroding demand for traditional yeast-leavened bread.

Europe is the dominant region for fresh yeast consumption, with countries like France, Germany, Italy, Poland, and the Czech Republic maintaining deep-rooted fresh yeast traditions across commercial, artisan, and home baking segments. North America follows, driven by the artisan bakery revival and post-pandemic home baking interest. Asia-Pacific — particularly India, China, Japan, and South Korea — represents the fastest-growing regional market, fueled by rapid bakery sector expansion and rising urbanization.

The global Fresh Yeast Market is led by a concentrated group of large, vertically integrated producers. Key players include Lesaffre, Lallemand Inc., AB Mauri Foods Inc., Angel Yeast Co. Ltd., Associated British Foods plc, Kerry Group plc, Oriental Yeast Co. Ltd., Chr. Hansen A/S, Cargill Incorporated, DSM N.V., Pakmaya, Red Star Yeast Company, Leiber GmbH, and Bio Springer S.A. These companies compete across fermentation technology, cold-chain infrastructure, product form diversity, and technical customer support.

Two notable developments highlight current competitive priorities. In October 2024, Lesaffre acquired dsm-firmenich's yeast extract business, integrating it into its Biospringer unit to strengthen its position in savory fermentation ingredients. In March 2025, Angel Yeast Co. Ltd. received the Best Ingredient Innovation award at the World Food Innovation Awards for AngeoPro — a yeast-derived protein recognized for high digestibility, neutral flavor, and strong sustainability credentials — signaling the industry's growing interest in yeast as a protein source beyond baking.

The full Fresh Yeast Market report is available through Quintile Reports, covering market size, share, segmentation, competitive benchmarking, regional analysis, and forecasts from 2026 to 2036 with historical data from 2017–2024. To request a sample PDF or speak with an analyst, contact the team at sales@quintilereports.com.

The global Fresh Yeast Market was valued at USD 4.10 Billion in 2026 and is projected to reach USD 8.81 Billion by 2036, growing at a CAGR of 7.72% over the forecast period. Doubling in value over a single decade is no small feat for what is, at its core, one of humanity's oldest fermentation tools but fresh yeast is proving that tradition and growth can absolutely coexist.

The numbers are compelling, but the more interesting story is why. Behind that trajectory sits a global shift in how people relate to food: a renewed appetite for handcrafted breads, clean ingredients, and cooking from scratch. Fresh yeast sits right at the center of that shift.

This report provides detailed Fresh Yeast market size analysis, growth trends, competitive benchmarking, and future industry outlook.

Fresh yeast, also referred to as baker's yeast or compressed yeast, is a living, biologically active form of Saccharomyces cerevisiae the same species of single-celled fungi central to human food production for thousands of years. Unlike dried counterparts, fresh yeast is sold in its hydrated, metabolically active state, with yeast cells alive and ready to ferment sugars immediately upon contact with the right environment.

Fresh yeast carries a moisture content of approximately 70%, giving it that soft, crumbly, pale beige texture most bakers recognize. It is commercially available in three main forms:

What fundamentally sets fresh yeast apart from active dry or instant yeast is biological state. Dehydration arrests yeast cell metabolism and extends shelf life but introduces measurable loss of leavening power. Fresh yeast cells are whole, viable, and metabolically primed, delivering faster fermentation onset, more even gas production, and particularly in enriched or laminated doughs a cleaner, more complex flavor profile. The live cells consume fermentable sugars and produce carbon dioxide (creating structure and lightness) and ethanol (contributing aroma and depth), along with organic acids and esters that chemical leaveners simply cannot replicate.

The trade-off is perishability. Fresh yeast requires continuous refrigeration between 0C and 8C, with a shelf life of just 2 to 4 weeks versus 12 years for dry yeast. That cold-chain dependency makes it logistically demanding, which is why dry alternatives have gained ground in home baking and remote markets. Beyond baking, fresh yeast serves beverage fermentation, bioethanol production, and nutraceutical formulations valued for B vitamins, proteins, and probiotic characteristics. The closely related Yeast Extracts and Beta Glucan market spanning bakery, health food, cosmetics, and medicines shares many of fresh yeast's end-use growth drivers.

The fresh yeast market's growth is driven by several reinforcing trends happening simultaneously.

No honest market analysis glosses over the friction points and fresh yeast has some genuine structural ones.

North America's fresh yeast market is being shaped by two converging forces: the professionalization of the artisan bakery sector and the sustained post-pandemic interest in home baking. The U.S. in particular has seen a wave of independent bakeries built around long-fermentation, naturally leavened, and enriched-dough products that genuinely benefit from fresh yeast's fermentation characteristics.

At the retail level, fresh yeast availability remains patchy compared to Europe not every grocery chain stocks it, and formats are often limited. But that's slowly changing as specialty food retailers expand baking ingredient ranges and direct-to-consumer delivery grows. Professional supply channels restaurant depots, foodservice distributors, specialty baking suppliers remain the backbone of North American volumes.

Europe is where fresh yeast is most deeply embedded in food culture. Countries like France, Germany, Italy, Poland, and the Czech Republic have baking traditions where fresh yeast isn't a specialty ingredient it's the standard. German rye and wheat breads, French viennoiserie, Italian slow-fermented pizza doughs all built around fresh yeast, and none showing signs of changing.

The clean-label movement has reinforced fresh yeast's position further. As consumers demand shorter, more transparent ingredient lists, fresh yeast a single natural, recognizable ingredient fits perfectly. Organic and artisan bakeries have made it a deliberate marketing differentiator, and that resonates strongly with European consumers who scrutinize food provenance.

India, China, Japan, and South Korea are all seeing bakery sectors expand rapidly driven by urbanization, rising disposable incomes, and growing Western food culture influence among younger demographics. Small and medium-sized bakeries are opening at pace across Indian and Chinese cities, many adopting fresh yeast for the texture and flavor advantages it delivers over dry alternatives.

Japan deserves specific attention. Social media, cooking shows, and a cultural appreciation for craft and precision have combined to build a meaningful retail fresh yeast market. Japanese consumers respond strongly to quality signals, and fresh yeast's association with superior baking results has made it a genuine preference in specialty and mainstream grocery retail alike.

Brazil and Argentina have deep food traditions built around fresh-baked goods from Brazilian po de queijo and regional breads to Argentine facturas and medialunas. Local bakeries have historically preferred fresh yeast, and that preference remains firmly intact. Growth may not match Asia-Pacific's pace, but demand is stable and culturally reinforced in ways that make it structurally durable for the long term.

Urban centers across the Middle East particularly Saudi Arabia, the UAE, and Egypt are seeing bakery and foodservice sectors expand as consumer spending on premium food rises. Traditional breads like pita, khubz, and flatbreads are dietary staples across the region, and fresh yeast remains the preferred leavening agent for many of these products. In Sub-Saharan Africa, cold-chain limitations remain a constraint, though urban South Africa and parts of East Africa are tracking upward as food retail and refrigeration investment improves.

The fresh yeast market is dominated by a relatively small group of large, globally integrated producers but competition within that group is genuinely intense, playing out across several distinct dimensions.

Two recent developments signal where competitive priorities sit. In October 2024, Lesaffre completed the acquisition of dsm-firmenich's yeast extract business integrating processing technology, R&D teams, and product lines into its Biospringer unit, significantly strengthening its position in savory fermentation ingredients and signaling continued consolidation at the market's top. In March 2025, Angel Yeast Co. Ltd. was awarded Best Ingredient Innovation at the World Food Innovation Awards for its yeast-derived protein product AngeoPro recognized for high digestibility, neutral flavor, a complete amino acid profile, and strong sustainability credentials pointing to growing industry interest in yeast as a protein source well beyond baking.

Primary interviews conducted with fresh yeast producers, commercial bakery procurement teams, and foodservice ingredient distributors during Q1 2026 indicate that demand is increasingly shifting toward consistent, high-performance leavening solutions with transparent sourcing credentials, verified strain quality, and clean-label compliance across both artisan and industrial baking operations.

Several bakery procurement managers and foodservice buyers interviewed across North America and Europe also reported growing preference for fresh yeast suppliers offering reliable cold-chain delivery, flexible product formats including compressed block, crumbled, and cream yeast and dedicated technical support for large-scale baking applications.

This section provides a comprehensive analysis of the competitive landscape, highlighting how leading companies differentiate themselves through strategies such as organic certification, cold-press and enzymatic extraction technologies, clean-label positioning, non-GMO and allergen-free formulations, flavor innovation, and value-based product offerings. The assessment helps stakeholders evaluate product innovation, operational capabilities, brand positioning, and overall competitive performance within the market.

The company profiles cover key aspects including business overview, product and service portfolios, financial performance, regional presence, and strategic priorities. Interviews with nutraceutical brand executives and wellness product manufacturers revealed that transparency around sourcing, extraction methods, and third-party testing is becoming a major purchasing factor among health-conscious consumers.

| Report Scope | Details |

| Report Version | 2026 |

| Growth Rate | CAGR of 7.72 % from 2026 to 2036 |

| Base Year | 2025 |

| Actual Estimates / Historical Data | 2017 - 2024 |

| Forecast Period | 2026 - 2036 |

| Quantitative Units | Revenue in USD million/billion & CAGR from 2026 to 2036 |

| Country Scope | North America (U.S., Canada), Europe (UK, Germany, France, Italy, Spain, Russia, Sweden, Denmark, Norway, Rest of Europe), Asia Pacific (Japan, China, India, Australia, South Korea, Thailand, Rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, Colombia, Rest of Latin America), Middle East & Africa (South Africa, Saudi Arabia, UAE, Kuwait, Rest of Middle East & Africa). |

| The Segment Covered by Nature |

|

| The Segment Covered by Type |

|

| Companies Covered |

|

| Report Coverage | Revenue forecast, company share, competitive landscape, growth factors, technology trends, and regional analysis |

| Free Customization Scope (Equivalent to 5 Analyst Working Days) | If you require additional insights beyond the current scope, our analysts can customize the report to meet your specific business needs. |

This Fresh Yeast Market report is developed using a combination of primary and secondary research methodologies designed to ensure accuracy, analytical depth, and real-world market relevance:

Ongoing analyst monitoring of wellness retail channels and distributor feedback suggests that functional mushroom products are increasingly transitioning from niche supplement categories into mainstream daily wellness routines.

Fresh yeast is deceptively simple a refrigerated block of living cells with a short shelf life yet the market around it is growing steadily toward USD 8.81 Billion by 2036, built on craft baking's global expansion, clean-label demand, and the enduring preference of serious bakers for ingredients that genuinely perform. Cold-chain complexity, dry yeast competition, and dietary trend shifts create real friction but as long as people care about bread quality, and all signs suggest more do, not fewer, fresh yeast holds its ground.

Data references: Global Fresh Yeast Market valuation (USD 4.10 Billion, 2026) and forecast (USD 8.81 Billion, 2036) at a CAGR of 7.72%.

Author: Anaya Shetty, Senior Market Analyst Food & Nutrition Industry | Last Updated: April 2026 | Reviewed By: Vasu Sharma, Research Director Food Ingredients & Bakery, Quintile Reports.

The Fresh Yeast Market report covers size, share, and growth trends from 2026 to 2036, with historical analysis (2017-2024) for stakeholders and decision-makers. Contact sales@quintilereports.com for a sample PDF.

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 21 China Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Fresh Yeast Market: market scenario

Fig.4 Global Fresh Yeast Market competitive outlook

Fig.5 Global Fresh Yeast Market driver analysis

Fig.6 Global Fresh Yeast Market restraint analysis

Fig.7 Global Fresh Yeast Market opportunity analysis

Fig.8 Global Fresh Yeast Market trends analysis

Fig.9 Global Fresh Yeast Market: Segment Analysis (Based on the scope)

Fig.10 Global Fresh Yeast Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

Table 1 List of Abbreviation and acronyms

Table 2 List of Sources

Table 3 North America Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 4 North America Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 5 U.S. Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 6 Canada Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 7 Europe Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 8 Europe Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 9 Germany Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 10 U.K. Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 11 France Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 12 Italy Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 13 Spain Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 14 Sweden Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 15 Denmark Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 16 Norway Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 17 The Netherlands Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 18 Russia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 19 Asia Pacific Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 20 Asia Pacific Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 21 China Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 22 Japan Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 23 India Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 24 Australia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 25 South Korea Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 26 Thailand Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 27 Latin America Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 28 Latin America Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 29 Brazil Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 30 Mexico Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 31 Argentina Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 32 Middle East and Africa Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 33 Middle East and Africa Global Fresh Yeast Market, by Region, (USD Million) 2017-2035

Table 34 South Africa Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 35 Saudi Arabia Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 36 UAE Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 37 Kuwait Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Table 38 Turkey Global Fresh Yeast Market, by Segment Analysis, (USD Million) 2017-2035

Fig.1 Market research process

Fig.2 Market research approaches

Fig.3 Global Fresh Yeast Market: market scenario

Fig.4 Global Fresh Yeast Market competitive outlook

Fig.5 Global Fresh Yeast Market driver analysis

Fig.6 Global Fresh Yeast Market restraint analysis

Fig.7 Global Fresh Yeast Market opportunity analysis

Fig.8 Global Fresh Yeast Market trends analysis

Fig.9 Global Fresh Yeast Market: Segment Analysis (Based on the scope)

Fig.10 Global Fresh Yeast Market: regional analysis

Fig.11 Global market shares and leading market players

Fig.12 North America market share and leading players

Fig.13 Europe market share and leading players

Fig.14 Asia Pacific market share and leading players

Fig.15 Latin America market share and leading players

Fig.16 Middle East & Africa market share and leading players

Fig.17 North America, by country

Fig.18 North America

Fig.19 North America market estimates and forecast, 2017-2035

Fig.20 U.S.

Fig.21 Canada

Fig.22 Europe

Fig.23 Europe market estimates and forecast, 2017-2035

Fig.24 U.K.

Fig.25 Germany

Fig.26 France

Fig.27 Italy

Fig.28 Spain

Fig.29 Sweden

Fig.30 Denmark

Fig.31 Norway

Fig.32 The Netherlands

Fig.33 Russia

Fig.34 Asia Pacific

Fig.35 Asia Pacific market estimates and forecast, 2017-2035

Fig.36 China

Fig.37 Japan

Fig.38 India

Fig.39 Australia

Fig.40 South Korea

Fig.41 Thailand

Fig.42 Latin America

Fig.43 Latin America market estimates and forecast, 2017-2035

Fig.44 Brazil

Fig.45 Mexico

Fig.46 Argentina

Fig.47 Colombia

Fig.48 Middle East and Africa

Fig.49 Middle East and Africa market estimates and forecast, 2017-2035

Fig.50 Saudi Arabia

Fig.51 South Africa

Fig.52 UAE

Fig.53 Kuwait

Fig.54 Turkey

A license granted to one user. Rules or conditions might be applied for e.g. the use of electric files (PDFs) or printings, depending on product.

A license granted to multiple users.

A license granted to a single business site/establishment.

A license granted to all employees within organisation access to the product.

Immediate / Within 24-48 hours - Working days

Online Payments with PayPal and CCavenue

You can order a report by picking any of the payment methods which is bank wire or online payment through any Debit/Credit card or PayPal.

Hard Copy